Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Nubank: A Brazilian FinTech Worth $10 Billion - MEDICIDokument25 SeitenNubank: A Brazilian FinTech Worth $10 Billion - MEDICIKay BarnesNoch keine Bewertungen

- PWC Insurance BrokerageDokument28 SeitenPWC Insurance BrokerageAbhinav Walia100% (1)

- Challenges: Need One Bank Licensing Policy, But Several Bank LicensingpoliciesDokument8 SeitenChallenges: Need One Bank Licensing Policy, But Several Bank LicensingpoliciesAbhinav WaliaNoch keine Bewertungen

- Wholesale Global Directory 2015 PDFDokument144 SeitenWholesale Global Directory 2015 PDFBarry Manlay100% (1)

- ElectronicCheck TutorialsDokument30 SeitenElectronicCheck Tutorialsluanasantts81100% (1)

- Cyber Security AwarenessDokument23 SeitenCyber Security Awarenessnilesh100% (1)

- Britannia Nutrichoice Case StudyDokument18 SeitenBritannia Nutrichoice Case StudyAbhinav WaliaNoch keine Bewertungen

- Survey Sucess With KinnserDokument12 SeitenSurvey Sucess With KinnserKinnser SoftwareNoch keine Bewertungen

- MOCN KPI Formulas - v2Dokument71 SeitenMOCN KPI Formulas - v2anwarfaesolNoch keine Bewertungen

- SantanderDokument1 SeiteSantanderKabanNoch keine Bewertungen

- State Life Internship Report, Usman Ali HCBFDokument134 SeitenState Life Internship Report, Usman Ali HCBFUSMAN254082% (38)

- Huawei SPS Convergent Solution For IPSTP and DA v1.0Dokument53 SeitenHuawei SPS Convergent Solution For IPSTP and DA v1.0aranibarmNoch keine Bewertungen

- Tractors Article Sep14Dokument7 SeitenTractors Article Sep14Abhinav WaliaNoch keine Bewertungen

- The Indian Tractor Industry - Bumpy Road AheadDokument3 SeitenThe Indian Tractor Industry - Bumpy Road AheadSanjana AcharyaNoch keine Bewertungen

- SB Whitepaper AutomotivecrmDokument8 SeitenSB Whitepaper AutomotivecrmAbhinav WaliaNoch keine Bewertungen

- Small To Big Marketing Makes It Possible: The Basics of Rural MarketingDokument2 SeitenSmall To Big Marketing Makes It Possible: The Basics of Rural MarketingAbhinav WaliaNoch keine Bewertungen

- ContentServer - 3 COMPANY PROFILE Escorts Limited 2014Dokument9 SeitenContentServer - 3 COMPANY PROFILE Escorts Limited 2014Abhinav WaliaNoch keine Bewertungen

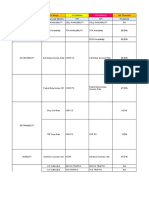

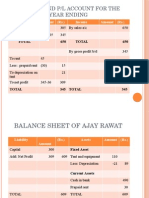

- Trading and P/L Account For The Year Ending: Expense Amount (RS.) Income Amount (RS.)Dokument2 SeitenTrading and P/L Account For The Year Ending: Expense Amount (RS.) Income Amount (RS.)Abhinav WaliaNoch keine Bewertungen

- Corporate Heads: Industry Company Name DesignationDokument2 SeitenCorporate Heads: Industry Company Name DesignationAbhinav WaliaNoch keine Bewertungen

- Corporate PresentationDokument45 SeitenCorporate PresentationAbhinav WaliaNoch keine Bewertungen

- IoT Messaging ProtocolsDokument58 SeitenIoT Messaging ProtocolsPranjal YadavNoch keine Bewertungen

- RBFDokument8 SeitenRBFPankaj KamraNoch keine Bewertungen

- White Paper: Case Study: The Home Depot Data BreachDokument19 SeitenWhite Paper: Case Study: The Home Depot Data BreachDiksha PanditNoch keine Bewertungen

- Distribution: Service Marketing MixDokument4 SeitenDistribution: Service Marketing MixArch 2017-22Noch keine Bewertungen

- IMT Ghaziabad - Ujjawal - 18.02.23Dokument28 SeitenIMT Ghaziabad - Ujjawal - 18.02.23Kartik SharmaNoch keine Bewertungen

- LTC Procedural Norms PDFDokument5 SeitenLTC Procedural Norms PDFsk_kannan26Noch keine Bewertungen

- Nepal Telecommunications Authority: MIS ReportDokument12 SeitenNepal Telecommunications Authority: MIS ReportRaMesh AdhikariNoch keine Bewertungen

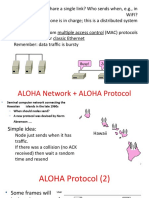

- Notes 5b Aloha ProtocolDokument58 SeitenNotes 5b Aloha ProtocolThe UnCONFUSEDNoch keine Bewertungen

- Account Statement From 1 Aug 2018 To 31 Aug 2018: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument6 SeitenAccount Statement From 1 Aug 2018 To 31 Aug 2018: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancePradeep Singh PanwarNoch keine Bewertungen

- Accenture Sustainable Mile POVDokument24 SeitenAccenture Sustainable Mile POVDaniel PazNoch keine Bewertungen

- Chapter 1 Digital Communication - CompressedDokument46 SeitenChapter 1 Digital Communication - CompressedToluwani AyubaNoch keine Bewertungen

- Construct and Ticket Domestic Airfares: D2.TTA - CL2.06 Trainee ManualDokument31 SeitenConstruct and Ticket Domestic Airfares: D2.TTA - CL2.06 Trainee ManualEdwin LolowangNoch keine Bewertungen

- PR4345 Government TransportDokument4 SeitenPR4345 Government TransportZairulNoch keine Bewertungen

- Quiz 1 - Intacc 2Dokument9 SeitenQuiz 1 - Intacc 2Eleina SwiftNoch keine Bewertungen

- A Report On Insurance Industry of NepalDokument7 SeitenA Report On Insurance Industry of NepaldeepNoch keine Bewertungen

- Sme BookDokument397 SeitenSme BookVivek Godgift J0% (1)

- Module 5 & 6Dokument48 SeitenModule 5 & 6JithuHashMi100% (1)

- Case Study: A Business Trip To BrusselsDokument10 SeitenCase Study: A Business Trip To BrusselsTarun SahaniyaNoch keine Bewertungen

- Club Lime - Member ShipDokument3 SeitenClub Lime - Member ShipCarlos Andrés Aristizabal MorenoNoch keine Bewertungen

- Ebay, Inc. SWOT Analysis.Dokument10 SeitenEbay, Inc. SWOT Analysis.vesperousNoch keine Bewertungen

- Grading Structure GesDokument7 SeitenGrading Structure Ges3944/95100% (1)