Das könnte Ihnen auch gefallen

- Asian Development Outlook 2015: Financing Asia’s Future GrowthVon EverandAsian Development Outlook 2015: Financing Asia’s Future GrowthNoch keine Bewertungen

- Private Debt in 2015Dokument8 SeitenPrivate Debt in 2015ed_nycNoch keine Bewertungen

- Databases Brief Introduction Coverage / Services / Products/ Contents User GuideDokument7 SeitenDatabases Brief Introduction Coverage / Services / Products/ Contents User GuideKrishnaNoch keine Bewertungen

- BARCLAYS - Global Credit Outlook 2016 - An Aging CycleDokument206 SeitenBARCLAYS - Global Credit Outlook 2016 - An Aging CyclenoobcatcherNoch keine Bewertungen

- Deutche Bank Doc 1 - Deutsche Bank at A GlanceDokument14 SeitenDeutche Bank Doc 1 - Deutsche Bank at A GlanceUriGrodNoch keine Bewertungen

- UBS Real Estate Outlook 2010Dokument32 SeitenUBS Real Estate Outlook 2010CRE Console100% (1)

- Nomura Report On ChinaDokument104 SeitenNomura Report On ChinaSimon LouieNoch keine Bewertungen

- UBS Debt Investr PresentationDokument36 SeitenUBS Debt Investr PresentationNacho DalmauNoch keine Bewertungen

- Bar Cap 3Dokument11 SeitenBar Cap 3Aquila99999Noch keine Bewertungen

- Ubs GlobalDokument24 SeitenUbs GlobalJoOANANoch keine Bewertungen

- Understanding Vietnam - A Look Beyond The Facts and PDFDokument24 SeitenUnderstanding Vietnam - A Look Beyond The Facts and PDFDawood GacayanNoch keine Bewertungen

- Deutsche BankDokument82 SeitenDeutsche BankFransiska SihalohoNoch keine Bewertungen

- An Investor's Guide To Inflation-Linked BondsDokument16 SeitenAn Investor's Guide To Inflation-Linked BondscoolaclNoch keine Bewertungen

- Sassaf Citi PresDokument29 SeitenSassaf Citi PresakiskefalasNoch keine Bewertungen

- Deutsche Bank Dr. Josef AckermannDokument32 SeitenDeutsche Bank Dr. Josef AckermannLuis Rguez. Del BarrioNoch keine Bewertungen

- DBQuantWeeklyDashboard - 2016 09 19 PDFDokument11 SeitenDBQuantWeeklyDashboard - 2016 09 19 PDFcastjamNoch keine Bewertungen

- UBS Research Year Ahead 2019 Report Global enDokument68 SeitenUBS Research Year Ahead 2019 Report Global enphilipw_15Noch keine Bewertungen

- Asia Maxima (Delirium) - 3Q14 20140703Dokument100 SeitenAsia Maxima (Delirium) - 3Q14 20140703Hans WidjajaNoch keine Bewertungen

- Euro Themes - SpainDokument22 SeitenEuro Themes - SpainGuy DviriNoch keine Bewertungen

- FX Daily Strategist: Europe: Foreign Exchange London: 8 February 2012 07:00 GMTDokument2 SeitenFX Daily Strategist: Europe: Foreign Exchange London: 8 February 2012 07:00 GMTzinxyNoch keine Bewertungen

- Bank Loans: Market Dynamics Poised To Deliver Attractive Risk-Adjusted ReturnsDokument6 SeitenBank Loans: Market Dynamics Poised To Deliver Attractive Risk-Adjusted ReturnsSabin NiculaeNoch keine Bewertungen

- Financial Reform: A Framework For Financial StabilityDokument29 SeitenFinancial Reform: A Framework For Financial Stabilityapi-26172897Noch keine Bewertungen

- Daily Breakfast Spread: EconomicsDokument6 SeitenDaily Breakfast Spread: EconomicsShou Yee WongNoch keine Bewertungen

- Modelling Cost at Risk - A Preliminary Approach - 0Dokument16 SeitenModelling Cost at Risk - A Preliminary Approach - 0Uzair Ul HaqNoch keine Bewertungen

- 10-Rules of Thumb - Morgan Stanley PDFDokument8 Seiten10-Rules of Thumb - Morgan Stanley PDFParas BholaNoch keine Bewertungen

- HSBC - Currency Outlook DecemberDokument46 SeitenHSBC - Currency Outlook Decembermgroble3Noch keine Bewertungen

- Economics Docs 2022 184258.ashxDokument65 SeitenEconomics Docs 2022 184258.ashxTshepo ThaisiNoch keine Bewertungen

- RBS On DowngradesDokument17 SeitenRBS On Downgradesharlock01Noch keine Bewertungen

- Investor Day IB FINALDokument24 SeitenInvestor Day IB FINALamadeo1985Noch keine Bewertungen

- Week Summary: Macro StrategyDokument10 SeitenWeek Summary: Macro StrategyNoel AndreottiNoch keine Bewertungen

- J.P. 摩根-美股-保险行业-2021年财险预览:商业再保险保险价格和自动频率顺风顺水-2021.1.4-83页Dokument85 SeitenJ.P. 摩根-美股-保险行业-2021年财险预览:商业再保险保险价格和自动频率顺风顺水-2021.1.4-83页HungNoch keine Bewertungen

- India Pharma Sector - Sector UpdateDokument142 SeitenIndia Pharma Sector - Sector Updatekushal-sinha-680Noch keine Bewertungen

- Foreign Exchange Daily ReportDokument5 SeitenForeign Exchange Daily ReportPrashanth Goud DharmapuriNoch keine Bewertungen

- 德银 全球投资策略之全球固定收益2021年展望:还需要迎头赶上 2020.12.22 110页Dokument112 Seiten德银 全球投资策略之全球固定收益2021年展望:还需要迎头赶上 2020.12.22 110页HungNoch keine Bewertungen

- Back-Testing Moody's LGD Methodology: June 2007Dokument16 SeitenBack-Testing Moody's LGD Methodology: June 2007maverickrzysNoch keine Bewertungen

- U.S. Large-Cap & Mid-Cap Banks - Drilling Into Energy ExposureDokument39 SeitenU.S. Large-Cap & Mid-Cap Banks - Drilling Into Energy ExposureMartin TsankovNoch keine Bewertungen

- Unicredit CEE Quarterly 4Q2019Dokument76 SeitenUnicredit CEE Quarterly 4Q2019Sorin DinuNoch keine Bewertungen

- Interest Rates - An IntroductionDokument186 SeitenInterest Rates - An IntroductionAamirNoch keine Bewertungen

- Deutsche BankDokument23 SeitenDeutsche Bankmichelerovatti0% (1)

- SBI Equity Savings Fund - Presentation PDFDokument23 SeitenSBI Equity Savings Fund - Presentation PDFPankaj RastogiNoch keine Bewertungen

- CPI SJ - A Critique On Credit Risks & ROE - Solid Footing But We Maintain Our HOLD On Valuation RiskDokument16 SeitenCPI SJ - A Critique On Credit Risks & ROE - Solid Footing But We Maintain Our HOLD On Valuation RiskMukarangaNoch keine Bewertungen

- Economic and Industry Analysis Co Combined 9-2010Dokument62 SeitenEconomic and Industry Analysis Co Combined 9-2010Rohit BansalNoch keine Bewertungen

- Global Market Outlook - August 2013 - GWMDokument14 SeitenGlobal Market Outlook - August 2013 - GWMFauzi DjauhariNoch keine Bewertungen

- CDS Bond BasisDokument41 SeitenCDS Bond BasisSharad DuttaNoch keine Bewertungen

- UBS Business Plan - Stategic Planning and Financing Basis - Model For Generating A Business Plan - (UBS AG) PDFDokument26 SeitenUBS Business Plan - Stategic Planning and Financing Basis - Model For Generating A Business Plan - (UBS AG) PDFQuantDev-MNoch keine Bewertungen

- ECON 351-International Trade-Turab HussainDokument6 SeitenECON 351-International Trade-Turab HussainshyasirNoch keine Bewertungen

- Barclays Oil ReportDokument55 SeitenBarclays Oil ReportGargar100% (1)

- (Routledge Focus On Economics and Finance) Arif Orçun Söylemez - Foreign Exchange Rates - A Research Overview of The Latest Prediction Techniques (2021, Routledge)Dokument83 Seiten(Routledge Focus On Economics and Finance) Arif Orçun Söylemez - Foreign Exchange Rates - A Research Overview of The Latest Prediction Techniques (2021, Routledge)Archie GaloNoch keine Bewertungen

- PzenaCommentary Second Quarter 2013Dokument3 SeitenPzenaCommentary Second Quarter 2013CanadianValueNoch keine Bewertungen

- Chile Handbook PDFDokument106 SeitenChile Handbook PDFAlejandro Quezada VerdugoNoch keine Bewertungen

- NCBC SaudiFactbook 2012Dokument232 SeitenNCBC SaudiFactbook 2012vineet_bmNoch keine Bewertungen

- Mutual Funds Sahi HaiDokument24 SeitenMutual Funds Sahi Haishiva1602Noch keine Bewertungen

- 2016 Year in VolatilityDokument18 Seiten2016 Year in Volatilitychris mbaNoch keine Bewertungen

- Capital Structure ToolkitDokument132 SeitenCapital Structure ToolkitOwen100% (1)

- 48 - IEW March 2014Dokument13 Seiten48 - IEW March 2014girishrajsNoch keine Bewertungen

- ALCO and Operational Risk Management at Bank of ChinaDokument17 SeitenALCO and Operational Risk Management at Bank of ChinaAbrar100% (1)

- Goldman Sachs Risk Management: November 17 2010 Presented By: Ken Forsyth Jeremy Poon Jamie MacdonaldDokument109 SeitenGoldman Sachs Risk Management: November 17 2010 Presented By: Ken Forsyth Jeremy Poon Jamie MacdonaldPol BernardinoNoch keine Bewertungen

- JPM Cap Intro 2011Dokument32 SeitenJPM Cap Intro 2011mdorneanuNoch keine Bewertungen

- Investment Consulting Business PlanDokument9 SeitenInvestment Consulting Business Planbe_supercoolNoch keine Bewertungen

- Topic 21 - Credit Risks and Credit Derivatives QuestionDokument10 SeitenTopic 21 - Credit Risks and Credit Derivatives QuestionRajat CNoch keine Bewertungen

- Operational Due Dilligence v2Dokument4 SeitenOperational Due Dilligence v2Rajat CNoch keine Bewertungen

- Topic 18 To 19 Question PDFDokument3 SeitenTopic 18 To 19 Question PDFRajat CNoch keine Bewertungen

- Industry Analysis PDFDokument25 SeitenIndustry Analysis PDFRajat CNoch keine Bewertungen

- Edhec Fund of Hedge PDFDokument32 SeitenEdhec Fund of Hedge PDFRajat CNoch keine Bewertungen

- Edhec Fund of Hedge PDFDokument32 SeitenEdhec Fund of Hedge PDFRajat CNoch keine Bewertungen

- Edhec Fund of Hedge PDFDokument32 SeitenEdhec Fund of Hedge PDFRajat CNoch keine Bewertungen

- 2013 Deutsche Bank Operational Due Diligence SurveyDokument48 Seiten2013 Deutsche Bank Operational Due Diligence SurveyRajat CNoch keine Bewertungen

- Preqin Investor Outlook Alternative Assets H1 2015Dokument50 SeitenPreqin Investor Outlook Alternative Assets H1 2015Rajat CNoch keine Bewertungen

- Mutual FundsDokument32 SeitenMutual Fundsapi-309082881Noch keine Bewertungen

- CustomSTMT2020Jan01 2020mar15Dokument4 SeitenCustomSTMT2020Jan01 2020mar1513KARATNoch keine Bewertungen

- Warren SM CH 02 Final PDFDokument66 SeitenWarren SM CH 02 Final PDFSandra0% (1)

- Aman Kapoor - Col. KS Mohan Sir - Priority BankingDokument69 SeitenAman Kapoor - Col. KS Mohan Sir - Priority Bankingbond11111Noch keine Bewertungen

- MKT Assignment (MKT Strategy)Dokument9 SeitenMKT Assignment (MKT Strategy)Fahim RajNoch keine Bewertungen

- BDO Card AppliFormDokument1 SeiteBDO Card AppliFormGilbert BoadillaNoch keine Bewertungen

- CH 5 - Mathematics of FinanceDokument29 SeitenCH 5 - Mathematics of FinanceSherie LynneNoch keine Bewertungen

- Bank Documents (3rd PT FABM2)Dokument18 SeitenBank Documents (3rd PT FABM2)Rose BaynaNoch keine Bewertungen

- Ipsas - Manual de Implementação - snc-APDokument4 SeitenIpsas - Manual de Implementação - snc-APAlcido JuanihaNoch keine Bewertungen

- Microsoft Word - Challan FormDokument1 SeiteMicrosoft Word - Challan Formadil shareen100% (1)

- CustodialDokument3 SeitenCustodialVinit PoojaryNoch keine Bewertungen

- Functions of The State Bank of PakistanDokument13 SeitenFunctions of The State Bank of PakistanHamadBalouchNoch keine Bewertungen

- Comprehensive NotesDokument13 SeitenComprehensive NotesBelle Andrea GozonNoch keine Bewertungen

- Banking Sector Reforms in IndiaDokument43 SeitenBanking Sector Reforms in IndiaChandini KambapuNoch keine Bewertungen

- Banker Customer RelationshipDokument4 SeitenBanker Customer RelationshipSaadat Ullah KhanNoch keine Bewertungen

- Schedule of Charges For Nri Accounts PrimeDokument4 SeitenSchedule of Charges For Nri Accounts PrimeSonam SharmaNoch keine Bewertungen

- Credit Co-Operative SocietiesDokument31 SeitenCredit Co-Operative SocietiesGurpreet Singh Deol100% (1)

- Problem SetDokument1 SeiteProblem SetNoel PadronNoch keine Bewertungen

- Irda Forms - Ia / Ib / IcDokument15 SeitenIrda Forms - Ia / Ib / IcSenthil KumarNoch keine Bewertungen

- 862 Bob Statement PDFDokument29 Seiten862 Bob Statement PDFTILAK PATELNoch keine Bewertungen

- Impact of Interest Rates On Stock Market in IndiaDokument76 SeitenImpact of Interest Rates On Stock Market in Indiakiran100% (1)

- Acca Paper F3 Financial Accounting Mock Exam Prepared By: MR Yeo Hong AnnDokument23 SeitenAcca Paper F3 Financial Accounting Mock Exam Prepared By: MR Yeo Hong AnnOrion0088Noch keine Bewertungen

- Cif IndividualDokument2 SeitenCif IndividualKeyla LumapasNoch keine Bewertungen

- Fact Sheet - DRT SuitDokument4 SeitenFact Sheet - DRT SuitdimpleNoch keine Bewertungen

- July 2009 NavigatorDokument4 SeitenJuly 2009 NavigatorRob FernandesNoch keine Bewertungen

- Islamic Banking AssignmentDokument3 SeitenIslamic Banking AssignmentNadia BaigNoch keine Bewertungen

- TR 7. Garcia v. CADokument2 SeitenTR 7. Garcia v. CAJyrus CimatuNoch keine Bewertungen

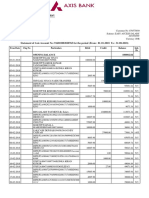

- Statement of Axis Account No:916010083028765 For The Period (From: 01-01-2018 To: 31-08-2018)Dokument9 SeitenStatement of Axis Account No:916010083028765 For The Period (From: 01-01-2018 To: 31-08-2018)Saran ManiNoch keine Bewertungen

- Fee Information DocumentDokument2 SeitenFee Information DocumentGsz Eli WongNoch keine Bewertungen

- Lending ProcessDokument15 SeitenLending ProcessRed HulkNoch keine Bewertungen