Das könnte Ihnen auch gefallen

- CONSTITUTIONAL LIMITATIONS - Those Limitations On The State's Exercise of TheDokument6 SeitenCONSTITUTIONAL LIMITATIONS - Those Limitations On The State's Exercise of TheMaybielynDavidNoch keine Bewertungen

- Cases TAXDokument10 SeitenCases TAXANGIE BERNALNoch keine Bewertungen

- Limitations I Nthe Power To TaxDokument3 SeitenLimitations I Nthe Power To TaxJoshua AmahitNoch keine Bewertungen

- Philex Mining Corporation vs Commissioner of Internal RevenueDokument11 SeitenPhilex Mining Corporation vs Commissioner of Internal RevenueJemar DelcampoNoch keine Bewertungen

- Nature of The Power of Taxation As An Inherent PowerDokument3 SeitenNature of The Power of Taxation As An Inherent PowerAnonymous DbjsDYAS100% (2)

- General PrinciplesDokument15 SeitenGeneral PrinciplesattywithnocaseyetNoch keine Bewertungen

- Taxation Law Class Report Topics and Case DoctrinesDokument134 SeitenTaxation Law Class Report Topics and Case DoctrinesCharm FerrerNoch keine Bewertungen

- Taxation Law 1 - Lectures by Atty. DumalaganDokument25 SeitenTaxation Law 1 - Lectures by Atty. DumalaganAlena Icao-Anotado100% (1)

- Tax CasesDokument63 SeitenTax CasesImelda Arreglo-AgripaNoch keine Bewertungen

- Taxation Case Digest2Dokument242 SeitenTaxation Case Digest2Kevin LavinaNoch keine Bewertungen

- General Principle TaxationDokument2 SeitenGeneral Principle Taxationnodnel salonNoch keine Bewertungen

- Tax DigestDokument217 SeitenTax DigestJarvy Pinongan100% (1)

- Case Digest TaxationDokument8 SeitenCase Digest Taxationtats100% (4)

- Case DigestsDokument158 SeitenCase DigestsJustin Imadhay100% (4)

- Pepsi Cole Bottling Company vs. Municipality of TanauanDokument2 SeitenPepsi Cole Bottling Company vs. Municipality of TanauanBae IreneNoch keine Bewertungen

- Bank Tax CaseDokument8 SeitenBank Tax CaseScribd Government DocsNoch keine Bewertungen

- DoctrinesDokument3 SeitenDoctrinesRoi Vincent RomeroNoch keine Bewertungen

- ABAKADA Guro Party List vs. ErmitaDokument9 SeitenABAKADA Guro Party List vs. ErmitaGabriel LajaraNoch keine Bewertungen

- Nature of The Power To TaxDokument4 SeitenNature of The Power To TaxLuisito Moslares MaestreNoch keine Bewertungen

- 1 Lutz vs. AranetaDokument35 Seiten1 Lutz vs. AranetaColleen Fretzie Laguardia NavarroNoch keine Bewertungen

- Taxes Defined: CIR vs Algue, Inc. and Key Taxation PrinciplesDokument4 SeitenTaxes Defined: CIR vs Algue, Inc. and Key Taxation PrinciplesAndrea IvanneNoch keine Bewertungen

- Held:: of Makati vs. CA, G.R. Nos. 89898-99, October 1, 1990)Dokument5 SeitenHeld:: of Makati vs. CA, G.R. Nos. 89898-99, October 1, 1990)charmagne cuevasNoch keine Bewertungen

- Phil Health Providers vs CIR DST RulingDokument3 SeitenPhil Health Providers vs CIR DST RulingIrene QuimsonNoch keine Bewertungen

- CHAPTER 1 - Fundamental Principles of TaxationDokument7 SeitenCHAPTER 1 - Fundamental Principles of Taxationcurlybambi100% (2)

- Taxation I Cases: Taxation Vis-À-Vis TaxDokument9 SeitenTaxation I Cases: Taxation Vis-À-Vis TaxKitel YbañezNoch keine Bewertungen

- Chap 1 Gen PrinciplesDokument4 SeitenChap 1 Gen PrinciplesJourd Magbanua100% (3)

- Limitations On The Power of TaxationDokument2 SeitenLimitations On The Power of TaxationApril Anne Costales100% (1)

- Purpose and Scope of TaxationDokument6 SeitenPurpose and Scope of TaxationMaria ThereseNoch keine Bewertungen

- Benefits-Protection TheoryDokument2 SeitenBenefits-Protection TheoryBoy Omar Garangan DatudaculaNoch keine Bewertungen

- Notes On TaxationDokument30 SeitenNotes On TaxationBeyond PaperNoch keine Bewertungen

- Taxation Notes: Are Deemed To Be The Laws of The Occupied Territory and Not of The Occupying EnemyDokument18 SeitenTaxation Notes: Are Deemed To Be The Laws of The Occupied Territory and Not of The Occupying EnemyReynaldo YuNoch keine Bewertungen

- Constitutional Limitations of TaxationDokument2 SeitenConstitutional Limitations of TaxationZoilo Renzo AmadorNoch keine Bewertungen

- Illustrations of Lifeblood Theory: "Symbiotic Relation"Dokument2 SeitenIllustrations of Lifeblood Theory: "Symbiotic Relation"joyNoch keine Bewertungen

- Issues On Assesment and Tax Collection Under The Bir and Proposed SolutionsDokument32 SeitenIssues On Assesment and Tax Collection Under The Bir and Proposed SolutionsEnrique Legaspi IVNoch keine Bewertungen

- Tax 1 - TereDokument57 SeitenTax 1 - Terecmv mendoza100% (1)

- 04 Victorias Milling Co. Inc. vs. Municipality of VictoriasDokument2 Seiten04 Victorias Milling Co. Inc. vs. Municipality of VictoriasJamaica Cabildo ManaligodNoch keine Bewertungen

- Limitations The of To To: InequitableDokument1 SeiteLimitations The of To To: InequitableKaren AfricanoNoch keine Bewertungen

- Doctrine (10 Cases)Dokument3 SeitenDoctrine (10 Cases)Coleen Del RosarioNoch keine Bewertungen

- Pepsi-Cola Bottling Co. of The Philippines, Inc. v. Municipality of TanauanDokument13 SeitenPepsi-Cola Bottling Co. of The Philippines, Inc. v. Municipality of TanauanFe Myra LagrosasNoch keine Bewertungen

- Gen. Principles and Income TaxDokument46 SeitenGen. Principles and Income TaxLeidi Kyohei NakaharaNoch keine Bewertungen

- 292 Sison V AnchetaDokument1 Seite292 Sison V AnchetaJuan Samuel IsmaelNoch keine Bewertungen

- Iii. Power of Taxation (DGST) Sison Vs Ancheta GR No. L-59431, 25 July 1984 Facts: Section 1 of BP BLG 135 Amended The TaxDokument6 SeitenIii. Power of Taxation (DGST) Sison Vs Ancheta GR No. L-59431, 25 July 1984 Facts: Section 1 of BP BLG 135 Amended The TaxMadelle PinedaNoch keine Bewertungen

- Case 1 - Manila Memorial Park v. DSWDDokument181 SeitenCase 1 - Manila Memorial Park v. DSWDEleazar CallantaNoch keine Bewertungen

- General Principle NotesDokument11 SeitenGeneral Principle NotesBar2012Noch keine Bewertungen

- PBCOM To TIODokument24 SeitenPBCOM To TIOShall PMNoch keine Bewertungen

- TAXATION: DEFINITION, PURPOSE, BASIS AND EXEMPTIONSDokument4 SeitenTAXATION: DEFINITION, PURPOSE, BASIS AND EXEMPTIONSMichelle Mae MabanoNoch keine Bewertungen

- Philex Mining vs. CIR, 294 SCRA 687Dokument12 SeitenPhilex Mining vs. CIR, 294 SCRA 687KidMonkey2299Noch keine Bewertungen

- National Power Corporation v. City of CabanatuanDokument21 SeitenNational Power Corporation v. City of CabanatuanXyril Ü LlanesNoch keine Bewertungen

- National Power Corp vs City of CabanatuanDokument22 SeitenNational Power Corp vs City of CabanatuanAggy AlbotraNoch keine Bewertungen

- Tax1 General Principles of TaxationDokument81 SeitenTax1 General Principles of TaxationLee Suarez100% (1)

- Classification of TaxesDokument16 SeitenClassification of TaxesJo-Al Gealon100% (1)

- The Economic Policies of Alexander Hamilton: Works & Speeches of the Founder of American Financial SystemVon EverandThe Economic Policies of Alexander Hamilton: Works & Speeches of the Founder of American Financial SystemNoch keine Bewertungen

- Landlord Tax Planning StrategiesVon EverandLandlord Tax Planning StrategiesNoch keine Bewertungen

- Hamilton's Economic Policies: Works & Speeches of the Founder of American Financial SystemVon EverandHamilton's Economic Policies: Works & Speeches of the Founder of American Financial SystemNoch keine Bewertungen

- Learning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxVon EverandLearning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxNoch keine Bewertungen

- How America was Tricked on Tax Policy: Secrets and Undisclosed PracticesVon EverandHow America was Tricked on Tax Policy: Secrets and Undisclosed PracticesNoch keine Bewertungen

- Next Level Tax Course: The only book a newbie needs for a foundation of the tax industryVon EverandNext Level Tax Course: The only book a newbie needs for a foundation of the tax industryNoch keine Bewertungen

- Criminal Law Class Grading SheetDokument2 SeitenCriminal Law Class Grading SheetXirkul TupasNoch keine Bewertungen

- Prelims - 2cDokument1 SeitePrelims - 2cXirkul TupasNoch keine Bewertungen

- Skull Island Attendance - 3-12-22 - 2aDokument2 SeitenSkull Island Attendance - 3-12-22 - 2aXirkul TupasNoch keine Bewertungen

- Crim1811 CoursehandoutsDokument97 SeitenCrim1811 CoursehandoutsXirkul TupasNoch keine Bewertungen

- CS Form No. 212 Attachment - Work Experience SheetDokument2 SeitenCS Form No. 212 Attachment - Work Experience SheetAniaNoch keine Bewertungen

- CS Lead18232020 2021Dokument4 SeitenCS Lead18232020 2021Xirkul TupasNoch keine Bewertungen

- Ccje Class Record Template 2021Dokument16 SeitenCcje Class Record Template 2021Xirkul TupasNoch keine Bewertungen

- Plea BargainingDokument1 SeitePlea BargainingXirkul TupasNoch keine Bewertungen

- CS Form No. 212 Personal Data Sheet RevisedDokument4 SeitenCS Form No. 212 Personal Data Sheet RevisedXirkul TupasNoch keine Bewertungen

- Sti West Negros University Burgos ST., Bacolod City, Negros Occidental, Philippines, 6100Dokument2 SeitenSti West Negros University Burgos ST., Bacolod City, Negros Occidental, Philippines, 6100Xirkul TupasNoch keine Bewertungen

- School Personnel Line Up 2022Dokument14 SeitenSchool Personnel Line Up 2022Xirkul TupasNoch keine Bewertungen

- Criminal Law Class Grading SheetDokument2 SeitenCriminal Law Class Grading SheetXirkul TupasNoch keine Bewertungen

- Colorful Vintage Museum Exhibit Painting Illustration History Class Education PresentationDokument1 SeiteColorful Vintage Museum Exhibit Painting Illustration History Class Education PresentationXirkul TupasNoch keine Bewertungen

- Plea BargainingDokument1 SeitePlea BargainingXirkul TupasNoch keine Bewertungen

- Sti West Negros University Burgos ST., Bacolod City, Negros Occidental, Philippines, 6100Dokument2 SeitenSti West Negros University Burgos ST., Bacolod City, Negros Occidental, Philippines, 6100Xirkul TupasNoch keine Bewertungen

- Final Offer - Homecillo-SignedDokument6 SeitenFinal Offer - Homecillo-SignedXirkul TupasNoch keine Bewertungen

- Final Offer - Homecillo-SignedDokument6 SeitenFinal Offer - Homecillo-SignedXirkul TupasNoch keine Bewertungen

- Request To ReturnDokument1 SeiteRequest To ReturnXirkul TupasNoch keine Bewertungen

- Grading Sheet Shows Scores for Criminal Law ClassDokument2 SeitenGrading Sheet Shows Scores for Criminal Law ClassXirkul TupasNoch keine Bewertungen

- Sti West Negros University Burgos ST., Bacolod City, Negros Occidental, Philippines, 6100Dokument2 SeitenSti West Negros University Burgos ST., Bacolod City, Negros Occidental, Philippines, 6100Xirkul TupasNoch keine Bewertungen

- Generous Gift of The MilitantDokument1 SeiteGenerous Gift of The MilitantXirkul TupasNoch keine Bewertungen

- Generous Gift of The MilitantDokument1 SeiteGenerous Gift of The MilitantXirkul TupasNoch keine Bewertungen

- The World Is An AppleDokument1 SeiteThe World Is An AppleXirkul TupasNoch keine Bewertungen

- Affidavit of Business Ownership KFKLDSNJKNSDKJFNDSJFVDokument1 SeiteAffidavit of Business Ownership KFKLDSNJKNSDKJFNDSJFVXirkul TupasNoch keine Bewertungen

- Generous Gift of The MilitantDokument1 SeiteGenerous Gift of The MilitantXirkul TupasNoch keine Bewertungen

- Great DatDokument1 SeiteGreat DatXirkul TupasNoch keine Bewertungen

- Notarial RegisterDokument1 SeiteNotarial RegisterXirkul TupasNoch keine Bewertungen

- Fiidavit To Slleight: Direct ExaminationDokument4 SeitenFiidavit To Slleight: Direct ExaminationXirkul TupasNoch keine Bewertungen

- Return motorcycle request letterDokument2 SeitenReturn motorcycle request letterXirkul TupasNoch keine Bewertungen

- Fiidavit To Slleight: Direct ExaminationDokument4 SeitenFiidavit To Slleight: Direct ExaminationXirkul TupasNoch keine Bewertungen

- IT-PLANET Cash Memo DetailsDokument1 SeiteIT-PLANET Cash Memo DetailsNikk AdesaraNoch keine Bewertungen

- East Delta University Payment InvoiceDokument2 SeitenEast Delta University Payment InvoiceMiraj RisatNoch keine Bewertungen

- GSTR3B PDFDokument48 SeitenGSTR3B PDFmalhar develkarNoch keine Bewertungen

- US Internal Revenue Service: td8734Dokument314 SeitenUS Internal Revenue Service: td8734IRSNoch keine Bewertungen

- June 20, 2021 July 8, 2021: Credit Card StatementDokument3 SeitenJune 20, 2021 July 8, 2021: Credit Card StatementPrateik ParakhNoch keine Bewertungen

- Cap & Gown OrderDokument2 SeitenCap & Gown OrderΝίκος Μυρογιάννης-ΚούκοςNoch keine Bewertungen

- What Is TRAIN Law and Its PurposeDokument6 SeitenWhat Is TRAIN Law and Its PurposeNica BastiNoch keine Bewertungen

- Samsung Refrigerator Tax InvoiceDokument1 SeiteSamsung Refrigerator Tax InvoiceJyoti Sarkar0% (1)

- Mepco Online Bill Hassan Raza DharallaDokument2 SeitenMepco Online Bill Hassan Raza DharallaTahfuz EhsaasNoch keine Bewertungen

- Credit Card StatementDokument4 SeitenCredit Card StatementbpraveensinghNoch keine Bewertungen

- E-Loading Guide: 1 Sim Load All NetworksDokument3 SeitenE-Loading Guide: 1 Sim Load All NetworksJoshua MaravillaNoch keine Bewertungen

- 3141XXXXXXXXX131419 07 2019Dokument2 Seiten3141XXXXXXXXX131419 07 2019Rahul JangraNoch keine Bewertungen

- Allied Bank Different AccountsDokument8 SeitenAllied Bank Different AccountsShahzaib KhanNoch keine Bewertungen

- Degital Payment SystemDokument20 SeitenDegital Payment SystemJaivik PanchalNoch keine Bewertungen

- Becker CPA Review Summary of Changes Included in The V1.1 REG TextbookDokument16 SeitenBecker CPA Review Summary of Changes Included in The V1.1 REG Textbookmohit2ucNoch keine Bewertungen

- LT Bill 19000113351 201909 PDFDokument2 SeitenLT Bill 19000113351 201909 PDFDipayan100% (1)

- Foreign Exchange Management ActDokument36 SeitenForeign Exchange Management ActSri VarshiniNoch keine Bewertungen

- Creditors Reconciliation Question Suggested SolutionDokument2 SeitenCreditors Reconciliation Question Suggested SolutionShweta SinghNoch keine Bewertungen

- DISH Final AwardDokument53 SeitenDISH Final Awarddsmithy65Noch keine Bewertungen

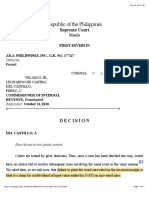

- Republic of The Philippines: Supreme CourtDokument11 SeitenRepublic of The Philippines: Supreme Courtyannie11Noch keine Bewertungen

- Water BillDokument2 SeitenWater BillSharungomes0% (1)

- Value Added Taxes Part 1 ExplainedDokument75 SeitenValue Added Taxes Part 1 ExplainedLEILALYN NICOLAS100% (1)

- June-Pay Slip PDFDokument1 SeiteJune-Pay Slip PDFAnonymous 5JMuQyENoch keine Bewertungen

- Ice Task 2 Delta LTD QuestionDokument5 SeitenIce Task 2 Delta LTD QuestionarronyeagarNoch keine Bewertungen

- Guide to Income Tax Proofs for Investments and DeductionsDokument2 SeitenGuide to Income Tax Proofs for Investments and Deductionssamuraioo7Noch keine Bewertungen

- .Paper - V - Sec.I - Direct Taxes PDFDokument238 Seiten.Paper - V - Sec.I - Direct Taxes PDFMichelle MarkNoch keine Bewertungen

- Preparation of BillsDokument46 SeitenPreparation of BillsBhanu GudluruNoch keine Bewertungen

- Multiple Choice-Problems MCIT of A Manufacturing ConcernDokument17 SeitenMultiple Choice-Problems MCIT of A Manufacturing ConcernAngela Ruedas75% (4)

- 2018 - PAL vs. CIRDokument2 Seiten2018 - PAL vs. CIRJimcris HermosadoNoch keine Bewertungen

- Kalahari Resorts Ohio - Reservations - Search Reservation ResultsDokument4 SeitenKalahari Resorts Ohio - Reservations - Search Reservation ResultsraviNoch keine Bewertungen