Das könnte Ihnen auch gefallen

- Adresseavisen Group: ND NDDokument6 SeitenAdresseavisen Group: ND NDaptureincNoch keine Bewertungen

- Sanitärtechnik Eisenberg GMBH - FinancialsDokument2 SeitenSanitärtechnik Eisenberg GMBH - Financialsin_daHouseNoch keine Bewertungen

- ANJ Annual Report Highlights Sustainable GrowthDokument216 SeitenANJ Annual Report Highlights Sustainable GrowthAry PandeNoch keine Bewertungen

- Excel Bodyshop EFDokument18 SeitenExcel Bodyshop EFgestion integralNoch keine Bewertungen

- Monmouth Inc Figures in Million $Dokument3 SeitenMonmouth Inc Figures in Million $amanNoch keine Bewertungen

- Marel q3 2019 Condensed Consolidated Interim Financial Statements ExcelDokument5 SeitenMarel q3 2019 Condensed Consolidated Interim Financial Statements ExcelAndre Laine AndreNoch keine Bewertungen

- 9M 2023 Reviewed Financial StatementsDokument64 Seiten9M 2023 Reviewed Financial StatementsZain RehmanNoch keine Bewertungen

- 915 529 Supplement Landmark XLS ENGDokument32 Seiten915 529 Supplement Landmark XLS ENGPaco ColínNoch keine Bewertungen

- Reliance Chemotex P and LDokument2 SeitenReliance Chemotex P and LRushil GabaNoch keine Bewertungen

- Case ExhibitsDokument7 SeitenCase Exhibitsug8Noch keine Bewertungen

- Landmark CaseDokument22 SeitenLandmark CaseLauren KlaassenNoch keine Bewertungen

- Ey Aarsrapport 2021 22 25Dokument1 SeiteEy Aarsrapport 2021 22 25Ronald RunruilNoch keine Bewertungen

- WackerDokument200 SeitenWackerpetar2001Noch keine Bewertungen

- Sealed Air Corporations Leveraged Recapitalization (A), Spreadsheet SupplementDokument6 SeitenSealed Air Corporations Leveraged Recapitalization (A), Spreadsheet SupplementKaran VoraNoch keine Bewertungen

- Canada Packers - Exhibits + Valuation - FionaDokument63 SeitenCanada Packers - Exhibits + Valuation - Fiona/jncjdncjdn100% (1)

- Nordstrom 2010 Annual ReportDokument88 SeitenNordstrom 2010 Annual ReportThiago Ribeiro da SilvaNoch keine Bewertungen

- Financial Statements-Kingsley AkinolaDokument4 SeitenFinancial Statements-Kingsley AkinolaKingsley AkinolaNoch keine Bewertungen

- Internship Report on Ratio Analysis of Jamuna BankDokument5 SeitenInternship Report on Ratio Analysis of Jamuna BanksahhhhhhhNoch keine Bewertungen

- Valuation Analysis For Robertson ToolDokument5 SeitenValuation Analysis For Robertson ToolPedro José ZapataNoch keine Bewertungen

- 3 Companies CS - Calculations 2022Dokument27 Seiten3 Companies CS - Calculations 2022shubhangi.jain582Noch keine Bewertungen

- Tata Steel LTD.: Margins On Income On Total IncomeDokument4 SeitenTata Steel LTD.: Margins On Income On Total IncomepriyaNoch keine Bewertungen

- Monmouth Inc SolutionDokument9 SeitenMonmouth Inc SolutionAjaxNoch keine Bewertungen

- Monmouth Inc SolutionDokument9 SeitenMonmouth Inc SolutionGourav DadhichNoch keine Bewertungen

- Paccar Ar 2015Dokument98 SeitenPaccar Ar 2015Quang PhanNoch keine Bewertungen

- Vantage Towers Q3 2020 Financial ReportDokument40 SeitenVantage Towers Q3 2020 Financial ReportValtteri ItärantaNoch keine Bewertungen

- Bright Line Sol.Dokument3 SeitenBright Line Sol.Sudesh SharmaNoch keine Bewertungen

- ANJ AR 2014 English - dT8RRA20170321164537Dokument232 SeitenANJ AR 2014 English - dT8RRA20170321164537baktikaryaditoNoch keine Bewertungen

- Prova Múltiplos Ciclo 2023.1Dokument14 SeitenProva Múltiplos Ciclo 2023.1Jadi MouradNoch keine Bewertungen

- Anexo 2: Selected Linear Financial Data in Millions of Dollars (Except Share Data), 1992-2003Dokument7 SeitenAnexo 2: Selected Linear Financial Data in Millions of Dollars (Except Share Data), 1992-2003Milton Raul Rivas saballosNoch keine Bewertungen

- 120 Financial Statements and Ratio Analysis PDFDokument20 Seiten120 Financial Statements and Ratio Analysis PDFMohit WaniNoch keine Bewertungen

- 4211 XLS EngDokument22 Seiten4211 XLS Engvictor vasquezNoch keine Bewertungen

- Financial Statements 78-119Dokument42 SeitenFinancial Statements 78-119Marcela PopaNoch keine Bewertungen

- BCTC Case 2Dokument10 SeitenBCTC Case 2Trâm Nguyễn QuỳnhNoch keine Bewertungen

- Presentation 1Dokument9 SeitenPresentation 1Zubair KhanNoch keine Bewertungen

- Q3 2022 Quarterly Financial Statements VT Group AGDokument6 SeitenQ3 2022 Quarterly Financial Statements VT Group AGAmr YehiaNoch keine Bewertungen

- MandS FinancialTablesandNotesDokument41 SeitenMandS FinancialTablesandNotessai101Noch keine Bewertungen

- 2022 Financial ReportDokument116 Seiten2022 Financial ReportTran Thi ThuongNoch keine Bewertungen

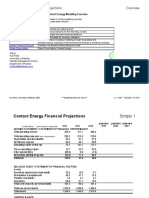

- Contact - Main 2006Dokument89 SeitenContact - Main 2006api-3763138Noch keine Bewertungen

- NH Financial Group Annual Report 2017Dokument121 SeitenNH Financial Group Annual Report 2017b6Noch keine Bewertungen

- RIAS Annual Financiel Account Statement 2019/20 1Dokument30 SeitenRIAS Annual Financiel Account Statement 2019/20 1Leandro Mainumby Arapoty BorgesNoch keine Bewertungen

- Orascom Construction PLC Interim Financial StatementsDokument62 SeitenOrascom Construction PLC Interim Financial StatementsEiad WaleedNoch keine Bewertungen

- Nestle Income Statement & Balance SheetDokument10 SeitenNestle Income Statement & Balance SheetDristi SinghNoch keine Bewertungen

- Trent LTDDokument23 SeitenTrent LTDpulkitnarang1606Noch keine Bewertungen

- FINM7044 Assignment 1 Group Company ModelDokument42 SeitenFINM7044 Assignment 1 Group Company ModelMesh MohNoch keine Bewertungen

- WSP GL FS Q22023 enDokument24 SeitenWSP GL FS Q22023 endennis72288Noch keine Bewertungen

- Rieter Consolidated Balance Sheet 2020 enDokument1 SeiteRieter Consolidated Balance Sheet 2020 enMuhammadSiddiqNoch keine Bewertungen

- This Spreadsheet Supports STUDENT Analysis of The Case "Bob's Baloney" (UVA-F-1942)Dokument4 SeitenThis Spreadsheet Supports STUDENT Analysis of The Case "Bob's Baloney" (UVA-F-1942)LAWZ1017Noch keine Bewertungen

- Bajaj Finserv Limited's focus on lending, asset management, and insuranceDokument23 SeitenBajaj Finserv Limited's focus on lending, asset management, and insuranceAthira K. ANoch keine Bewertungen

- A E L (AEL) : Mber Nterprises TDDokument8 SeitenA E L (AEL) : Mber Nterprises TDdarshanmadeNoch keine Bewertungen

- Consolidated Income and Financial Statements 2018Dokument4 SeitenConsolidated Income and Financial Statements 2018Aayush PrakashNoch keine Bewertungen

- DL 090227 2008 PDFDokument216 SeitenDL 090227 2008 PDFcattleyajenNoch keine Bewertungen

- Monmouth Inc SolutionDokument9 SeitenMonmouth Inc SolutionCesar CameyNoch keine Bewertungen

- Monmouth Inc SolutionDokument9 SeitenMonmouth Inc SolutionPedro José ZapataNoch keine Bewertungen

- Monmouth Inc SolutionDokument9 SeitenMonmouth Inc SolutionPedro José ZapataNoch keine Bewertungen

- Horniman Horticulture Financial ProjectionsDokument2 SeitenHorniman Horticulture Financial ProjectionsHằng Dương Thị MinhNoch keine Bewertungen

- Book 2Dokument18 SeitenBook 2Aishwarya DaymaNoch keine Bewertungen

- 2 B&K 3qfy20Dokument7 Seiten2 B&K 3qfy20Girish Raj SankunnyNoch keine Bewertungen

- Ey Aarsrapport 2021 22 15Dokument1 SeiteEy Aarsrapport 2021 22 15Ronald RunruilNoch keine Bewertungen

- Engineering and Commercial Functions in BusinessVon EverandEngineering and Commercial Functions in BusinessBewertung: 5 von 5 Sternen5/5 (1)

- Delivering Utility Computing: Business-driven IT OptimizationVon EverandDelivering Utility Computing: Business-driven IT OptimizationNoch keine Bewertungen

- CDSC FAQ EnglishDokument44 SeitenCDSC FAQ EnglishSanjeev Bikram KarkiNoch keine Bewertungen

- Commodities Corp The Mike Marcus TapeDokument10 SeitenCommodities Corp The Mike Marcus TapeLonewolf99100% (2)

- Environmental Services Inc Performs Various Tests On Wells and SepticDokument1 SeiteEnvironmental Services Inc Performs Various Tests On Wells and Septictrilocksp SinghNoch keine Bewertungen

- Supply and Demand Basic Forex Stocks Trading Nutshell by Alfonso MorenoDokument48 SeitenSupply and Demand Basic Forex Stocks Trading Nutshell by Alfonso MorenoNguyen Ung100% (2)

- PPL Cup DifficultDokument8 SeitenPPL Cup DifficultRukia Kuchiki100% (1)

- Problem 1: The Statement of Affairs: Straight ProblemsDokument5 SeitenProblem 1: The Statement of Affairs: Straight ProblemsJemNoch keine Bewertungen

- Analyzing Reverse Merger in India Ease in Tax Implication PDFDokument13 SeitenAnalyzing Reverse Merger in India Ease in Tax Implication PDFDhruv TiwariNoch keine Bewertungen

- American and Euro Option DifferenceDokument4 SeitenAmerican and Euro Option DifferenceShabana KhanNoch keine Bewertungen

- CFA 2 - Mock Exam AIDokument5 SeitenCFA 2 - Mock Exam AITiến Dũng MaiNoch keine Bewertungen

- FinQuiz Level2Mock2016Version3JuneAMQuestionsDokument33 SeitenFinQuiz Level2Mock2016Version3JuneAMQuestionsDavid LêNoch keine Bewertungen

- Antique'S Morning Presentation: Global NewsDokument11 SeitenAntique'S Morning Presentation: Global NewsRomelu MartialNoch keine Bewertungen

- Arbitrage Pricing TheoryDokument20 SeitenArbitrage Pricing TheoryDeepti PantulaNoch keine Bewertungen

- CMBS 101 Slides (All Sessions) CMSADokument41 SeitenCMBS 101 Slides (All Sessions) CMSAaehayaNoch keine Bewertungen

- JAWABAN ADVANCE 2 Intercompany TransactionsDokument6 SeitenJAWABAN ADVANCE 2 Intercompany TransactionsDANIEL TEJANoch keine Bewertungen

- Goldman Sachs Abacus 2007 Ac1 An Outline of The Financial CrisisDokument14 SeitenGoldman Sachs Abacus 2007 Ac1 An Outline of The Financial CrisisAkanksha BehlNoch keine Bewertungen

- Comm 457 Solutions To Practice MidtermDokument9 SeitenComm 457 Solutions To Practice MidtermJason SNoch keine Bewertungen

- Afin250 2018S1Dokument19 SeitenAfin250 2018S1jimmyNoch keine Bewertungen

- Baf Annual Report 2022Dokument558 SeitenBaf Annual Report 2022Tahir Mustafa ChohanNoch keine Bewertungen

- DCF Model Example - PRGODokument57 SeitenDCF Model Example - PRGOstayfoolishmediaNoch keine Bewertungen

- Chapter 7 LeverageDokument21 SeitenChapter 7 Leveragemuluken walelgnNoch keine Bewertungen

- Wasting Assets Impairment of AssetsDokument14 SeitenWasting Assets Impairment of AssetsJohn Ferd M. FerminNoch keine Bewertungen

- The Amazing Secrets of The Hottest Forex Trader PDFDokument17 SeitenThe Amazing Secrets of The Hottest Forex Trader PDFcreat150% (2)

- Corporate Finance - KS KimDokument5 SeitenCorporate Finance - KS Kim01202750693Noch keine Bewertungen

- Ch13 InvestmentsDokument29 SeitenCh13 InvestmentsJemal SeidNoch keine Bewertungen

- Secrets of A Forex Millionaire TraderDokument61 SeitenSecrets of A Forex Millionaire TraderEric PlottPalmTrees.Com75% (12)

- Boot Camp Part 2: Volatility, Directional Trading, and SpreadingDokument48 SeitenBoot Camp Part 2: Volatility, Directional Trading, and SpreadingVineet Vidyavilas PathakNoch keine Bewertungen

- 1033. ტურიზმის-მარკეტინგი-სოფო-თევდორაძეDokument120 Seiten1033. ტურიზმის-მარკეტინგი-სოფო-თევდორაძეAnton SinatashviliNoch keine Bewertungen

- Enabling ActivityDokument5 SeitenEnabling ActivityQuienilyn SanchezNoch keine Bewertungen

- Essay On Market EfficiencyDokument2 SeitenEssay On Market EfficiencyKimkhorn LongNoch keine Bewertungen

- Course outline-ISF 201 Islamic Financial AccountingDokument2 SeitenCourse outline-ISF 201 Islamic Financial AccountingMuhammad Omer RafiqueNoch keine Bewertungen