Das könnte Ihnen auch gefallen

- Warren Buffett Biography PDFDokument8 SeitenWarren Buffett Biography PDFtarana2000100% (6)

- CNBC Transcript 2006 2019 02Dokument1.575 SeitenCNBC Transcript 2006 2019 02N BNoch keine Bewertungen

- Graham Value Investing MetricsDokument2 SeitenGraham Value Investing MetricsfikgangNoch keine Bewertungen

- Ragupati Chandrasekaran's Notes From The Biglari Holdings 2012 Annual MeetingDokument10 SeitenRagupati Chandrasekaran's Notes From The Biglari Holdings 2012 Annual MeetingThe Manual of Ideas100% (1)

- Washington PostBuffett Analysis1Dokument2 SeitenWashington PostBuffett Analysis1Calvin ChangNoch keine Bewertungen

- Engaged Capital's Letter To Abercrombie & FitchDokument9 SeitenEngaged Capital's Letter To Abercrombie & FitchKim BhasinNoch keine Bewertungen

- The 2011 Hays Salary Guide: Sharing Our ExpertiseDokument58 SeitenThe 2011 Hays Salary Guide: Sharing Our ExpertiseTristan YeNoch keine Bewertungen

- Buffett Partner Charlie Munger Has A Side Gig - Designing College Dorms - WSJDokument6 SeitenBuffett Partner Charlie Munger Has A Side Gig - Designing College Dorms - WSJAndri ChandraNoch keine Bewertungen

- Interview With Warren BuffettDokument2 SeitenInterview With Warren BuffettAdii BoaaNoch keine Bewertungen

- Here Are A Few Relevant ExamplesDokument6 SeitenHere Are A Few Relevant ExamplesTeddy RusliNoch keine Bewertungen

- Notes From The 2004 Wesco Annual Meeting: May 5, 2004 Pasadena, CA by Whitney TilsonDokument24 SeitenNotes From The 2004 Wesco Annual Meeting: May 5, 2004 Pasadena, CA by Whitney Tilsonshadysbr0kenNoch keine Bewertungen

- Harvest Interview Series Ori Eyal of Emerging Value Capital ManagementDokument6 SeitenHarvest Interview Series Ori Eyal of Emerging Value Capital ManagementCanadianValueNoch keine Bewertungen

- Bruce BerkowitzDokument35 SeitenBruce BerkowitznewbietraderNoch keine Bewertungen

- A Trillion-Dollar BusinessDokument6 SeitenA Trillion-Dollar BusinesssiewyukNoch keine Bewertungen

- Letters of The Manager Since 1998Dokument111 SeitenLetters of The Manager Since 1998Lukas SavickasNoch keine Bewertungen

- 5-Year-Old Billionaire Charlie Munger: The Secret To A Long and Happy Life Is 'So Simple'Dokument2 Seiten5-Year-Old Billionaire Charlie Munger: The Secret To A Long and Happy Life Is 'So Simple'MAR LUKBANNoch keine Bewertungen

- Markel Breakfast 2011 NotesDokument9 SeitenMarkel Breakfast 2011 NotesbenclaremonNoch keine Bewertungen

- Geico Case Study f17Dokument4 SeitenGeico Case Study f17ezra koenigNoch keine Bewertungen

- Greenhaven Road Capital Q1 2017Dokument12 SeitenGreenhaven Road Capital Q1 2017superinvestorbulletiNoch keine Bewertungen

- Prem Watsa - The 2 Billion Dollar Man - Toronto Live - 04-2009Dokument6 SeitenPrem Watsa - The 2 Billion Dollar Man - Toronto Live - 04-2009Damon MengNoch keine Bewertungen

- EMBA Applied Value Investing (Ajdler) SP2016Dokument3 SeitenEMBA Applied Value Investing (Ajdler) SP2016darwin12Noch keine Bewertungen

- MIT Sloan PDFDokument12 SeitenMIT Sloan PDFJai KamdarNoch keine Bewertungen

- 1976 Buffett Letter About Geico - FutureBlindDokument4 Seiten1976 Buffett Letter About Geico - FutureBlindPradeep RaghunathanNoch keine Bewertungen

- PremWatsaFairfaxNewsletter7 12-20-11Dokument6 SeitenPremWatsaFairfaxNewsletter7 12-20-11able1Noch keine Bewertungen

- Dempster Mills Manufacturing Case Study BPLsDokument15 SeitenDempster Mills Manufacturing Case Study BPLstycoonshan24Noch keine Bewertungen

- An Investment Only A Mother Could Love The Case For Natural Resource EquitiesDokument12 SeitenAn Investment Only A Mother Could Love The Case For Natural Resource EquitiessuperinvestorbulletiNoch keine Bewertungen

- Value Investor Forum Presentation 2015 (Print Version)Dokument29 SeitenValue Investor Forum Presentation 2015 (Print Version)streettalk700Noch keine Bewertungen

- Three Hours With Warren - Complete Transcript - 2008-08-22Dokument62 SeitenThree Hours With Warren - Complete Transcript - 2008-08-22drunkdealmasterNoch keine Bewertungen

- Chou LettersDokument90 SeitenChou LettersLuke ConstableNoch keine Bewertungen

- Sequoia Fund Investor Day Transcript - May 20th 2011Dokument20 SeitenSequoia Fund Investor Day Transcript - May 20th 2011colinwalt99Noch keine Bewertungen

- Warren Buffett: "The Investor of Today Does Not Profit From Yesterday'S Growth"Dokument19 SeitenWarren Buffett: "The Investor of Today Does Not Profit From Yesterday'S Growth"Anshul AggarwalNoch keine Bewertungen

- Wally Weitz Letter To ShareholdersDokument2 SeitenWally Weitz Letter To ShareholdersAnonymous j5tXg7onNoch keine Bewertungen

- Michael L Riordan, The Founder and CEO of Gilead Sciences, and Warren E Buffett, Berkshire Hathaway Chairman: CorrespondenceDokument5 SeitenMichael L Riordan, The Founder and CEO of Gilead Sciences, and Warren E Buffett, Berkshire Hathaway Chairman: CorrespondenceOpenSquareCommons100% (27)

- Warren Buffett CNBC Transcript Feb-29-2016 PDFDokument92 SeitenWarren Buffett CNBC Transcript Feb-29-2016 PDFAndri ChandraNoch keine Bewertungen

- BH 2015 AmDokument14 SeitenBH 2015 Amva.apg.90100% (2)

- Kevin Byun's Q1 2010 Denali Investors LetterDokument9 SeitenKevin Byun's Q1 2010 Denali Investors LetterThe Manual of IdeasNoch keine Bewertungen

- Value: InvestorDokument4 SeitenValue: InvestorAlex WongNoch keine Bewertungen

- Market Cap To GDP An Updated Look at The Buffett Valuation IndicatorDokument7 SeitenMarket Cap To GDP An Updated Look at The Buffett Valuation IndicatorRamon AmorimNoch keine Bewertungen

- Profiles in Investing - Rich Pzena (Bottom Line 2003)Dokument2 SeitenProfiles in Investing - Rich Pzena (Bottom Line 2003)tatsrus1Noch keine Bewertungen

- Charlie Munger 2005-2013 (Minus Harvard-Westlake)Dokument171 SeitenCharlie Munger 2005-2013 (Minus Harvard-Westlake)Kevin MartelliNoch keine Bewertungen

- Glenn GreenbergDokument3 SeitenGlenn Greenbergannsusan21Noch keine Bewertungen

- Personality (Warren Buffett)Dokument13 SeitenPersonality (Warren Buffett)Pratik TambeNoch keine Bewertungen

- BuybacksDokument22 SeitenBuybackssamson1190Noch keine Bewertungen

- Amitabh Singhvi L MOI Interview L JUNE-2011Dokument6 SeitenAmitabh Singhvi L MOI Interview L JUNE-2011Wayne GonsalvesNoch keine Bewertungen

- Wesco Shareholder Letter 2007Dokument7 SeitenWesco Shareholder Letter 2007eblochNoch keine Bewertungen

- Bruce Berkowitz On WFC 90sDokument4 SeitenBruce Berkowitz On WFC 90sVu Latticework PoetNoch keine Bewertungen

- C S II C S II: ASE Tudy ASE TudyDokument20 SeitenC S II C S II: ASE Tudy ASE TudyMarcel GozaliNoch keine Bewertungen

- 5x5x5 InterviewDokument7 Seiten5x5x5 InterviewspachecofdzNoch keine Bewertungen

- Profiles in Investing - Mario Gabelli Bottom Line 2003)Dokument2 SeitenProfiles in Investing - Mario Gabelli Bottom Line 2003)tatsrus1Noch keine Bewertungen

- 50 Master Moves That Shaped Berkshire Hathaway Outlook BusinessDokument35 Seiten50 Master Moves That Shaped Berkshire Hathaway Outlook BusinessesconieNoch keine Bewertungen

- Graham & Doddsville Spring 2011 NewsletterDokument27 SeitenGraham & Doddsville Spring 2011 NewsletterOld School ValueNoch keine Bewertungen

- Life Advice: Be Careful of Life Advice: Nassim Taleb Randomness The Black Swan AntifragilityDokument6 SeitenLife Advice: Be Careful of Life Advice: Nassim Taleb Randomness The Black Swan AntifragilitybrightstarNoch keine Bewertungen

- Insight: Prime PropertiesDokument8 SeitenInsight: Prime PropertiesvahssNoch keine Bewertungen

- The Nifty Fifty - Joe Kusnan's BlogDokument2 SeitenThe Nifty Fifty - Joe Kusnan's BlogPradeep RaghunathanNoch keine Bewertungen

- Schloss 2006Dokument2 SeitenSchloss 2006Logic Gate Capital100% (1)

- Inner Scorecard Vs Outer ScorecardDokument4 SeitenInner Scorecard Vs Outer ScorecardKavish DangNoch keine Bewertungen

- David Einhorn MSFT Speech-2006Dokument5 SeitenDavid Einhorn MSFT Speech-2006mikesfbayNoch keine Bewertungen

- Warren Buffett HistoryDokument7 SeitenWarren Buffett HistoryAamir KhanNoch keine Bewertungen

- Warren Buffett Biography: PreferredDokument7 SeitenWarren Buffett Biography: PreferredVikas NkNoch keine Bewertungen

- Value Investing in India: Gurus:-Warren Buffett BiographyDokument6 SeitenValue Investing in India: Gurus:-Warren Buffett BiographyPragati OberoiNoch keine Bewertungen

- Warren Buffett ProjectDokument20 SeitenWarren Buffett ProjectAlin ApostolescuNoch keine Bewertungen

- LODR NotesDokument33 SeitenLODR NotestirthankarNoch keine Bewertungen

- FABV - PresentationDokument12 SeitenFABV - PresentationPuneet MalhotraNoch keine Bewertungen

- Ebook PDF Comparative Income Taxation A Structural Analysis 3rd Edition Revised PDFDokument47 SeitenEbook PDF Comparative Income Taxation A Structural Analysis 3rd Edition Revised PDFrubin.smith411100% (37)

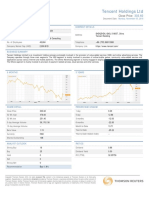

- Tencent Holdings LTD: Close PriceDokument2 SeitenTencent Holdings LTD: Close PricetrungNoch keine Bewertungen

- Cash Flow Analysis Lyst5937Dokument5 SeitenCash Flow Analysis Lyst5937Vibhav SinghNoch keine Bewertungen

- Financial Report Pertamina 2019 English Version-RevDokument186 SeitenFinancial Report Pertamina 2019 English Version-RevAlim FirdausNoch keine Bewertungen

- Module 14 Financial Instruments and Equity Investments at Fair Value TheoryDokument2 SeitenModule 14 Financial Instruments and Equity Investments at Fair Value TheoryKendrew SujideNoch keine Bewertungen

- Invesrment in Debt InstrumentsDokument2 SeitenInvesrment in Debt InstrumentsElla MontefalcoNoch keine Bewertungen

- Globiva Services Private Limited - Company Profile, Directors, Revenue & MoreDokument7 SeitenGlobiva Services Private Limited - Company Profile, Directors, Revenue & Moreroshankumar078673Noch keine Bewertungen

- 9706 w17 QP 11Dokument11 Seiten9706 w17 QP 11Vinetha KarunanithiNoch keine Bewertungen

- Capital StructureDokument13 SeitenCapital StructureRam SharmaNoch keine Bewertungen

- External?file Income-StatementDokument2 SeitenExternal?file Income-StatementAntonette JeniebreNoch keine Bewertungen

- Calculation On SpreadsheetDokument2 SeitenCalculation On SpreadsheetsnehalbhirudNoch keine Bewertungen

- Advanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FDokument7 SeitenAdvanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FJames CantorneNoch keine Bewertungen

- ConvergEx Traders Guide 2014 Q3Dokument168 SeitenConvergEx Traders Guide 2014 Q3thisthat7Noch keine Bewertungen

- MAS Review MaterialDokument14 SeitenMAS Review MaterialJemar Murillo DalaganNoch keine Bewertungen

- Chapter 4 Cost of CapitalDokument19 SeitenChapter 4 Cost of CapitalmedrekNoch keine Bewertungen

- ReporttDokument7 SeitenReporttaryan nicoleNoch keine Bewertungen

- Assignment June 2022Dokument3 SeitenAssignment June 2022AirForce ManNoch keine Bewertungen

- Akl Edisi TerbaruDokument46 SeitenAkl Edisi TerbaruemakNoch keine Bewertungen

- Consolidations: Chapter-6Dokument54 SeitenConsolidations: Chapter-6Ram KumarNoch keine Bewertungen

- Bank Valuation - FE FIG TryoutDokument5 SeitenBank Valuation - FE FIG Tryoutcharlotte.zibautNoch keine Bewertungen

- SMEDA Spices Processing, Packing & Marketing111Dokument6 SeitenSMEDA Spices Processing, Packing & Marketing111Jahangir AliNoch keine Bewertungen

- HLLQP QuickFact FormulaSheet 2016Dokument2 SeitenHLLQP QuickFact FormulaSheet 2016nandhinigrmNoch keine Bewertungen

- ACC 178 SAS Module 25Dokument14 SeitenACC 178 SAS Module 25maria isayNoch keine Bewertungen

- WORKSHEET (Lembar Jawaban)Dokument2 SeitenWORKSHEET (Lembar Jawaban)I Gede Wahyu krisna DarmaNoch keine Bewertungen

- متطلبات القياس و الافصاح المحاسبي عن رأس المال الفكري و أثره على القوائم المالية لمنظمات الأعمالDokument24 Seitenمتطلبات القياس و الافصاح المحاسبي عن رأس المال الفكري و أثره على القوائم المالية لمنظمات الأعمالNour MezianeNoch keine Bewertungen

- (5032) - OFFICIALLY Assignment 1Dokument19 Seiten(5032) - OFFICIALLY Assignment 1Nguyen Khanh Ly (FGW HN)Noch keine Bewertungen

- Cost of Goods Sold: Sales CommissionDokument7 SeitenCost of Goods Sold: Sales Commissionaparna153Noch keine Bewertungen