Das könnte Ihnen auch gefallen

- The Deterministic Life Contingencies ModelDokument6 SeitenThe Deterministic Life Contingencies ModelYhoshy ZeballosNoch keine Bewertungen

- Risk and InsuranceDokument16 SeitenRisk and InsurancehafeezhasnainNoch keine Bewertungen

- Bernard Paper 2012Dokument26 SeitenBernard Paper 2012JuanCamiloGonzálezTrujilloNoch keine Bewertungen

- Seasons 100 ProposalDokument3 SeitenSeasons 100 ProposalAlvin Dela Cruz100% (1)

- BMS REPORT 2_mergedDokument79 SeitenBMS REPORT 2_mergedVaibhav MohiteNoch keine Bewertungen

- 19.3 FMP 2Dokument38 Seiten19.3 FMP 2Javneet KaurNoch keine Bewertungen

- Definition of InsuranceDokument17 SeitenDefinition of InsuranceLNoch keine Bewertungen

- How Much Is That Guarantee in The WindowDokument4 SeitenHow Much Is That Guarantee in The WindowRuss ThorntonNoch keine Bewertungen

- Institute and Faculty of Actuaries: Instructions To The CandidateDokument5 SeitenInstitute and Faculty of Actuaries: Instructions To The Candidateanon_103901460Noch keine Bewertungen

- The Demand and Supply of Health InsuranceDokument6 SeitenThe Demand and Supply of Health Insuranceannie:XNoch keine Bewertungen

- Week 1-3 - Risk ModelsDokument61 SeitenWeek 1-3 - Risk ModelsParita PanchalNoch keine Bewertungen

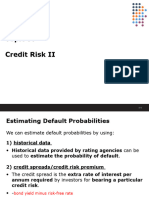

- Topic 9 Credit Risk II - LectureDokument31 SeitenTopic 9 Credit Risk II - Lecturecanenny limNoch keine Bewertungen

- Cost Per YearDokument2 SeitenCost Per YearselvyNoch keine Bewertungen

- ILY Research Paper 091504Dokument30 SeitenILY Research Paper 091504Tu WeiNoch keine Bewertungen

- Risk Management & InsuranceDokument1 SeiteRisk Management & InsuranceSoumitro ChakravartyNoch keine Bewertungen

- Risk and Insurance - Anderson, BrownDokument16 SeitenRisk and Insurance - Anderson, BrownGrant MailerNoch keine Bewertungen

- CH 3Dokument11 SeitenCH 3fikruNoch keine Bewertungen

- Chapter 2 Overview Financial Risk MGMT Questions and Answers-RevisedDokument3 SeitenChapter 2 Overview Financial Risk MGMT Questions and Answers-RevisedSahaana VijayNoch keine Bewertungen

- TermDokument113 SeitenTermvivataNoch keine Bewertungen

- Debunking Common Pitfalls of Life Insurance RiskDokument12 SeitenDebunking Common Pitfalls of Life Insurance RiskfherremansNoch keine Bewertungen

- Insurance and RiskDokument7 SeitenInsurance and RiskZillay HusnainNoch keine Bewertungen

- Risk Management Assignment 3: President University Cikarang UtaraDokument7 SeitenRisk Management Assignment 3: President University Cikarang UtaraAlya RamadhaniNoch keine Bewertungen

- Insurance Industry in IndiaDokument91 SeitenInsurance Industry in IndiaOne's JourneyNoch keine Bewertungen

- The Relevance of Mathematics in Insurance Industry PDFDokument65 SeitenThe Relevance of Mathematics in Insurance Industry PDFMeriNoch keine Bewertungen

- Teaching Notes 2021aDokument44 SeitenTeaching Notes 2021aMohamed Yada AlghaliNoch keine Bewertungen

- Risk Management Chapter ThreeDokument8 SeitenRisk Management Chapter ThreeDaniel filmonNoch keine Bewertungen

- Insurance by Ahsan IlahiDokument9 SeitenInsurance by Ahsan IlahiBusiness JournalsNoch keine Bewertungen

- A Project Report On Consumer PerceptionDokument106 SeitenA Project Report On Consumer PerceptionAKSHIT VERMANoch keine Bewertungen

- Calculate Life Insurance PremiumsDokument5 SeitenCalculate Life Insurance PremiumsRahat KhanNoch keine Bewertungen

- Insurance CompanyDokument2 SeitenInsurance CompanyPramod Kumar NishadNoch keine Bewertungen

- Risk AssignmentDokument11 SeitenRisk AssignmentAmanuel HabtamuNoch keine Bewertungen

- Marketing (Introduction of Insurance)Dokument9 SeitenMarketing (Introduction of Insurance)Yog CoolNoch keine Bewertungen

- Basic Principles of Life InsuranceDokument44 SeitenBasic Principles of Life InsuranceAlanNoch keine Bewertungen

- FAIS AssignmentDokument17 SeitenFAIS AssignmentSalman SaeedNoch keine Bewertungen

- Module II Risk and UncertainityDokument11 SeitenModule II Risk and UncertainityJebin JamesNoch keine Bewertungen

- Lecture 8Dokument15 SeitenLecture 8Rahul ReddyNoch keine Bewertungen

- Profit SharingDokument20 SeitenProfit SharingDumitru TudorNoch keine Bewertungen

- Term Paper 2000cDokument9 SeitenTerm Paper 2000cJaybee GuintoNoch keine Bewertungen

- Financial Markets and Instruments 9Dokument17 SeitenFinancial Markets and Instruments 9Zhichang ZhangNoch keine Bewertungen

- Slic InsuranceDokument109 SeitenSlic InsuranceAnmol GuptaNoch keine Bewertungen

- Module 1 Introduction of InsuranceDokument16 SeitenModule 1 Introduction of InsuranceAniket KaleNoch keine Bewertungen

- Name: Raza Ali.: Roll No: (2k20/BBAE/133) Subject:Insurance Class: BBA Part 2 Evening. Dept:IBADokument14 SeitenName: Raza Ali.: Roll No: (2k20/BBAE/133) Subject:Insurance Class: BBA Part 2 Evening. Dept:IBARashdullah Shah 133Noch keine Bewertungen

- A Project Report On "Consumer Perception Towards Insurance Sector"Dokument107 SeitenA Project Report On "Consumer Perception Towards Insurance Sector"ilomuNoch keine Bewertungen

- Insurance: Pooling of LossesDokument12 SeitenInsurance: Pooling of LossesNafiz RahmanNoch keine Bewertungen

- Marine InsuranceDokument201 SeitenMarine Insurancejasmina.mushy22Noch keine Bewertungen

- The Microeconomics of InsuranceDokument163 SeitenThe Microeconomics of InsuranceJuanacho001Noch keine Bewertungen

- CHAPTER 4 - InsuranceDokument134 SeitenCHAPTER 4 - InsuranceMuneera Zakaria75% (8)

- 23terminology - English SectionDokument115 Seiten23terminology - English Sectionobadfaisal24Noch keine Bewertungen

- Chapter 12 (Updated Oct 5)Dokument29 SeitenChapter 12 (Updated Oct 5)Zoe LamNoch keine Bewertungen

- Rmip PDFDokument176 SeitenRmip PDFBala ArvindNoch keine Bewertungen

- Avoid These 3 Social Security PitfallsDokument9 SeitenAvoid These 3 Social Security PitfallsSundar RamanathanNoch keine Bewertungen

- Actuarial Two. Unit 1Dokument50 SeitenActuarial Two. Unit 1Mohamedi ZuberiNoch keine Bewertungen

- Root Cause Analysis For Employee TurnoverDokument77 SeitenRoot Cause Analysis For Employee TurnoverRani Gujari100% (4)

- Risk CH 3Dokument9 SeitenRisk CH 3Tadele BekeleNoch keine Bewertungen

- Safe Money First: Your Guidebook to Annuities and Safe Retirement Financial Planning StrategiesVon EverandSafe Money First: Your Guidebook to Annuities and Safe Retirement Financial Planning StrategiesNoch keine Bewertungen

- Tax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingVon EverandTax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingNoch keine Bewertungen

- Risk Management: How to Use Different Insurance to Your BenefitVon EverandRisk Management: How to Use Different Insurance to Your BenefitNoch keine Bewertungen

- Reg 198 NsoutreachtDokument2 SeitenReg 198 NsoutreachtDavid DorrNoch keine Bewertungen

- Gerova Financial GroupDokument20 SeitenGerova Financial GroupDavid DorrNoch keine Bewertungen

- Lisa Actuarial Tables Female Smoker ANBDokument1 SeiteLisa Actuarial Tables Female Smoker ANBDavid DorrNoch keine Bewertungen

- SocGen New World OrderDokument18 SeitenSocGen New World Ordera_sarosh7050Noch keine Bewertungen

- Lisa Actuarial Tables Female Smoker ANBDokument1 SeiteLisa Actuarial Tables Female Smoker ANBDavid DorrNoch keine Bewertungen

- ILMA Purchase and Sale AgreementDokument30 SeitenILMA Purchase and Sale AgreementDavid Dorr100% (1)

- ING Change of Ownership InterceptionDokument3 SeitenING Change of Ownership InterceptionDavid DorrNoch keine Bewertungen

- Lisa Actuarial Tables Female Smoker ANBDokument1 SeiteLisa Actuarial Tables Female Smoker ANBDavid DorrNoch keine Bewertungen

- Caldwell COIDokument2 SeitenCaldwell COIDavid DorrNoch keine Bewertungen

- Trade Report June 09Dokument9 SeitenTrade Report June 09David DorrNoch keine Bewertungen

- Sec 3-24-10Dokument13 SeitenSec 3-24-10David DorrNoch keine Bewertungen

- Trade Report January 09Dokument11 SeitenTrade Report January 09David DorrNoch keine Bewertungen

- Trade Report February 09Dokument7 SeitenTrade Report February 09David DorrNoch keine Bewertungen

- Trade Report December 08Dokument11 SeitenTrade Report December 08David DorrNoch keine Bewertungen

- Trade Report May 09Dokument10 SeitenTrade Report May 09David DorrNoch keine Bewertungen

- Trade Report April 09Dokument11 SeitenTrade Report April 09David DorrNoch keine Bewertungen

- Trade Report March 09Dokument9 SeitenTrade Report March 09David DorrNoch keine Bewertungen

- Quadratic Stochastic Intensity and Prospective Mortality TablesDokument43 SeitenQuadratic Stochastic Intensity and Prospective Mortality TablesDavid DorrNoch keine Bewertungen

- The Volatility of MortalityDokument26 SeitenThe Volatility of MortalityDavid DorrNoch keine Bewertungen

- Survivor DerivativesDokument34 SeitenSurvivor DerivativesDavid DorrNoch keine Bewertungen

- The Design of Securitization For Longevity RiskDokument52 SeitenThe Design of Securitization For Longevity RiskDavid DorrNoch keine Bewertungen

- The Role of Longevity Bonds in Optimal PortfolioDokument17 SeitenThe Role of Longevity Bonds in Optimal PortfolioDavid DorrNoch keine Bewertungen

- Securitizing and Tranching Longevity ExposuresDokument41 SeitenSecuritizing and Tranching Longevity ExposuresDavid DorrNoch keine Bewertungen

- Stochastic Portfolio Specific MortalityDokument20 SeitenStochastic Portfolio Specific MortalityDavid DorrNoch keine Bewertungen

- Securitized Senior Life SettlementsDokument20 SeitenSecuritized Senior Life SettlementsDavid DorrNoch keine Bewertungen

- Q Forwards JP MorganDokument4 SeitenQ Forwards JP MorganDavid DorrNoch keine Bewertungen

- Static Hedging Effectiveness For Longevity RiskDokument35 SeitenStatic Hedging Effectiveness For Longevity RiskDavid DorrNoch keine Bewertungen

- Pricing Longevity Bonds Using Implied Survival ProbabilitiesDokument21 SeitenPricing Longevity Bonds Using Implied Survival ProbabilitiesDavid DorrNoch keine Bewertungen

- Open Source PresentationDokument10 SeitenOpen Source PresentationDavid DorrNoch keine Bewertungen

- Options On Normal UnderlyingsDokument29 SeitenOptions On Normal UnderlyingsDavid DorrNoch keine Bewertungen

- Gmail - Claims Medical Rejection - CIR - 2023 - 150000 - 0298788Dokument2 SeitenGmail - Claims Medical Rejection - CIR - 2023 - 150000 - 0298788Ramesh DhamiNoch keine Bewertungen

- GR No 73887 Great Pacific Life Assurance Corp V Judico & NLRCDokument2 SeitenGR No 73887 Great Pacific Life Assurance Corp V Judico & NLRCRuel ReyesNoch keine Bewertungen

- If1 Examination Guide For Exams From 1 January 2023 To 31 December 2023 PDFDokument29 SeitenIf1 Examination Guide For Exams From 1 January 2023 To 31 December 2023 PDFJ Ferns100% (1)

- AIA Star Shield Plus Brochure Nov2013Dokument16 SeitenAIA Star Shield Plus Brochure Nov2013spacevibesNoch keine Bewertungen

- Summer Internship Report Aim IndiaDokument74 SeitenSummer Internship Report Aim IndiaKartik JainNoch keine Bewertungen

- EY Commercial Real Estate DebtDokument16 SeitenEY Commercial Real Estate DebtPaul BalbinNoch keine Bewertungen

- Edillon V Manila BankersDokument2 SeitenEdillon V Manila BankersGabe BedanaNoch keine Bewertungen

- Cila Property Sig Reinstatement Basis of Settlement Final VersionDokument9 SeitenCila Property Sig Reinstatement Basis of Settlement Final Version23985811Noch keine Bewertungen

- Ammaar HassanDokument2 SeitenAmmaar HassanDanish IqbalNoch keine Bewertungen

- MGT211 Shortnotes 1 To 45 LecDokument12 SeitenMGT211 Shortnotes 1 To 45 LecEngr Imtiaz Hussain GilaniNoch keine Bewertungen

- FormOfCoverNote_Motor Insurance DetailsDokument2 SeitenFormOfCoverNote_Motor Insurance Detailscommission sompoNoch keine Bewertungen

- Bullet Notes 9 - Other Percentage TaxDokument4 SeitenBullet Notes 9 - Other Percentage TaxFlores Renato Jr. S.Noch keine Bewertungen

- Insurance Law ReviewerDokument35 SeitenInsurance Law Reviewerisraeljamora100% (4)

- To, Vivian, PA PDFDokument22 SeitenTo, Vivian, PA PDFVivianToNoch keine Bewertungen

- Pioneer Review, October 11, 2012Dokument16 SeitenPioneer Review, October 11, 2012surfnewmediaNoch keine Bewertungen

- SEC Schedule 14D-9 Filing by Tasty Baking Company Regarding Tender Offer by Flowers FoodsDokument77 SeitenSEC Schedule 14D-9 Filing by Tasty Baking Company Regarding Tender Offer by Flowers Foodskg17Noch keine Bewertungen

- DT20229919409 OlDokument20 SeitenDT20229919409 OlDattatray PokleNoch keine Bewertungen

- Corporate Profile State LifeDokument56 SeitenCorporate Profile State LifeSana AliNoch keine Bewertungen

- Stockyard Days 2018Dokument16 SeitenStockyard Days 2018Lillie NewspapersNoch keine Bewertungen

- 3005 159959535 00 B00 Py PDFDokument2 Seiten3005 159959535 00 B00 Py PDFmonuNoch keine Bewertungen

- United States Court of Appeals For The Third CircuitDokument18 SeitenUnited States Court of Appeals For The Third CircuitScribd Government DocsNoch keine Bewertungen

- Insutance LawDokument2 SeitenInsutance LawTarakasish GhoshNoch keine Bewertungen

- Family Must KnowDokument16 SeitenFamily Must KnowKhalilahmad Khatri83% (6)

- IRDA SA3 Exam Study of Indian General Insurance MarketsDokument4 SeitenIRDA SA3 Exam Study of Indian General Insurance MarketsVignesh Srinivasan100% (1)

- Bajaj Allianz General Insurance Company LTDDokument1 SeiteBajaj Allianz General Insurance Company LTDseshu 2010Noch keine Bewertungen

- CEILLI - New - Edition - Questions (English-Set - 2) 2024Dokument15 SeitenCEILLI - New - Edition - Questions (English-Set - 2) 2024littleaskar 77Noch keine Bewertungen

- Asmita Gaha Magar InsuranceDokument6 SeitenAsmita Gaha Magar InsuranceNikhil Visa ServicesNoch keine Bewertungen

- PV - CoADokument28 SeitenPV - CoArian_defriNoch keine Bewertungen

- Result PDFDokument1 SeiteResult PDFAnonymous WWihP9Noch keine Bewertungen