Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Blaine Kitchenware Case Study SolutionDokument5 SeitenBlaine Kitchenware Case Study SolutionMohan Kumar89% (37)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Understanding Technical Stock Market IndicatorsDokument49 SeitenUnderstanding Technical Stock Market IndicatorsTaimoor ShahNoch keine Bewertungen

- NISM-Series-VIII-Equity Derivatives Workbook (New Version September-2015)Dokument162 SeitenNISM-Series-VIII-Equity Derivatives Workbook (New Version September-2015)janardhanvn100% (3)

- Psychology PG PDFDokument45 SeitenPsychology PG PDFkumarrajdeepbsrNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Acct 2101 Exam 1 Study GuideDokument3 SeitenAcct 2101 Exam 1 Study GuideDavid Lee100% (1)

- Fusion Applications: 14 July 2010Dokument50 SeitenFusion Applications: 14 July 2010kumarrajdeepbsrNoch keine Bewertungen

- Setting Gann and Murrey MathDokument9 SeitenSetting Gann and Murrey MathAnggi Koloa50% (2)

- SAP GL ConfigurationDokument164 SeitenSAP GL ConfigurationTharaka Hettiarachchi100% (1)

- R.A. No. 11976 - Ease of Paying TaxesDokument18 SeitenR.A. No. 11976 - Ease of Paying TaxesBeaNoch keine Bewertungen

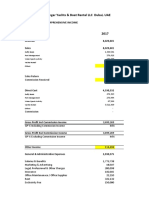

- Sample Balance Sheet Concierge Service IndustryDokument12 SeitenSample Balance Sheet Concierge Service IndustrykpsrikanthvNoch keine Bewertungen

- AP 5904Q InvestmentsDokument4 SeitenAP 5904Q Investmentskristine319Noch keine Bewertungen

- Types of Procurement: Direct, Indirect, Goods & ServicesDokument9 SeitenTypes of Procurement: Direct, Indirect, Goods & ServicesAnas SiddiquiNoch keine Bewertungen

- I-Direct Top Picks: Market Outlook: Key Triggers Ahead Market Outlook: Key Triggers AheadDokument14 SeitenI-Direct Top Picks: Market Outlook: Key Triggers Ahead Market Outlook: Key Triggers AheadkumarrajdeepbsrNoch keine Bewertungen

- Greentree4 Product Overview Full Brochure PDFDokument56 SeitenGreentree4 Product Overview Full Brochure PDFkumarrajdeepbsrNoch keine Bewertungen

- I-Direct Top Picks: Market Outlook: Key Triggers Ahead Market Outlook: Key Triggers AheadDokument14 SeitenI-Direct Top Picks: Market Outlook: Key Triggers Ahead Market Outlook: Key Triggers AheadkumarrajdeepbsrNoch keine Bewertungen

- O F E-B A: " Racle Inancials Usiness Pplications"Dokument4 SeitenO F E-B A: " Racle Inancials Usiness Pplications"kumarrajdeepbsrNoch keine Bewertungen

- NISM Series VIII Equity Derivatives Workbook Version April 2014 Updated On 03 June 2014Dokument162 SeitenNISM Series VIII Equity Derivatives Workbook Version April 2014 Updated On 03 June 2014JomonJoseNoch keine Bewertungen

- Oracle Financials Erp Training System Navigation PDFDokument9 SeitenOracle Financials Erp Training System Navigation PDFkumarrajdeepbsrNoch keine Bewertungen

- Sap Siemens Material Fico PDFDokument1 SeiteSap Siemens Material Fico PDFkumarrajdeepbsr50% (2)

- ErpDokument18 SeitenErpmadhub_17Noch keine Bewertungen

- Step by Step Sap GL User ManualDokument110 SeitenStep by Step Sap GL User Manualsailu000Noch keine Bewertungen

- IndiaDokument114 SeitenIndiastutivadalia100% (1)

- Sample Financial PlanDokument41 SeitenSample Financial Planganasugu100% (1)

- Customer Portal Demo - PpsDokument99 SeitenCustomer Portal Demo - PpskumarrajdeepbsrNoch keine Bewertungen

- Peoplesoft Financials 8.8 vs. 9.0 Delta TrainingDokument154 SeitenPeoplesoft Financials 8.8 vs. 9.0 Delta TrainingkumarrajdeepbsrNoch keine Bewertungen

- Accountspayableinstructorguide1 131028165220 Phpapp02Dokument747 SeitenAccountspayableinstructorguide1 131028165220 Phpapp02Nagendra BabuNoch keine Bewertungen

- Complete Oracle P2P Cycle - Simplifying Oracle E Business SuiteDokument15 SeitenComplete Oracle P2P Cycle - Simplifying Oracle E Business Suitemandeep_kumar7721Noch keine Bewertungen

- Oracle FAH Consolidates Financial DataDokument1 SeiteOracle FAH Consolidates Financial DataRammohan PushadapuNoch keine Bewertungen

- Vision2050 PDFDokument38 SeitenVision2050 PDFkumarrajdeepbsrNoch keine Bewertungen

- Oracle Financials 11 5 10Dokument101 SeitenOracle Financials 11 5 10Avinash100% (10)

- Empoweringoraclespeoplesoftcustomerswiththefinancialintelligenceneededtosucceed 111012132345 Phpapp01Dokument49 SeitenEmpoweringoraclespeoplesoftcustomerswiththefinancialintelligenceneededtosucceed 111012132345 Phpapp01kumarrajdeepbsrNoch keine Bewertungen

- Oracle Applications - Concepts R12Dokument204 SeitenOracle Applications - Concepts R12Ramesh GarikapatiNoch keine Bewertungen

- InsightDokument2 SeitenInsightkumarrajdeepbsrNoch keine Bewertungen

- 11 145 Ajard 609 620 PDFDokument13 Seiten11 145 Ajard 609 620 PDFkumarrajdeepbsrNoch keine Bewertungen

- Narayan's SAEA Goat Marketing Paper 2014 PDFDokument18 SeitenNarayan's SAEA Goat Marketing Paper 2014 PDFkumarrajdeepbsrNoch keine Bewertungen

- Topics Covered: How Corporations Issue SecuritiesDokument7 SeitenTopics Covered: How Corporations Issue SecuritiesTam DoNoch keine Bewertungen

- Second Paper: Elements of Financial ManagementDokument5 SeitenSecond Paper: Elements of Financial ManagementGuruKPONoch keine Bewertungen

- Final Preboard Batch 91 Reviewees PDFDokument18 SeitenFinal Preboard Batch 91 Reviewees PDFJoris YapNoch keine Bewertungen

- Principal Audit Procedures To Be Performed in ConsolidationDokument1 SeitePrincipal Audit Procedures To Be Performed in ConsolidationREtyNoch keine Bewertungen

- Question 1: Ifrs 9 - Financial InstrumentsDokument2 SeitenQuestion 1: Ifrs 9 - Financial InstrumentsamitsinghslideshareNoch keine Bewertungen

- Screenshot 2023-10-02 at 3.41.33 PMDokument3 SeitenScreenshot 2023-10-02 at 3.41.33 PMNareen RajNoch keine Bewertungen

- Organisation Announcement - Rakesh SonyDokument1 SeiteOrganisation Announcement - Rakesh SonyAshwaniNoch keine Bewertungen

- Ibig 04 08Dokument45 SeitenIbig 04 08Russell KimNoch keine Bewertungen

- Dep Mini Case Mohini Sharma Bengal Aluminium and Other ProblemsDokument3 SeitenDep Mini Case Mohini Sharma Bengal Aluminium and Other ProblemsAnishaSapraNoch keine Bewertungen

- Free Cash Flow Calculation and Valuation ExampleDokument11 SeitenFree Cash Flow Calculation and Valuation ExamplealliahnahNoch keine Bewertungen

- Consolidation TheoryDokument22 SeitenConsolidation TheorySmruti RanjanNoch keine Bewertungen

- A Study On Multi-Variate Financial Statement Analysis of Amazon and EbayDokument14 SeitenA Study On Multi-Variate Financial Statement Analysis of Amazon and EbayNisrine HafidNoch keine Bewertungen

- First Yacht Project - V1 - ActualsDokument26 SeitenFirst Yacht Project - V1 - ActualsRaja HindustaniNoch keine Bewertungen

- Chapter 3 The Accounting Information SystemDokument62 SeitenChapter 3 The Accounting Information SystemAnshumanSinghNoch keine Bewertungen

- CMA Blank FormDokument34 SeitenCMA Blank FormbipinNoch keine Bewertungen

- Analyzing the Accuracy of the Springate, Zmijewski, and Altman Models in Predicting Financial Distress of Manufacturing Companies Listed on the Indonesia Stock ExchangeDokument13 SeitenAnalyzing the Accuracy of the Springate, Zmijewski, and Altman Models in Predicting Financial Distress of Manufacturing Companies Listed on the Indonesia Stock ExchangehanifNoch keine Bewertungen

- Stock Isin Code Client NameDokument28 SeitenStock Isin Code Client NameSabyasachi BaralNoch keine Bewertungen

- Business CombinationDokument9 SeitenBusiness CombinationRoldan Arca PagaposNoch keine Bewertungen

- Bahria University: Lahore CampusDokument4 SeitenBahria University: Lahore CampusAMBREENNoch keine Bewertungen

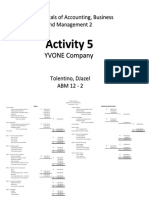

- Activity 5 - TolentinoDokument2 SeitenActivity 5 - TolentinoDJazel TolentinoNoch keine Bewertungen

- Daythree Digital Berhad IPODokument9 SeitenDaythree Digital Berhad IPO健德Noch keine Bewertungen

- Financial Highlights and ReviewsDokument17 SeitenFinancial Highlights and ReviewsThorapioMayNoch keine Bewertungen

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDokument18 SeitenIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeAnonymous taCBG1AKaNoch keine Bewertungen

- Nike Case AnalysisDokument10 SeitenNike Case AnalysisFarhan SoepraptoNoch keine Bewertungen