Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- What The CEO Wants You To KnowDokument8 SeitenWhat The CEO Wants You To KnowDilfaraz Kalawat100% (5)

- Discharge of ContractDokument53 SeitenDischarge of ContractDilfaraz Kalawat79% (14)

- Discharge of ContractDokument53 SeitenDischarge of ContractDilfaraz Kalawat79% (14)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Legality of Object and ConsiderationDokument8 SeitenLegality of Object and ConsiderationDilfaraz KalawatNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Merger Model Sample BIWS JobSearchDigestDokument7 SeitenMerger Model Sample BIWS JobSearchDigestCCerberus24Noch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Negotiable Instruments ActDokument21 SeitenNegotiable Instruments ActDilfaraz KalawatNoch keine Bewertungen

- Financial Statements AnalysisDokument18 SeitenFinancial Statements AnalysisDilfaraz KalawatNoch keine Bewertungen

- World Class ManufacturingDokument36 SeitenWorld Class ManufacturingDilfaraz KalawatNoch keine Bewertungen

- Tally AssignmentDokument90 SeitenTally AssignmentSHAHULNoch keine Bewertungen

- DINAGTUAN Rhonalyn Installment LiquidationDokument20 SeitenDINAGTUAN Rhonalyn Installment LiquidationRhad EstoqueNoch keine Bewertungen

- Petition For Extrajudicial Foreclosure (Template)Dokument6 SeitenPetition For Extrajudicial Foreclosure (Template)RA MlionNoch keine Bewertungen

- Manufacturing Accounts FormatDokument7 SeitenManufacturing Accounts Formatlaguda babajide100% (10)

- Legality of Object and ConsiderationDokument6 SeitenLegality of Object and ConsiderationDilfaraz Kalawat100% (6)

- Legality of Object and ConsiderationDokument6 SeitenLegality of Object and ConsiderationDilfaraz Kalawat100% (6)

- Free ConsentDokument77 SeitenFree ConsentDilfaraz KalawatNoch keine Bewertungen

- Free ConsentDokument77 SeitenFree ConsentDilfaraz KalawatNoch keine Bewertungen

- 08 - Advances, Deposits, Prepayments and Other ReceivablesDokument4 Seiten08 - Advances, Deposits, Prepayments and Other ReceivablesAqib SheikhNoch keine Bewertungen

- Pagcor Vs BirDokument5 SeitenPagcor Vs BirClarisse Ann MirandaNoch keine Bewertungen

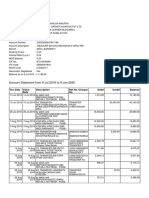

- Account Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument4 SeitenAccount Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancemauryapiaeNoch keine Bewertungen

- Performance TaskDokument3 SeitenPerformance TaskAnne Esguerra80% (5)

- Road Ahead For FinTech in IndiaDokument68 SeitenRoad Ahead For FinTech in IndiaAjith AjithNoch keine Bewertungen

- Guide To Understanding Financial Reporting QualityDokument5 SeitenGuide To Understanding Financial Reporting QualityDilfaraz KalawatNoch keine Bewertungen

- Time Is Neutral and Does Not ChangeDokument28 SeitenTime Is Neutral and Does Not ChangeDilfaraz KalawatNoch keine Bewertungen

- Open Economy MacroeconomicsDokument96 SeitenOpen Economy MacroeconomicsDilfaraz KalawatNoch keine Bewertungen

- Working Capital Cash Flow - Iimb FnfeDokument22 SeitenWorking Capital Cash Flow - Iimb FnfeDilfaraz KalawatNoch keine Bewertungen

- Osd What Is An IonDokument20 SeitenOsd What Is An IonDilfaraz KalawatNoch keine Bewertungen

- Defered TaxDokument2 SeitenDefered TaxDilfaraz KalawatNoch keine Bewertungen

- FSA RatiosDokument10 SeitenFSA RatiosDilfaraz KalawatNoch keine Bewertungen

- Fairway Corporation Balance Sheet Share Capital ReservesDokument4 SeitenFairway Corporation Balance Sheet Share Capital ReservesDilfaraz KalawatNoch keine Bewertungen

- Corporate ValuationDokument18 SeitenCorporate ValuationDilfaraz Kalawat100% (1)

- The Indian Contract Act 1872Dokument20 SeitenThe Indian Contract Act 1872Dilfaraz KalawatNoch keine Bewertungen

- Capital BudgetingDokument18 SeitenCapital BudgetingDilfaraz KalawatNoch keine Bewertungen

- Note On Consumer Protection ActDokument4 SeitenNote On Consumer Protection Actreadytogo1Noch keine Bewertungen

- Competent Employees IntroductionDokument10 SeitenCompetent Employees IntroductionDilfaraz KalawatNoch keine Bewertungen

- Consumer Protection Act, 1986Dokument34 SeitenConsumer Protection Act, 1986dreamza2z50% (2)

- Free ConsentDokument29 SeitenFree ConsentDilfaraz KalawatNoch keine Bewertungen

- The Indian Contract Act 1872Dokument47 SeitenThe Indian Contract Act 1872Dilfaraz KalawatNoch keine Bewertungen

- Consumer Protection Act, 1986Dokument34 SeitenConsumer Protection Act, 1986dreamza2z50% (2)

- The Indian Contract ActDokument16 SeitenThe Indian Contract ActArnold100% (1)

- Canara Bank & ING BankDokument26 SeitenCanara Bank & ING BankAmey ManchekarNoch keine Bewertungen

- 1ST Grading ExamDokument12 Seiten1ST Grading ExamJEFFERSON CUTENoch keine Bewertungen

- RP-425-GC: Application For Extension of 2020 Enhanced STAR DeadlineDokument2 SeitenRP-425-GC: Application For Extension of 2020 Enhanced STAR DeadlineSam WasserNoch keine Bewertungen

- Philippine Credit Card Authorization FormDokument1 SeitePhilippine Credit Card Authorization FormJack Roquid RodriguezNoch keine Bewertungen

- Chapter07 MCBDokument54 SeitenChapter07 MCBanjney050592Noch keine Bewertungen

- Financial Plan (Safari Internet CafeDokument4 SeitenFinancial Plan (Safari Internet CafeKealeboga Duece Thobolo100% (1)

- Behavioural Analysis of Individual Investors Towards Selection of Mutual Fund Schemes: An Empirical StudyDokument7 SeitenBehavioural Analysis of Individual Investors Towards Selection of Mutual Fund Schemes: An Empirical StudyAlphonseGeorgeNoch keine Bewertungen

- Procedure CFVDokument13 SeitenProcedure CFVNDTInstructorNoch keine Bewertungen

- Aguinaldo Industries V CirDokument1 SeiteAguinaldo Industries V CirChristine JacintoNoch keine Bewertungen

- Fact Finding - UT TakafulDokument1 SeiteFact Finding - UT TakafulcaptkhairulnizamNoch keine Bewertungen

- 10 - Chapter 1 PDFDokument34 Seiten10 - Chapter 1 PDFRitesh RamanNoch keine Bewertungen

- Mardia Chemicals Ltd. V Union of India Case SummaryDokument132 SeitenMardia Chemicals Ltd. V Union of India Case SummaryBrijesh50% (2)

- Taxfinalquiz 4Dokument67 SeitenTaxfinalquiz 4Aeron Rai RoqueNoch keine Bewertungen

- Importance of Capital StructureDokument2 SeitenImportance of Capital StructureShruti JoseNoch keine Bewertungen

- Appendic 5C-1 - Summarized Disclosure ChecklistDokument8 SeitenAppendic 5C-1 - Summarized Disclosure ChecklistLuis Enrique Altamar RamosNoch keine Bewertungen

- CS Project Report-Forex ManagementDokument32 SeitenCS Project Report-Forex ManagementAkriti PathakNoch keine Bewertungen

- Finals Quiz 2 Installment SalesDokument1 SeiteFinals Quiz 2 Installment SalesAdam SmithNoch keine Bewertungen

- Lecture 8 - LiquidationDokument30 SeitenLecture 8 - LiquidationSaurabh AroraNoch keine Bewertungen

- Paid Sick Leave MemoDokument4 SeitenPaid Sick Leave Memodharry8108Noch keine Bewertungen

- 811ffa 10363313 INV 2021 17655Dokument1 Seite811ffa 10363313 INV 2021 17655arjun singhaNoch keine Bewertungen