Das könnte Ihnen auch gefallen

- TMF - A Quick Look at Ethan Allen - Ethan Allen Interiors IncDokument4 SeitenTMF - A Quick Look at Ethan Allen - Ethan Allen Interiors InccasefortrilsNoch keine Bewertungen

- Planet Fitness, Inc. Announces Fourth Quarter and Fiscal Year 2016 ResultsDokument12 SeitenPlanet Fitness, Inc. Announces Fourth Quarter and Fiscal Year 2016 ResultscasefortrilsNoch keine Bewertungen

- EMH To Behavioral Finance - ShillerDokument44 SeitenEMH To Behavioral Finance - ShillerrexyfloydNoch keine Bewertungen

- SSRN Id313681Dokument48 SeitenSSRN Id313681casefortrilsNoch keine Bewertungen

- Korean Stock TradingDokument5 SeitenKorean Stock TradingcasefortrilsNoch keine Bewertungen

- SSRN Id283699Dokument50 SeitenSSRN Id283699casefortrilsNoch keine Bewertungen

- Company Stock in 401 (K) Plans: Corresponding AuthorDokument51 SeitenCompany Stock in 401 (K) Plans: Corresponding AuthorcasefortrilsNoch keine Bewertungen

- International Stock Trading - Fidelity InvestmentsDokument4 SeitenInternational Stock Trading - Fidelity InvestmentscasefortrilsNoch keine Bewertungen

- The Capital Asset Pricing Model - Theory and EvidenceDokument35 SeitenThe Capital Asset Pricing Model - Theory and Evidenceangelcomputer2Noch keine Bewertungen

- SSRN Id330540Dokument10 SeitenSSRN Id330540casefortrilsNoch keine Bewertungen

- SSRN Id316569Dokument52 SeitenSSRN Id316569casefortrilsNoch keine Bewertungen

- SSRN Id327880Dokument77 SeitenSSRN Id327880casefortrilsNoch keine Bewertungen

- 2015 0604 Arete Asset Management Policy Myths Reconnecting Investors With Useful InsightsDokument3 Seiten2015 0604 Arete Asset Management Policy Myths Reconnecting Investors With Useful InsightscasefortrilsNoch keine Bewertungen

- 2015 0606 Mauldin Economics Thoughts From The Frontline Cleaning Out The AtticDokument10 Seiten2015 0606 Mauldin Economics Thoughts From The Frontline Cleaning Out The AtticcasefortrilsNoch keine Bewertungen

- 2015 0602 Is The Stock Market CheapDokument9 Seiten2015 0602 Is The Stock Market CheapcasefortrilsNoch keine Bewertungen

- 2015 0602 - Is The Stock Market Cheap - Advisor Perspectives (DshortDokument9 Seiten2015 0602 - Is The Stock Market Cheap - Advisor Perspectives (DshortcasefortrilsNoch keine Bewertungen

- 2015 0602 Franklin Templeton Investments State of Emerging Markets All About Those Central BanksDokument5 Seiten2015 0602 Franklin Templeton Investments State of Emerging Markets All About Those Central BankscasefortrilsNoch keine Bewertungen

- 2015 0606 - Cleaning Out The Attic - Mauldin EconomicsDokument6 Seiten2015 0606 - Cleaning Out The Attic - Mauldin EconomicscasefortrilsNoch keine Bewertungen

- 2015 0528 Burt Malkiel WaveFront Capital MGMT How Much Should We Invest in Emerging MarketsDokument11 Seiten2015 0528 Burt Malkiel WaveFront Capital MGMT How Much Should We Invest in Emerging MarketscasefortrilsNoch keine Bewertungen

- 2015 0623 Nuveen Asset Management Equities Gather Momentum On Positive IndicatorsDokument4 Seiten2015 0623 Nuveen Asset Management Equities Gather Momentum On Positive IndicatorscasefortrilsNoch keine Bewertungen

- 2015 0622 Dynamika Capital Greece Implications For Global CarryDokument2 Seiten2015 0622 Dynamika Capital Greece Implications For Global CarrycasefortrilsNoch keine Bewertungen

- 2015 0622 Research Affiliates Greek Drama Act 2Dokument6 Seiten2015 0622 Research Affiliates Greek Drama Act 2casefortrilsNoch keine Bewertungen

- Daily Dirtnap v6-223 (2014 12)Dokument3 SeitenDaily Dirtnap v6-223 (2014 12)casefortrilsNoch keine Bewertungen

- 2015 0622 - Lord Abbett - Stocks - A Wary Good Sign For BullsDokument2 Seiten2015 0622 - Lord Abbett - Stocks - A Wary Good Sign For BullscasefortrilsNoch keine Bewertungen

- 2015 0614 - The People's Republic of Debt - Mauldin EconomicsDokument11 Seiten2015 0614 - The People's Republic of Debt - Mauldin EconomicscasefortrilsNoch keine Bewertungen

- Daily Dirtnap v4-141 (2012 08)Dokument3 SeitenDaily Dirtnap v4-141 (2012 08)casefortrilsNoch keine Bewertungen

- 2015 0622 Hale Stewart Us Equity and Economic Review For The Week of June 15 19 Better News But Still A Touch SlogDokument11 Seiten2015 0622 Hale Stewart Us Equity and Economic Review For The Week of June 15 19 Better News But Still A Touch SlogcasefortrilsNoch keine Bewertungen

- Daily Dirtnap v6-195 (2014 10)Dokument3 SeitenDaily Dirtnap v6-195 (2014 10)casefortrilsNoch keine Bewertungen

- Daily Dirtnap v6-168 (2014 09)Dokument3 SeitenDaily Dirtnap v6-168 (2014 09)casefortrilsNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- 1 - ST Benedicts Teaching Hospital - Case QuestionsDokument1 Seite1 - ST Benedicts Teaching Hospital - Case QuestionsJM LopezNoch keine Bewertungen

- 3rdyr - 1stF - Accounting For Business Combinations - 2324Dokument34 Seiten3rdyr - 1stF - Accounting For Business Combinations - 2324zaounxosakubNoch keine Bewertungen

- 2006 Loeys, J., Exploiting Cross-Market MomentumDokument16 Seiten2006 Loeys, J., Exploiting Cross-Market MomentumArthur FournierNoch keine Bewertungen

- Accounting For Corporations IIDokument25 SeitenAccounting For Corporations IIibrahim mohamedNoch keine Bewertungen

- Accounting Short Question and AnswersDokument4 SeitenAccounting Short Question and AnswersMalik Naseer AwanNoch keine Bewertungen

- Apollo HospitalsDokument18 SeitenApollo HospitalsvishalNoch keine Bewertungen

- Islamic Bonds: Learning ObjectivesDokument20 SeitenIslamic Bonds: Learning ObjectivesAbdelnasir HaiderNoch keine Bewertungen

- Mas - Final Preboard-Plv ExamDokument12 SeitenMas - Final Preboard-Plv ExamRed YuNoch keine Bewertungen

- SIM Audit 421 Problem Week 4-5Dokument33 SeitenSIM Audit 421 Problem Week 4-5Kristelle MarieNoch keine Bewertungen

- Axis Bank (Buy at CMP: 719) Target 875-910, SL-640 Time Frame 9-24 MonthsDokument51 SeitenAxis Bank (Buy at CMP: 719) Target 875-910, SL-640 Time Frame 9-24 MonthsMaruthee SharmaNoch keine Bewertungen

- Optimize futures hedging with multi-period purchasesDokument26 SeitenOptimize futures hedging with multi-period purchasesvivekNoch keine Bewertungen

- CapitalCube - GBDC - GBDC US Company Reports - 4 PagesDokument4 SeitenCapitalCube - GBDC - GBDC US Company Reports - 4 PagesSagar PatelNoch keine Bewertungen

- Entrepreneurship: Dr. Akshita JainDokument137 SeitenEntrepreneurship: Dr. Akshita JainSALONI JAINNoch keine Bewertungen

- Chapter 8: An Introduction To Asset Pricing ModelsDokument43 SeitenChapter 8: An Introduction To Asset Pricing ModelsMohana KrishnaNoch keine Bewertungen

- Influencer Marketing Proposal 5Dokument11 SeitenInfluencer Marketing Proposal 5Paul0% (1)

- How We Trade OptionsDokument21 SeitenHow We Trade Optionslecee01100% (1)

- ECMT2130: Semester 2, 2020 Assignment: Geoff Shuetrim Geoffrey - Shuetrim@sydney - Edu.au University of SydneyDokument7 SeitenECMT2130: Semester 2, 2020 Assignment: Geoff Shuetrim Geoffrey - Shuetrim@sydney - Edu.au University of SydneyDaniyal AsifNoch keine Bewertungen

- Week 1 GroupDokument2 SeitenWeek 1 GroupConner Becker100% (1)

- PAPER F3 Financial StrategyDokument3 SeitenPAPER F3 Financial StrategyIzzawah YawNoch keine Bewertungen

- Calculate Value at Risk (VaR) for a diversified portfolioDokument11 SeitenCalculate Value at Risk (VaR) for a diversified portfolioRashmiroja SahuNoch keine Bewertungen

- Business Valuation Using Financial Statements (BVFS) Prof. Vaidya Nathan Term 6, February 2022Dokument242 SeitenBusiness Valuation Using Financial Statements (BVFS) Prof. Vaidya Nathan Term 6, February 2022Anurag JainNoch keine Bewertungen

- Recognition and MeasurementDokument16 SeitenRecognition and MeasurementajishNoch keine Bewertungen

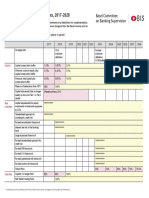

- Basel III transitional arrangements 2017-2028 summaryDokument1 SeiteBasel III transitional arrangements 2017-2028 summarygoonNoch keine Bewertungen

- National University of Science and TechnologyDokument8 SeitenNational University of Science and TechnologyPATIENCE MUSHONGANoch keine Bewertungen

- Dresdner Struct Products Vicious CircleDokument8 SeitenDresdner Struct Products Vicious CircleBoris MangalNoch keine Bewertungen

- Semi Final Exam EntrepDokument3 SeitenSemi Final Exam EntrepEricson C UngriaNoch keine Bewertungen

- SEFL AnnexureDokument1 SeiteSEFL AnnexureBalakrishna AnkayyaNoch keine Bewertungen

- MCQ 501Dokument90 SeitenMCQ 501haqmalNoch keine Bewertungen

- Analyisis Report Tesla Statement of ConditionDokument13 SeitenAnalyisis Report Tesla Statement of ConditionAmel BarghutiNoch keine Bewertungen

- Subjects Chapters DOC: I) Ethical and Professional Standards 1.ethics and Trust in The Investment ProfessionDokument2 SeitenSubjects Chapters DOC: I) Ethical and Professional Standards 1.ethics and Trust in The Investment ProfessionHanako ChinatsuNoch keine Bewertungen