Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Adjusting Entries QuizDokument12 SeitenAdjusting Entries QuizJuan Dela CruzNoch keine Bewertungen

- Grade11 Fabm1 Q2 Week1Dokument22 SeitenGrade11 Fabm1 Q2 Week1Mickaela MonterolaNoch keine Bewertungen

- BBFA1103 Introductory Accounting - Eaug20Dokument336 SeitenBBFA1103 Introductory Accounting - Eaug20Vivi50% (2)

- Accounting Adjusting EntryDokument20 SeitenAccounting Adjusting EntryClemencia Masiba100% (1)

- Penn Foster 06101501 Financial Accounting Exam Parts 1 and 2 Manville and Coleman-FooseDokument3 SeitenPenn Foster 06101501 Financial Accounting Exam Parts 1 and 2 Manville and Coleman-FooseMike RussellNoch keine Bewertungen

- Acctg Assginment 4 Adjusting EntriesDokument3 SeitenAcctg Assginment 4 Adjusting EntriesDaisy Marie A. RoselNoch keine Bewertungen

- STR 581 Final Exam Capstone Part 2 Week 4Dokument9 SeitenSTR 581 Final Exam Capstone Part 2 Week 4Mike Russell100% (3)

- Linear Programming Model - Excel Solution Module3 - Complete Worksheet - P3-12 - P3-22 - P3-18Dokument2 SeitenLinear Programming Model - Excel Solution Module3 - Complete Worksheet - P3-12 - P3-22 - P3-18Mike Russell0% (1)

- ACCT 505 Managerial Accounting Week 2 Job Order and Process Costing Systems Quiz AnswerDokument10 SeitenACCT 505 Managerial Accounting Week 2 Job Order and Process Costing Systems Quiz AnswerMike RussellNoch keine Bewertungen

- Tax Return - Carrie A. Morgan, Age 45, Is Single and Lives With Her Dependent MotherDokument6 SeitenTax Return - Carrie A. Morgan, Age 45, Is Single and Lives With Her Dependent MotherMike RussellNoch keine Bewertungen

- STR 581 Final Exam Capstone Part 2 Week 4Dokument9 SeitenSTR 581 Final Exam Capstone Part 2 Week 4Mike Russell100% (3)

- FINANCE EXAM 3 The Hasting Company Began Operations On January 1, 2003Dokument7 SeitenFINANCE EXAM 3 The Hasting Company Began Operations On January 1, 2003Mike Russell50% (2)

- ECON 104 Homework 12 Why The Trade Deficit in The US Increased AnswerDokument3 SeitenECON 104 Homework 12 Why The Trade Deficit in The US Increased AnswerMike RussellNoch keine Bewertungen

- ACC 206 Week 4 Assignment Balance Sheet of Watson CompanyDokument3 SeitenACC 206 Week 4 Assignment Balance Sheet of Watson CompanyMike RussellNoch keine Bewertungen

- ECO 425 Homework 4 Complete A+ AnswerDokument2 SeitenECO 425 Homework 4 Complete A+ AnswerMike RussellNoch keine Bewertungen

- HSM 543 Health Services Finance Week 7 Course Project AnswerDokument64 SeitenHSM 543 Health Services Finance Week 7 Course Project AnswerMike RussellNoch keine Bewertungen

- Wise Company Completes These Transactions During April of The Current Year Journals Ledgers Receivable A+ AnswerDokument2 SeitenWise Company Completes These Transactions During April of The Current Year Journals Ledgers Receivable A+ AnswerMike Russell40% (5)

- Advance Payment of Revenues: Liability MethodDokument9 SeitenAdvance Payment of Revenues: Liability MethodDan Ryan100% (1)

- Chapter 4Dokument109 SeitenChapter 4nadima behzadNoch keine Bewertungen

- 3.1 Learning Objective 3-1: Chapter 3 Accrual Accounting & IncomeDokument75 Seiten3.1 Learning Objective 3-1: Chapter 3 Accrual Accounting & IncomeSeanNoch keine Bewertungen

- Answer Key - Quizzer On AJEDokument2 SeitenAnswer Key - Quizzer On AJEClarissa De GuzmanNoch keine Bewertungen

- Pacrim Careers Provides Training To Individuals Who Pay Tuition DirectlyDokument1 SeitePacrim Careers Provides Training To Individuals Who Pay Tuition DirectlyTaimour HassanNoch keine Bewertungen

- Adjusting EntriesDokument27 SeitenAdjusting EntrieskaiginNoch keine Bewertungen

- Sas Certified Accounting Technician Level 1 Module 2Dokument29 SeitenSas Certified Accounting Technician Level 1 Module 2Plame GaseroNoch keine Bewertungen

- Assignment Module 5Dokument2 SeitenAssignment Module 5Hazel Jane MejiaNoch keine Bewertungen

- Adjusting Entries: Fifth Step of The Accounting CycleDokument12 SeitenAdjusting Entries: Fifth Step of The Accounting CyclealtaNoch keine Bewertungen

- Key Terms Introduced or Emphasized in Chapter 4Dokument2 SeitenKey Terms Introduced or Emphasized in Chapter 4Faryal MughalNoch keine Bewertungen

- Chapter 3 Adjusting The AccountsDokument26 SeitenChapter 3 Adjusting The AccountsGeorgeNoch keine Bewertungen

- Chapter 3 Quick StudyDokument10 SeitenChapter 3 Quick StudyPhạm Hồng Trang Alice -Noch keine Bewertungen

- BTS Accounting Firm Trial Balance December 31, 2014Dokument4 SeitenBTS Accounting Firm Trial Balance December 31, 2014Trisha AlaNoch keine Bewertungen

- Tanauan Institute, Inc.: Adjustments For AccrualsDokument7 SeitenTanauan Institute, Inc.: Adjustments For AccrualsHanna CaraigNoch keine Bewertungen

- BFAR 11-04-2022 The Accounting Cycle 3 Adjusting EntriesDokument4 SeitenBFAR 11-04-2022 The Accounting Cycle 3 Adjusting EntriesSheryl cornelNoch keine Bewertungen

- Accounting Chapter 3 SummaryDokument7 SeitenAccounting Chapter 3 SummaryHariNoch keine Bewertungen

- Intermediate Accounting: Accounting Changes and Error AnalysisDokument87 SeitenIntermediate Accounting: Accounting Changes and Error Analysis12C1 LớpNoch keine Bewertungen

- 02 AddDokument14 Seiten02 AddHà My NguyễnNoch keine Bewertungen

- Reen LawnsDokument8 SeitenReen LawnsAshish BhallaNoch keine Bewertungen

- Adjusting Entry-Solutions of ExercisesDokument4 SeitenAdjusting Entry-Solutions of ExercisesSerazul Arafin MrinmoyNoch keine Bewertungen

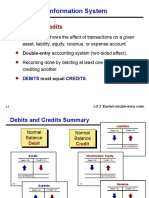

- Accounting Information System: Debits and CreditsDokument84 SeitenAccounting Information System: Debits and CreditsDavid Bradley BeckNoch keine Bewertungen

- CH3 AcctDokument13 SeitenCH3 AcctJillian LaluanNoch keine Bewertungen

- Integprac1 Quiz 3Dokument1 SeiteIntegprac1 Quiz 3AMARO, BABY LIZ ANDESNoch keine Bewertungen

- Chapter: Income Statement: - Adjusting EntriesDokument20 SeitenChapter: Income Statement: - Adjusting Entriesaishwarya joshiNoch keine Bewertungen

- Final Exam Preparation Auditing II: Condition Yang Terjadi Dan Mempengaruhi Akun-Akun Sebelum TanggalDokument5 SeitenFinal Exam Preparation Auditing II: Condition Yang Terjadi Dan Mempengaruhi Akun-Akun Sebelum TanggalAlvira FajriNoch keine Bewertungen