Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- American Barrick Resources Corporation Managing Gold Price RiskDokument7 SeitenAmerican Barrick Resources Corporation Managing Gold Price RiskKshitishNoch keine Bewertungen

- Market Indices For Stocks and BondsDokument15 SeitenMarket Indices For Stocks and BondsKayshiel Agus100% (1)

- Caf 1 Ia ST PDFDokument270 SeitenCaf 1 Ia ST PDFFizzazubair rana50% (2)

- Cashflow 101 ManualDokument16 SeitenCashflow 101 Manualwladwolf100% (2)

- Banking Law Project. Pankaj Sharma. Sem IX. A.100. HNLUDokument19 SeitenBanking Law Project. Pankaj Sharma. Sem IX. A.100. HNLUPankaj SharmaNoch keine Bewertungen

- Factor-Factor Relationships: X X / X X (X XDokument50 SeitenFactor-Factor Relationships: X X / X X (X XAnandKuttiyanNoch keine Bewertungen

- M3 - Valuation Question SetDokument13 SeitenM3 - Valuation Question SetHetviNoch keine Bewertungen

- Ravenswood 2012 Business Studies Trials & SolutionsDokument37 SeitenRavenswood 2012 Business Studies Trials & SolutionsArpit KumarNoch keine Bewertungen

- Vimp Interview QuestionsDokument19 SeitenVimp Interview Questionsppt85Noch keine Bewertungen

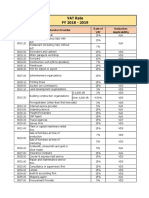

- Bangladesh Tax & VAT Rate 2018-19Dokument6 SeitenBangladesh Tax & VAT Rate 2018-19IFTEKHAR IFTE83% (24)

- Investment+Planning+Module (1)Dokument137 SeitenInvestment+Planning+Module (1)jayaram_polaris100% (1)

- Vanguard Funds: Supplement To The ProspectusesDokument45 SeitenVanguard Funds: Supplement To The Prospectusesnotmee123Noch keine Bewertungen

- Types of StocksDokument16 SeitenTypes of StocksEira ShaneNoch keine Bewertungen

- Insigne v. Abra Valley CollegeDokument2 SeitenInsigne v. Abra Valley CollegeRidzanna AbdulgafurNoch keine Bewertungen

- Assignment 1: Submitted byDokument9 SeitenAssignment 1: Submitted byzarin tasnimNoch keine Bewertungen

- Capital Budgeting, Cash Flows & Decision Making ProcessDokument47 SeitenCapital Budgeting, Cash Flows & Decision Making ProcessAnifahchannie PacalnaNoch keine Bewertungen

- Success MeasuresDokument4 SeitenSuccess MeasuresRachel YoungNoch keine Bewertungen

- MD Abdullah Al Mamun - ID-17102049 - Major Accounting.Dokument44 SeitenMD Abdullah Al Mamun - ID-17102049 - Major Accounting.Abdullah Al MamunNoch keine Bewertungen

- Analysis of Cost EstimationDokument58 SeitenAnalysis of Cost Estimationccsreddy100% (3)

- V1 Exam 2 AMDokument31 SeitenV1 Exam 2 AMNeerajNoch keine Bewertungen

- Lesson 4 Laws On Partnership and CorporationDokument34 SeitenLesson 4 Laws On Partnership and CorporationGerstene Reynoso MaurNoch keine Bewertungen

- 232 FM AssignmentDokument17 Seiten232 FM Assignmentbhupesh joshiNoch keine Bewertungen

- 204 - Corporate and Allied LawsDokument5 Seiten204 - Corporate and Allied LawsSubodh MalkarNoch keine Bewertungen

- Sheet (3) : Corporations: Dividends, Retained Earnings, and Income ReportingDokument28 SeitenSheet (3) : Corporations: Dividends, Retained Earnings, and Income ReportingMagdy KamelNoch keine Bewertungen

- Nse Options Strategies Explanation With ExamplesDokument63 SeitenNse Options Strategies Explanation With Exampleskumarmba09Noch keine Bewertungen

- Corporate FinanceDokument66 SeitenCorporate FinanceRobin SrivastavaNoch keine Bewertungen

- Stock Market Tips For BeginersDokument6 SeitenStock Market Tips For BeginersNarendraVukkaNoch keine Bewertungen

- 012 CASCO PHILIPPINE CHEMICAL CO. v. PEDRO GIMENEZ, GR No. L-17931, 1963-02-28Dokument10 Seiten012 CASCO PHILIPPINE CHEMICAL CO. v. PEDRO GIMENEZ, GR No. L-17931, 1963-02-28Arvin Jay LealNoch keine Bewertungen

- Algorithmic Trading Directory 2010Dokument100 SeitenAlgorithmic Trading Directory 201017524100% (4)

- Definition of 'Financial Analysis'Dokument2 SeitenDefinition of 'Financial Analysis'KumarNoch keine Bewertungen