Das könnte Ihnen auch gefallen

- Accounting and Financial Reporting FundamentalsDokument19 SeitenAccounting and Financial Reporting FundamentalstundsandyNoch keine Bewertungen

- ACT103 - Module 1Dokument13 SeitenACT103 - Module 1Le MinouNoch keine Bewertungen

- Lesson 1Dokument9 SeitenLesson 1Bervette HansNoch keine Bewertungen

- Review of The Accounting ProcessDokument10 SeitenReview of The Accounting ProcessFranz TagubaNoch keine Bewertungen

- #02 Conceptual FrameworkDokument5 Seiten#02 Conceptual FrameworkZaaavnn VannnnnNoch keine Bewertungen

- Introduction To AccountingDokument9 SeitenIntroduction To AccountingJessicaNoch keine Bewertungen

- Accounts 1Dokument14 SeitenAccounts 1Piyush PatelNoch keine Bewertungen

- Chapter 5 Principls and ConceptsDokument10 SeitenChapter 5 Principls and ConceptsawlachewNoch keine Bewertungen

- Limitations of Financial AccountingDokument6 SeitenLimitations of Financial Accountingchitra_shresthaNoch keine Bewertungen

- Chapter 3-Adjusting The AccountsDokument26 SeitenChapter 3-Adjusting The Accountsbebybey100% (1)

- CMBE 2 - Lesson 1 ModuleDokument11 SeitenCMBE 2 - Lesson 1 ModuleEunice AmbrocioNoch keine Bewertungen

- Journal EntriesDokument40 SeitenJournal EntriesPai100% (4)

- Introduction To Accounting: StructureDokument418 SeitenIntroduction To Accounting: StructureRashadNoch keine Bewertungen

- Chapter 5 Expenditure Cycle Part 1Dokument33 SeitenChapter 5 Expenditure Cycle Part 1KRIS ANNE SAMUDIO100% (1)

- CMBE 2 - Lesson 3 ModuleDokument12 SeitenCMBE 2 - Lesson 3 ModuleEunice AmbrocioNoch keine Bewertungen

- Concepts, Principles and Convensions - AnoverviewDokument6 SeitenConcepts, Principles and Convensions - AnoverviewA KA SH TickuNoch keine Bewertungen

- Role of Accounting in SocietyDokument9 SeitenRole of Accounting in SocietyAbdul GafoorNoch keine Bewertungen

- Lecture 1 - 2-Basics of AccountingDokument29 SeitenLecture 1 - 2-Basics of AccountingRavi KumarNoch keine Bewertungen

- Chap 1-4Dokument20 SeitenChap 1-4Rose Ann Robante TubioNoch keine Bewertungen

- Accounting and Finance For Managers - Course Material PDFDokument94 SeitenAccounting and Finance For Managers - Course Material PDFbil gossayw100% (1)

- Debited The Asset Supplies. This Account Shows A Debited The Account Supplies Expense. ThisDokument4 SeitenDebited The Asset Supplies. This Account Shows A Debited The Account Supplies Expense. ThiszairahNoch keine Bewertungen

- ACCOUNTING CONCEPTS, CONVENTIONS AND PRINCIPLES EXPLAINEDDokument42 SeitenACCOUNTING CONCEPTS, CONVENTIONS AND PRINCIPLES EXPLAINEDSheetal NafdeNoch keine Bewertungen

- Accountancy - Chapter 4 & 5Dokument5 SeitenAccountancy - Chapter 4 & 5maricarNoch keine Bewertungen

- Introduction to Accounting BranchesDokument13 SeitenIntroduction to Accounting BranchesKelvin Jay Sebastian SaplaNoch keine Bewertungen

- Chapter 3 AccountingDokument11 SeitenChapter 3 AccountingĐỗ ĐăngNoch keine Bewertungen

- Chapter 1: Introduction To AccountingDokument17 SeitenChapter 1: Introduction To AccountingPALADUGU MOUNIKANoch keine Bewertungen

- (201001 - 201020) Afar - Partnership Formation (PPT Version)Dokument41 Seiten(201001 - 201020) Afar - Partnership Formation (PPT Version)Mau Dela CruzNoch keine Bewertungen

- 13Dokument63 Seiten13amysilverbergNoch keine Bewertungen

- Accountancy ManualDokument61 SeitenAccountancy ManualAhmad Fauzi MehatNoch keine Bewertungen

- Accounting ConceptsDokument13 SeitenAccounting ConceptsdeepshrmNoch keine Bewertungen

- The Accounting Cycle: 9-Step Accounting Process InshareDokument3 SeitenThe Accounting Cycle: 9-Step Accounting Process InshareBTS ARMYNoch keine Bewertungen

- Module 2 - Financial Statements - Organized PDFDokument14 SeitenModule 2 - Financial Statements - Organized PDFSandyNoch keine Bewertungen

- CAT Level 1 Mock Examination-1Dokument4 SeitenCAT Level 1 Mock Examination-1Nadine ReidNoch keine Bewertungen

- Acct1a&b Chapter 1 ReviewerDokument3 SeitenAcct1a&b Chapter 1 ReviewerKathleen Louise VarillaNoch keine Bewertungen

- Journal Entries - Financial AccountingDokument3 SeitenJournal Entries - Financial AccountingElham JabarkhailNoch keine Bewertungen

- Ch05-Job CostingDokument35 SeitenCh05-Job Costingemanmaryum7Noch keine Bewertungen

- 4 Pas 7 - Statement of Cash Flows: Objective and ScopeDokument17 Seiten4 Pas 7 - Statement of Cash Flows: Objective and ScopeRose Aubrey A Cordova100% (1)

- Basic Accounting ReviewDokument75 SeitenBasic Accounting ReviewSofie SergioNoch keine Bewertungen

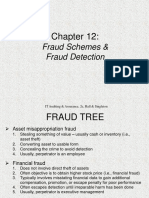

- Ch12 Fraud Scheme DetectionDokument18 SeitenCh12 Fraud Scheme DetectionPanda BoarsNoch keine Bewertungen

- NVCC Accounting ACC 211 EXAM 1 PracticeDokument12 SeitenNVCC Accounting ACC 211 EXAM 1 Practiceflak27bl2Noch keine Bewertungen

- Trends in Accounting ResearchDokument14 SeitenTrends in Accounting ResearchNoel ConsultaNoch keine Bewertungen

- The Revenue Cycle: Group 1Dokument43 SeitenThe Revenue Cycle: Group 1Ratih PratiwiNoch keine Bewertungen

- Types of Major Accounts: An Account Is The Basic Storage of Information in AccountingDokument15 SeitenTypes of Major Accounts: An Account Is The Basic Storage of Information in AccountingGab GamboaNoch keine Bewertungen

- CQCF - Qualitative CharacteristicsDokument4 SeitenCQCF - Qualitative CharacteristicsEllen MaskariñoNoch keine Bewertungen

- Elements of Financial StatementsDokument2 SeitenElements of Financial StatementsHanifah AyuNoch keine Bewertungen

- BBA 1st Sem. FULL SYLLABUS Basic AccountingDokument115 SeitenBBA 1st Sem. FULL SYLLABUS Basic AccountingYash KhattriNoch keine Bewertungen

- Module 2 - Financial Accounting PrinciplesDokument13 SeitenModule 2 - Financial Accounting PrinciplesVimbai MusangeyaNoch keine Bewertungen

- Unit 1. Introduction To Accounting and Business 1.1Dokument25 SeitenUnit 1. Introduction To Accounting and Business 1.1Qabsoo FiniinsaaNoch keine Bewertungen

- Residual Equity TheoryDokument3 SeitenResidual Equity Theorybrix simeonNoch keine Bewertungen

- Chapter-3Dokument30 SeitenChapter-3Catherine Rivera100% (1)

- Strategic Cost Management Jpfranco: Lecture Note in Responsibility AccountingDokument10 SeitenStrategic Cost Management Jpfranco: Lecture Note in Responsibility AccountingAnnamarisse parungaoNoch keine Bewertungen

- Yveth Lumabi 1 C-BSOADokument8 SeitenYveth Lumabi 1 C-BSOAYveth LumabiNoch keine Bewertungen

- Chapter 1 BASIC ACCOUNTING FEATURES CONCEPT AND PRINCIPLESDokument13 SeitenChapter 1 BASIC ACCOUNTING FEATURES CONCEPT AND PRINCIPLESTiffany VinzonNoch keine Bewertungen

- ACCOUNTING PRINCIPLES AND CONCEPTS EXPLAINEDDokument57 SeitenACCOUNTING PRINCIPLES AND CONCEPTS EXPLAINEDLucky MehNoch keine Bewertungen

- GFA06 - Financial Analysis and Appraisal of ProjectsDokument48 SeitenGFA06 - Financial Analysis and Appraisal of ProjectswossenNoch keine Bewertungen

- BA Module (Day 1)Dokument60 SeitenBA Module (Day 1)Jamie CantubaNoch keine Bewertungen

- Module For AccountingDokument46 SeitenModule For AccountingJhefz KhurtzNoch keine Bewertungen

- Acctg 2 Module 2Dokument5 SeitenAcctg 2 Module 2Reina Marie W. TamposNoch keine Bewertungen