Das könnte Ihnen auch gefallen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Seidl NCBC08 Paper TR CorrectedDokument10 SeitenSeidl NCBC08 Paper TR CorrectedsajuhereNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- ASHRAE Journal - Tips To Reduce Chilled Water Plant Costs - TaylorDokument6 SeitenASHRAE Journal - Tips To Reduce Chilled Water Plant Costs - TaylorsajuhereNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- HPAC A Fresh Look at Fans-FinalDokument10 SeitenHPAC A Fresh Look at Fans-FinalsajuhereNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- ASHRAE Journal - Underfloor Lessons Learned-DalyDokument4 SeitenASHRAE Journal - Underfloor Lessons Learned-DalysajuhereNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- ASHRAE Journal - Select & Control Economizer Dampers in VAV Systems - TaylorDokument7 SeitenASHRAE Journal - Select & Control Economizer Dampers in VAV Systems - Taylorsajuhere100% (1)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- 8614 - ERP vs. Quality White PaperDokument3 Seiten8614 - ERP vs. Quality White PapersajuhereNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Leed FaqDokument4 SeitenLeed FaqsajuhereNoch keine Bewertungen

- ASHRAE Journal - How To Design & Control Waterside Economizers-TaylorDokument7 SeitenASHRAE Journal - How To Design & Control Waterside Economizers-TaylorsajuhereNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- MunicipalGreenBuildingOrdinance SussmanDokument15 SeitenMunicipalGreenBuildingOrdinance SussmansajuhereNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Energy Savings White PaperDokument14 SeitenEnergy Savings White PapersajuhereNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Industrial SecurityDokument71 SeitenIndustrial Securityharrison rojas64% (11)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- TTester 1.10k EN 140409-1Dokument89 SeitenTTester 1.10k EN 140409-1Domingo ArroyoNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- PPE ChecklistDokument3 SeitenPPE ChecklistAtique Ur Rehman KhattakNoch keine Bewertungen

- Math Samples PDFDokument1 SeiteMath Samples PDFArwin VillegasNoch keine Bewertungen

- SIEMENS Manfred Pohl 20120523cigre2012Dokument23 SeitenSIEMENS Manfred Pohl 20120523cigre2012suraiyya begumNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Saudi Aramco Test Report: SATR-P-3210 3-Jul-18 Elect-Medium Voltage Power Cable, High-Potential Withstand TestingDokument10 SeitenSaudi Aramco Test Report: SATR-P-3210 3-Jul-18 Elect-Medium Voltage Power Cable, High-Potential Withstand Testingkarthi51289Noch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Lotus TravelerDokument43 SeitenLotus Travelersyedmn21Noch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Project Report: Digital Logic DesignsDokument17 SeitenProject Report: Digital Logic DesignsSiddique FarooqNoch keine Bewertungen

- Bank StatmentDokument10 SeitenBank StatmentSivakumar ThangarajanNoch keine Bewertungen

- Pavan Tools Catalog 2012Dokument76 SeitenPavan Tools Catalog 2012Pavan ToolsNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Voltage Drop Affects The Operation of Induction MachinesDokument3 SeitenVoltage Drop Affects The Operation of Induction MachinesAnonymous oZdAPQdIJNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- ProjectDokument5 SeitenProjectDeepak KesharwaniNoch keine Bewertungen

- Design Based Comparative Study of Several Condensers Ijariie2142 PDFDokument7 SeitenDesign Based Comparative Study of Several Condensers Ijariie2142 PDFFranceNoch keine Bewertungen

- Regular Expressions in QTPDokument15 SeitenRegular Expressions in QTPBhargav S RajendraNoch keine Bewertungen

- John Scofield Trio Rider With Stewart and Swallow Web Rider-1405457761Dokument8 SeitenJohn Scofield Trio Rider With Stewart and Swallow Web Rider-1405457761diablichoNoch keine Bewertungen

- ICT-CHS Grade 9Dokument6 SeitenICT-CHS Grade 9LILEBELLE BALDOVENoch keine Bewertungen

- 2016-04 DIAMETER ArchitectureDokument22 Seiten2016-04 DIAMETER ArchitectureVivek ShahNoch keine Bewertungen

- SasaDokument20 SeitenSasaSpinu AlexandruNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Accounting Information SystemDokument2 SeitenAccounting Information SystemJansen Alonzo BordeyNoch keine Bewertungen

- History: Aviation Is The Practical Aspect or Art ofDokument3 SeitenHistory: Aviation Is The Practical Aspect or Art ofEarle J ZaficoNoch keine Bewertungen

- Catalogue TD InsulatorsDokument26 SeitenCatalogue TD InsulatorsBery HamidNoch keine Bewertungen

- QAP For Pipes For Hydrant and Sprinkler SystemDokument3 SeitenQAP For Pipes For Hydrant and Sprinkler SystemCaspian DattaNoch keine Bewertungen

- Agilent Phase-Noise-Measurement TES-E5052B DatasheetDokument21 SeitenAgilent Phase-Noise-Measurement TES-E5052B DatasheetTeq ShoNoch keine Bewertungen

- Bus Switching Scheme PDFDokument6 SeitenBus Switching Scheme PDFJAYKUMAR SINGHNoch keine Bewertungen

- Passive Trap Filter For Harmonic ReductionDokument9 SeitenPassive Trap Filter For Harmonic ReductionShiva KumarNoch keine Bewertungen

- 5GHz VCODokument5 Seiten5GHz VCOnavinrkNoch keine Bewertungen

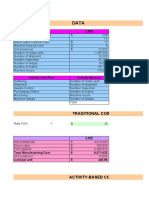

- Traditional Costing: Activity Cost Pool Activity MeasureDokument4 SeitenTraditional Costing: Activity Cost Pool Activity Measureyola yufitanNoch keine Bewertungen

- Solid Fuel Boiler Control Standard 2: Version 1.0) Version 1.0) Version 1.0) Version 1.0)Dokument26 SeitenSolid Fuel Boiler Control Standard 2: Version 1.0) Version 1.0) Version 1.0) Version 1.0)Ana Odzaklieska Krste SmileskiNoch keine Bewertungen

- Bc250mo PDS Reg - Europe en V8 PDS Eur 24537 10012335Dokument3 SeitenBc250mo PDS Reg - Europe en V8 PDS Eur 24537 10012335Fahad AliNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Fluke T3 Voltage and Continuity TesterDokument2 SeitenFluke T3 Voltage and Continuity Testerkoko MeNoch keine Bewertungen