Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Common Accounting System For PACSDokument43 SeitenCommon Accounting System For PACSanilpanmandNoch keine Bewertungen

- Construction Internal Audit ProgramDokument17 SeitenConstruction Internal Audit ProgramDasthagiriBhasha75% (4)

- Dimensional Fund Advisors 2002 Case SoluDokument3 SeitenDimensional Fund Advisors 2002 Case SoluPawan PoollaNoch keine Bewertungen

- Etoro Forex Trading Course - First LessonDokument19 SeitenEtoro Forex Trading Course - First LessonTrading Guru100% (4)

- Chapter 14Dokument18 SeitenChapter 14RenNoch keine Bewertungen

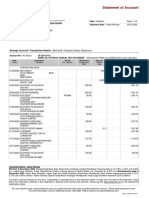

- Statement of Account: No 15 Jalan Awana 12 Taman Cheras Awana 43200 Batu 9 Cheras, SelangorDokument5 SeitenStatement of Account: No 15 Jalan Awana 12 Taman Cheras Awana 43200 Batu 9 Cheras, Selangorputri nurishaNoch keine Bewertungen

- Alexion PharmaceuticalsDokument3 SeitenAlexion PharmaceuticalsHristo VasilevNoch keine Bewertungen

- Dole Food CompanyDokument6 SeitenDole Food CompanyHristo VasilevNoch keine Bewertungen

- World Population Prospects: The 2012 RevisionDokument5 SeitenWorld Population Prospects: The 2012 RevisionHristo VasilevNoch keine Bewertungen

- Paris Orl Ans Statuts MAJ 20141128 ENG CleanDokument10 SeitenParis Orl Ans Statuts MAJ 20141128 ENG CleanHristo VasilevNoch keine Bewertungen

- 2010 09 Nett Made With LoveDokument6 Seiten2010 09 Nett Made With LoveHristo VasilevNoch keine Bewertungen

- Ceo 2.0Dokument33 SeitenCeo 2.0Kleiner Perkins Caufield & Byers100% (1)

- 2 Pre-Election Plays To Maximize Your Income in 2012: by Jeff Fischer, Advisor, Motley Fool ProDokument6 Seiten2 Pre-Election Plays To Maximize Your Income in 2012: by Jeff Fischer, Advisor, Motley Fool ProHristo VasilevNoch keine Bewertungen

- The Role of Oligarchs in RussiaDokument20 SeitenThe Role of Oligarchs in RussiaHristo VasilevNoch keine Bewertungen

- Internship Report MTMDokument45 SeitenInternship Report MTMusmanaltafNoch keine Bewertungen

- Investment Office ANRS: Project Profile On The Establishment of Absorbent Cotton Making PlantDokument29 SeitenInvestment Office ANRS: Project Profile On The Establishment of Absorbent Cotton Making Plantabel_kayelNoch keine Bewertungen

- Under The Supervision of MR .Pradeep Singh Kala Isd Head Sbi Mutual Fund (J & K)Dokument57 SeitenUnder The Supervision of MR .Pradeep Singh Kala Isd Head Sbi Mutual Fund (J & K)Faizan NazirNoch keine Bewertungen

- MCQ On Guidance Note CARODokument63 SeitenMCQ On Guidance Note CAROUma Suryanarayanan100% (1)

- HDFC MF Transaction-Slip-18.7 PDFDokument1 SeiteHDFC MF Transaction-Slip-18.7 PDFPrasad PnNoch keine Bewertungen

- An Analysis of Personal Financial Literacy Among College StudentsDokument22 SeitenAn Analysis of Personal Financial Literacy Among College StudentsMade WillyNoch keine Bewertungen

- DU M.Com Information Brochure 2015Dokument14 SeitenDU M.Com Information Brochure 2015Neepur GargNoch keine Bewertungen

- Case A Case B Case CDokument2 SeitenCase A Case B Case Ckhiladi883Noch keine Bewertungen

- LO 7 - Bagian 6&7Dokument5 SeitenLO 7 - Bagian 6&7Sekar Ayu Kartika SariNoch keine Bewertungen

- R13-Brand ValuationDokument3 SeitenR13-Brand ValuationYashi GuptaNoch keine Bewertungen

- Accounting For InventoriesDokument32 SeitenAccounting For InventoriesShery HashmiNoch keine Bewertungen

- Ai Hidayati Amminy BT Ahmad AmminyDokument6 SeitenAi Hidayati Amminy BT Ahmad AmminyhidayatiamminyNoch keine Bewertungen

- Daftar Akun Rumah Cantik HanaDokument4 SeitenDaftar Akun Rumah Cantik HanaLSP SMKN 1 BanjarmasinNoch keine Bewertungen

- I M B M +® Æ I " T ( "' : H V™ T JDokument26 SeitenI M B M +® Æ I " T ( "' : H V™ T JPratik GazalwarNoch keine Bewertungen

- Accounting For Governmental & Nonprofit 16e Solution Manual Chapter 17Dokument24 SeitenAccounting For Governmental & Nonprofit 16e Solution Manual Chapter 17sellertbsm2014Noch keine Bewertungen

- PWT 90Dokument1.315 SeitenPWT 90burcakkaplanNoch keine Bewertungen

- ExmDokument18 SeitenExmRoy Mitz Bautista0% (2)

- Types of Audit AssignmentDokument21 SeitenTypes of Audit AssignmentKanika GoelNoch keine Bewertungen

- Inter Corporate Loans, Investments, Gaurantees and SecuritiesDokument29 SeitenInter Corporate Loans, Investments, Gaurantees and SecuritiesManik Singh KapoorNoch keine Bewertungen

- Final Ass. 2 Malinao Kathleen S. BSBAHRM 2 3DDokument4 SeitenFinal Ass. 2 Malinao Kathleen S. BSBAHRM 2 3DHanna Ruth FloreceNoch keine Bewertungen

- FinalDokument31 SeitenFinalAniruddha RantuNoch keine Bewertungen

- Five Star Training Academy: NerangDokument1 SeiteFive Star Training Academy: NeranghemssNoch keine Bewertungen

- Business Environment 1 PDF PDFDokument35 SeitenBusiness Environment 1 PDF PDFDave NNoch keine Bewertungen

- The Effect of Economic Value Added FreeDokument15 SeitenThe Effect of Economic Value Added FreeSumant AlagawadiNoch keine Bewertungen