Das könnte Ihnen auch gefallen

- Budget 2014-15 Analysis - Vedantam GuptaDokument3 SeitenBudget 2014-15 Analysis - Vedantam GuptaVedantam GuptaNoch keine Bewertungen

- IMF Conditionality Package 2013Dokument20 SeitenIMF Conditionality Package 2013Safia AslamNoch keine Bewertungen

- Driving Growth Union Budget 2023 24Dokument25 SeitenDriving Growth Union Budget 2023 24shwetaNoch keine Bewertungen

- Jism Jan14 FiscalDokument16 SeitenJism Jan14 FiscalramakntaNoch keine Bewertungen

- Union Budget 2013-14: No Change in Income Tax Slabs Relief of Rs 2,000 For Tax Payers in Tax Bracket of Rs. 2-5 LakhDokument1 SeiteUnion Budget 2013-14: No Change in Income Tax Slabs Relief of Rs 2,000 For Tax Payers in Tax Bracket of Rs. 2-5 LakhShruti SharmaNoch keine Bewertungen

- EconomicSurvey2014 15Dokument22 SeitenEconomicSurvey2014 15tbharathkumarreddy3081Noch keine Bewertungen

- India Union BudgetDokument12 SeitenIndia Union BudgetMd DhaniyalNoch keine Bewertungen

- Fiscal Framework: Ntroduction AND UmmaryDokument1 SeiteFiscal Framework: Ntroduction AND UmmarySagargn SagarNoch keine Bewertungen

- Indian Union Budget 2020Dokument11 SeitenIndian Union Budget 2020Md DhaniyalNoch keine Bewertungen

- Budget 2012Dokument6 SeitenBudget 2012Divya HdsNoch keine Bewertungen

- Bangladesh Quarterly Economic Update: June 2014Von EverandBangladesh Quarterly Economic Update: June 2014Noch keine Bewertungen

- Fiscal and Monetary Policy Developments in PakistanDokument19 SeitenFiscal and Monetary Policy Developments in PakistanNazish IlyasNoch keine Bewertungen

- Expenditure Management CommissionDokument36 SeitenExpenditure Management CommissionaronNoch keine Bewertungen

- Final Exam 13574 PDFDokument5 SeitenFinal Exam 13574 PDFHome PhoneNoch keine Bewertungen

- Since Assuming Office in May 2014, The New Government Has Undertaken A Number of New Reform Measures Whose Cumulative Impact Could Be SubstantialDokument9 SeitenSince Assuming Office in May 2014, The New Government Has Undertaken A Number of New Reform Measures Whose Cumulative Impact Could Be SubstantialOkay PlusNoch keine Bewertungen

- Nion Udget: Prepared by Jignesh S Vamja - 4 SemDokument26 SeitenNion Udget: Prepared by Jignesh S Vamja - 4 SemjigneshvamjaNoch keine Bewertungen

- Single Biggest Challenge India Faces With Respect To Macro-EconomicsDokument3 SeitenSingle Biggest Challenge India Faces With Respect To Macro-EconomicsAnonymous K8h21n5dNoch keine Bewertungen

- Key Features of Budget 2012-2013Dokument15 SeitenKey Features of Budget 2012-2013anupbhansali2004Noch keine Bewertungen

- Trade Policy Review Report by Pakistan: Orld Rade RganizationDokument13 SeitenTrade Policy Review Report by Pakistan: Orld Rade Rganizationthewizards_nomanNoch keine Bewertungen

- Grant Thornton Analaysis-Budget 2013-14Dokument39 SeitenGrant Thornton Analaysis-Budget 2013-14Kazmi Uzair SultanNoch keine Bewertungen

- BudgetDokument50 SeitenBudgetPankajBhardwajNoch keine Bewertungen

- SPEX Issue 35Dokument12 SeitenSPEX Issue 35SMU Political-Economics Exchange (SPEX)Noch keine Bewertungen

- Budget Main PagesDokument43 SeitenBudget Main Pagesneha16septNoch keine Bewertungen

- Indian Economy IDokument10 SeitenIndian Economy IVirendra SinghNoch keine Bewertungen

- Budget Recommendations NationalDokument5 SeitenBudget Recommendations NationalAyushRajNoch keine Bewertungen

- Assignment Fiscal Policy in The PhilippinesDokument16 SeitenAssignment Fiscal Policy in The PhilippinesOliver SantosNoch keine Bewertungen

- Monthly Economic Affairs - June, 2014Dokument40 SeitenMonthly Economic Affairs - June, 2014The CSS PointNoch keine Bewertungen

- Article of Economic TimesDokument5 SeitenArticle of Economic TimesHarin LydiaNoch keine Bewertungen

- GDP Growth Sustained: Total Expenditure Has Increased by Rs. 192669 Crore in 2016-17 (BE) From 2015-16 (RE)Dokument4 SeitenGDP Growth Sustained: Total Expenditure Has Increased by Rs. 192669 Crore in 2016-17 (BE) From 2015-16 (RE)Aryan DeepNoch keine Bewertungen

- Budget 2024 25 Summary 1706888004Dokument20 SeitenBudget 2024 25 Summary 1706888004scientist xyzNoch keine Bewertungen

- Budget Analysis Bolsters BharatDokument28 SeitenBudget Analysis Bolsters BharatPramod KumarNoch keine Bewertungen

- 3 Year Action AgendaDokument12 Seiten3 Year Action AgendaUmar FarooqNoch keine Bewertungen

- The Indian Economy: Some Current Concerns: First Dr. A.D. Shinde Memorial LectureDokument23 SeitenThe Indian Economy: Some Current Concerns: First Dr. A.D. Shinde Memorial LectureAjeet ParmarNoch keine Bewertungen

- Union Budget 2013-14: Key Takeout's From The BudgetDokument4 SeitenUnion Budget 2013-14: Key Takeout's From The BudgetFeedback Business Consulting Services Pvt. Ltd.Noch keine Bewertungen

- India: Highlights of The 2012/2013 Budget: The Indian Government Has Announced Its Proposals For The 2012/13 BudgetDokument4 SeitenIndia: Highlights of The 2012/2013 Budget: The Indian Government Has Announced Its Proposals For The 2012/13 BudgetVishal PranavNoch keine Bewertungen

- Union Budget 2019-20: July 5, 2019Dokument19 SeitenUnion Budget 2019-20: July 5, 2019majhiajitNoch keine Bewertungen

- Union Budget Report 2019 20 PDFDokument19 SeitenUnion Budget Report 2019 20 PDFok2Noch keine Bewertungen

- Budget AnalysisDokument9 SeitenBudget AnalysisRishi BiggheNoch keine Bewertungen

- Economic Survey 2015 SummaryDokument41 SeitenEconomic Survey 2015 SummaryMohit JangidNoch keine Bewertungen

- Chidambaram Using Postponement Principle to Meet Fiscal Deficit TargetDokument3 SeitenChidambaram Using Postponement Principle to Meet Fiscal Deficit TargetAnonymous 13ulUnpZNoch keine Bewertungen

- Bold Step Towards 5 Trillion Economy: CMA Bhogavalli Mallikarjuna GuptaDokument3 SeitenBold Step Towards 5 Trillion Economy: CMA Bhogavalli Mallikarjuna GuptavenkannaNoch keine Bewertungen

- India's Economic Survey forecasts 6.1-6.7% GDP growth for 2013-14Dokument2 SeitenIndia's Economic Survey forecasts 6.1-6.7% GDP growth for 2013-14scribd0Noch keine Bewertungen

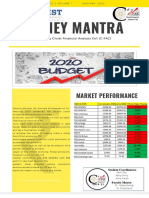

- Money Mantra: Market PerformanceDokument4 SeitenMoney Mantra: Market PerformanceAlbin SibyNoch keine Bewertungen

- Eco Project FinalDokument7 SeitenEco Project FinalVirag ShingaviNoch keine Bewertungen

- Budget 2021-2022: by Y. NikhileshwaraDokument2 SeitenBudget 2021-2022: by Y. NikhileshwaraNarayan AgrawalNoch keine Bewertungen

- Fiscal Policy Strategy StatementDokument8 SeitenFiscal Policy Strategy Statementjosephdass756Noch keine Bewertungen

- ECO 6 FDDokument16 SeitenECO 6 FD20047 BHAVANDEEP SINGHNoch keine Bewertungen

- India Union Budget 2013 PWC Analysis BookletDokument40 SeitenIndia Union Budget 2013 PWC Analysis BookletsuchjazzNoch keine Bewertungen

- Economic Survey 2015-16 highlights key challenges facing Indian economyDokument1 SeiteEconomic Survey 2015-16 highlights key challenges facing Indian economyAspirant NewbieNoch keine Bewertungen

- Economic Survey 2014-15 HighlightsDokument2 SeitenEconomic Survey 2014-15 HighlightsManish MishraNoch keine Bewertungen

- Bounties For The Well-Off: NtroductionDokument10 SeitenBounties For The Well-Off: NtroductionshubhamNoch keine Bewertungen

- Union Budget 2016-17 - Impact AnalysisDokument4 SeitenUnion Budget 2016-17 - Impact AnalysishareshmsNoch keine Bewertungen

- A Windfall For Rural and Agriculture. Peanuts For The SalariedDokument20 SeitenA Windfall For Rural and Agriculture. Peanuts For The SalariedhompatNoch keine Bewertungen

- Highlights of Budget 2009-10Dokument13 SeitenHighlights of Budget 2009-10chauhanaimt38Noch keine Bewertungen

- Telecom Industry: Group Member: Sunil Soni Shashank Chaturvedi Mukesh Saurabh KumarDokument17 SeitenTelecom Industry: Group Member: Sunil Soni Shashank Chaturvedi Mukesh Saurabh Kumarmukesh04Noch keine Bewertungen

- February 28, 2015: Key Features of Budget 2015-2016Dokument17 SeitenFebruary 28, 2015: Key Features of Budget 2015-2016Rajendra Prasad R SNoch keine Bewertungen

- Macro Perspective On Fiscal ConsiderationDokument10 SeitenMacro Perspective On Fiscal Considerationkhan_sadiNoch keine Bewertungen

- Business Environment: Budget 2013-2014 AnalysisDokument11 SeitenBusiness Environment: Budget 2013-2014 AnalysisKyle BaileyNoch keine Bewertungen

- Bangladesh Quarterly Economic Update: September 2014Von EverandBangladesh Quarterly Economic Update: September 2014Noch keine Bewertungen

- CbseDokument10 SeitenCbsedarshanraghuNoch keine Bewertungen

- 2.sbi Po Exam 28-4-13.text - Marked.text - MarkedDokument40 Seiten2.sbi Po Exam 28-4-13.text - Marked.text - MarkedAmit ChauhanNoch keine Bewertungen

- 6Dokument9 Seiten6Sagargn SagarNoch keine Bewertungen

- 11 & 12 February-2018 CA Kannada1Dokument5 Seiten11 & 12 February-2018 CA Kannada1Sagargn SagarNoch keine Bewertungen

- Economic Survey 2015 SummaryDokument41 SeitenEconomic Survey 2015 SummaryMohit JangidNoch keine Bewertungen

- Precis WritingDokument7 SeitenPrecis WritingJyotidesaiNoch keine Bewertungen

- Community Development ProgrammesDokument7 SeitenCommunity Development ProgrammesSirajBashirNoch keine Bewertungen

- Environment, Resources & Biodiversity Answers: 1. (B) Exp.: 6. (D) 7. (C) 8. (A) Exp.Dokument5 SeitenEnvironment, Resources & Biodiversity Answers: 1. (B) Exp.: 6. (D) 7. (C) 8. (A) Exp.Sagargn SagarNoch keine Bewertungen

- 66 75Dokument10 Seiten66 75Sagargn SagarNoch keine Bewertungen

- Principles of Distributive JusticeDokument9 SeitenPrinciples of Distributive JusticeSagargn SagarNoch keine Bewertungen

- Lekhana - M Govinda PaiDokument11 SeitenLekhana - M Govinda PaiSagargn SagarNoch keine Bewertungen

- Panchayat Raj Act 1947 Ch4.38-50Dokument13 SeitenPanchayat Raj Act 1947 Ch4.38-50pankajpandeylkoNoch keine Bewertungen

- Cooperative Societies WriteupDokument8 SeitenCooperative Societies WriteupSagargn SagarNoch keine Bewertungen

- GP Mains 99 Rural Devpt and CoopDokument12 SeitenGP Mains 99 Rural Devpt and CoopSagargn SagarNoch keine Bewertungen

- CSM 2014 Result WQDokument8 SeitenCSM 2014 Result WQDivay Khosla100% (1)

- Agriculture: 1) National Food Security MissionDokument16 SeitenAgriculture: 1) National Food Security MissionSagargn SagarNoch keine Bewertungen

- Daily Docket 2.0 PDFDokument1 SeiteDaily Docket 2.0 PDFSummer NgoNoch keine Bewertungen

- 16 Co-Operative Inspector ADokument1 Seite16 Co-Operative Inspector ASagargn SagarNoch keine Bewertungen

- Number Series TricksDokument4 SeitenNumber Series TricksSatywan SainiNoch keine Bewertungen

- SSC CGL Post Preference List Amp Job Profile of All PostsDokument6 SeitenSSC CGL Post Preference List Amp Job Profile of All PostsSagargn SagarNoch keine Bewertungen

- Nature of PostsDokument13 SeitenNature of PostsSagargn SagarNoch keine Bewertungen

- BESCOMDokument1 SeiteBESCOMSagargn SagarNoch keine Bewertungen

- SSC CGL 2014 Tier-1 Exam Topic Wise AnalysisDokument3 SeitenSSC CGL 2014 Tier-1 Exam Topic Wise AnalysisSagargn SagarNoch keine Bewertungen

- Ancient India (160 KB) PDFDokument26 SeitenAncient India (160 KB) PDFPraveen VermaNoch keine Bewertungen

- Revised Ug Fee Notification MBBS, Bds & Ayush June-2015 Dated 06.06.2015Dokument4 SeitenRevised Ug Fee Notification MBBS, Bds & Ayush June-2015 Dated 06.06.2015Sagargn SagarNoch keine Bewertungen

- CH 01Dokument8 SeitenCH 01api-295592931Noch keine Bewertungen

- Ss Teacher BDokument1 SeiteSs Teacher BSagargn SagarNoch keine Bewertungen

- Status NotfnDokument8 SeitenStatus NotfnSagargn SagarNoch keine Bewertungen

- Notification AdvertisementDokument8 SeitenNotification AdvertisementvijaikirubaNoch keine Bewertungen

- Conservation of Kuttichira SettlementDokument145 SeitenConservation of Kuttichira SettlementSumayya Kareem100% (1)

- Networks Lab Assignment 1Dokument2 SeitenNetworks Lab Assignment 1006honey006Noch keine Bewertungen

- p2 - Guerrero Ch13Dokument40 Seitenp2 - Guerrero Ch13JerichoPedragosa88% (17)

- Beyond B2 English CourseDokument1 SeiteBeyond B2 English Coursecarlitos_coolNoch keine Bewertungen

- Women Safety AppDokument18 SeitenWomen Safety AppVinod BawaneNoch keine Bewertungen

- Network Theory - BASICS - : By: Mr. Vinod SalunkheDokument17 SeitenNetwork Theory - BASICS - : By: Mr. Vinod Salunkhevinod SALUNKHENoch keine Bewertungen

- Recent Advances in Active Metal Brazing of Ceramics and Process-S12540-019-00536-4Dokument12 SeitenRecent Advances in Active Metal Brazing of Ceramics and Process-S12540-019-00536-4sebjangNoch keine Bewertungen

- Appendix B, Profitability AnalysisDokument97 SeitenAppendix B, Profitability AnalysisIlya Yasnorina IlyasNoch keine Bewertungen

- Batool2019 Article ANanocompositePreparedFromMagn PDFDokument10 SeitenBatool2019 Article ANanocompositePreparedFromMagn PDFmazharNoch keine Bewertungen

- (V) 2020-Using Extensive Reading in Improving Reading Speed and Level of Reading Comprehension of StudentsDokument7 Seiten(V) 2020-Using Extensive Reading in Improving Reading Speed and Level of Reading Comprehension of StudentsMEYTA RAHMATUL AZKIYANoch keine Bewertungen

- Effects of War On EconomyDokument7 SeitenEffects of War On Economyapi-3721555100% (1)

- Fabm2 q2 Module 4 TaxationDokument17 SeitenFabm2 q2 Module 4 TaxationLady HaraNoch keine Bewertungen

- CONNECTIFYDokument3 SeitenCONNECTIFYAbhishek KulshresthaNoch keine Bewertungen

- Lay Out New PL Press QltyDokument68 SeitenLay Out New PL Press QltyDadan Hendra KurniawanNoch keine Bewertungen

- Lesson Plan 12 Climate ChangeDokument5 SeitenLesson Plan 12 Climate ChangeRey Bello MalicayNoch keine Bewertungen

- Diferencias Gas LP y Gas Natural: Adminigas, S.A. de C.VDokument2 SeitenDiferencias Gas LP y Gas Natural: Adminigas, S.A. de C.VMarco Antonio Zelada HurtadoNoch keine Bewertungen

- 2.5L ENGINE Chevy Tracker 1999Dokument580 Seiten2.5L ENGINE Chevy Tracker 1999andres german romeroNoch keine Bewertungen

- Design of Steel Structures Handout 2012-2013Dokument3 SeitenDesign of Steel Structures Handout 2012-2013Tushar Gupta100% (1)

- Lignan & NeolignanDokument12 SeitenLignan & NeolignanUle UleNoch keine Bewertungen

- Outstanding 12m Bus DrivelineDokument2 SeitenOutstanding 12m Bus DrivelineArshad ShaikhNoch keine Bewertungen

- SCIENCE 5 PERFORMANCE TASKs 1-4 4th QuarterDokument3 SeitenSCIENCE 5 PERFORMANCE TASKs 1-4 4th QuarterBALETE100% (1)

- Aveva Installation GuideDokument48 SeitenAveva Installation GuideNico Van HoofNoch keine Bewertungen

- Wei Et Al 2016Dokument7 SeitenWei Et Al 2016Aline HunoNoch keine Bewertungen

- Expose Anglais TelephoneDokument6 SeitenExpose Anglais TelephoneAlexis SoméNoch keine Bewertungen

- EE114-1 Homework 2: Building Electrical SystemsDokument2 SeitenEE114-1 Homework 2: Building Electrical SystemsGuiaSanchezNoch keine Bewertungen

- Project Final Report: Crop BreedingDokument16 SeitenProject Final Report: Crop BreedingAniket PatilNoch keine Bewertungen

- Sheet (1) : An Iron Ring Has A Cross-Sectional Area of 3 CMDokument2 SeitenSheet (1) : An Iron Ring Has A Cross-Sectional Area of 3 CMKhalifa MohamedNoch keine Bewertungen

- Publications FireSafetyDesign SDokument369 SeitenPublications FireSafetyDesign SJayachandra Reddy AnnavaramNoch keine Bewertungen

- The Collected Letters of Flann O'BrienDokument640 SeitenThe Collected Letters of Flann O'BrienSean MorrisNoch keine Bewertungen

- ABRAMS M H The Fourth Dimension of A PoemDokument17 SeitenABRAMS M H The Fourth Dimension of A PoemFrancyne FrançaNoch keine Bewertungen