Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- View From The Next Rung - Moving From Staff To Senior AccountantDokument3 SeitenView From The Next Rung - Moving From Staff To Senior AccountantJill Edmonds, Communications DirectorNoch keine Bewertungen

- The Write Stuff - Improving Accounting Students' Writing SkillsDokument6 SeitenThe Write Stuff - Improving Accounting Students' Writing SkillsJill Edmonds, Communications DirectorNoch keine Bewertungen

- New Fun With Fund Balances - Implementing GASB 54Dokument5 SeitenNew Fun With Fund Balances - Implementing GASB 54Jill Edmonds, Communications DirectorNoch keine Bewertungen

- Dealing With Poor Performers ... Start With The EnablersDokument2 SeitenDealing With Poor Performers ... Start With The EnablersJill Edmonds, Communications DirectorNoch keine Bewertungen

- Career vs. Culture - Do You Have To Choose?Dokument2 SeitenCareer vs. Culture - Do You Have To Choose?Jill Edmonds, Communications DirectorNoch keine Bewertungen

- Cash Is King - Utilize Cost Segregation StudiesDokument5 SeitenCash Is King - Utilize Cost Segregation StudiesJill Edmonds, Communications DirectorNoch keine Bewertungen

- Sarbanes-Oxley - Friend or Foe?Dokument5 SeitenSarbanes-Oxley - Friend or Foe?Jill Edmonds, Communications DirectorNoch keine Bewertungen

- Class Notes - Accounting Education in 2010Dokument6 SeitenClass Notes - Accounting Education in 2010Jill Edmonds, Communications DirectorNoch keine Bewertungen

- Delegation - Dumping or EmpoweringDokument3 SeitenDelegation - Dumping or EmpoweringJill Edmonds, Communications DirectorNoch keine Bewertungen

- Portfolio Diversification - Where It Goes WrongDokument4 SeitenPortfolio Diversification - Where It Goes WrongJill Edmonds, Communications DirectorNoch keine Bewertungen

- Full Speed Ahead - 4 Ways To Set Your CPA Career in MotionDokument2 SeitenFull Speed Ahead - 4 Ways To Set Your CPA Career in MotionJill Edmonds, Communications DirectorNoch keine Bewertungen

- Getting in The Financial Planning GameDokument4 SeitenGetting in The Financial Planning GameJill Edmonds, Communications DirectorNoch keine Bewertungen

- Primer On Virginia's Pass-Through Entity Withholding RulesDokument4 SeitenPrimer On Virginia's Pass-Through Entity Withholding RulesJill Edmonds, Communications DirectorNoch keine Bewertungen

- An RX For Health Care Woes - CPAs and Firms Can Manage Health Care Costs NowDokument4 SeitenAn RX For Health Care Woes - CPAs and Firms Can Manage Health Care Costs NowJill Edmonds, Communications DirectorNoch keine Bewertungen

- Are You Ready To Serve On A Nonprofit BoardDokument4 SeitenAre You Ready To Serve On A Nonprofit BoardJill Edmonds, Communications Director100% (1)

- Government Contracting - Look Before You LeapDokument8 SeitenGovernment Contracting - Look Before You LeapJill Edmonds, Communications DirectorNoch keine Bewertungen

- The Virtual CFODokument5 SeitenThe Virtual CFOJill Edmonds, Communications DirectorNoch keine Bewertungen

- Keep Your Head Above The Clouds - Cloud Computing TrendsDokument4 SeitenKeep Your Head Above The Clouds - Cloud Computing TrendsJill Edmonds, Communications DirectorNoch keine Bewertungen

- 5 Ways To Get SuedDokument2 Seiten5 Ways To Get SuedJill Edmonds, Communications DirectorNoch keine Bewertungen

- Manage The Next Generation CPA FirmDokument2 SeitenManage The Next Generation CPA FirmJill Edmonds, Communications DirectorNoch keine Bewertungen

- Communicate Better. Get ResultsDokument2 SeitenCommunicate Better. Get ResultsJill Edmonds, Communications DirectorNoch keine Bewertungen

- Difficult Conversations - How To Destroy Your OpponentDokument2 SeitenDifficult Conversations - How To Destroy Your OpponentJill Edmonds, Communications DirectorNoch keine Bewertungen

- Speak Volumes Without Saying A Word ... Through ListeningDokument2 SeitenSpeak Volumes Without Saying A Word ... Through ListeningJill Edmonds, Communications DirectorNoch keine Bewertungen

- Sketch Your CPA FutureDokument2 SeitenSketch Your CPA FutureJill Edmonds, Communications DirectorNoch keine Bewertungen

- An XBRL Starter GuideDokument4 SeitenAn XBRL Starter GuideJill Edmonds, Communications DirectorNoch keine Bewertungen

- Exploring The Social Media FrontierDokument4 SeitenExploring The Social Media FrontierJill Edmonds, Communications DirectorNoch keine Bewertungen

- Going Green With Recent LegislationDokument4 SeitenGoing Green With Recent LegislationJill Edmonds, Communications DirectorNoch keine Bewertungen

- Forgive & Forget? Decoding Bankruptcy Debt Forgiveness RulesDokument4 SeitenForgive & Forget? Decoding Bankruptcy Debt Forgiveness RulesJill Edmonds, Communications DirectorNoch keine Bewertungen

- Staying Active in The New Year: Having (And Keeping) Your CPA License Unlocks A World of PossibilitiesDokument2 SeitenStaying Active in The New Year: Having (And Keeping) Your CPA License Unlocks A World of PossibilitiesJill Edmonds, Communications DirectorNoch keine Bewertungen

- Chapter 9 Capital Budgeting PDFDokument112 SeitenChapter 9 Capital Budgeting PDFtharinduNoch keine Bewertungen

- Corporation TaxationDokument16 SeitenCorporation TaxationMeg Lee0% (1)

- Rossari Biotech IPO Note Analyzes Specialty Chemical MakerDokument8 SeitenRossari Biotech IPO Note Analyzes Specialty Chemical Makerzeeshan_iraniNoch keine Bewertungen

- Corporation Law Quiz 1Dokument5 SeitenCorporation Law Quiz 1Paul Ryan VillanuevaNoch keine Bewertungen

- Going Concern Asset Based Valuation Financial ModelDokument4 SeitenGoing Concern Asset Based Valuation Financial ModelJessica PaludipanNoch keine Bewertungen

- Accounting 1 1 Hour 30 Minutes (30 Questions) Answer All QuestionsDokument11 SeitenAccounting 1 1 Hour 30 Minutes (30 Questions) Answer All QuestionsNurin QistinaNoch keine Bewertungen

- Substantive Test of Intangible Assets, Prepaid Expenses (Autosaved)Dokument38 SeitenSubstantive Test of Intangible Assets, Prepaid Expenses (Autosaved)Mej AgaoNoch keine Bewertungen

- Golf club's exclusive voting rights disputeDokument4 SeitenGolf club's exclusive voting rights disputeIsabella RodriguezNoch keine Bewertungen

- Topic 4 - Events After Reporting Period (IAS 10)Dokument15 SeitenTopic 4 - Events After Reporting Period (IAS 10)CavipsotNoch keine Bewertungen

- The Growth in Corporate Governance CodesDokument15 SeitenThe Growth in Corporate Governance CodesSudip BaruaNoch keine Bewertungen

- IB Presentation BMWDokument21 SeitenIB Presentation BMWMayank GaurNoch keine Bewertungen

- 12 Test 2 Aud339 June 2022 SS 1 PDFDokument5 Seiten12 Test 2 Aud339 June 2022 SS 1 PDFNUR LYANA INANI AZMINoch keine Bewertungen

- FAU Questions & Answer PackDokument3 SeitenFAU Questions & Answer PackDawn CaldeiraNoch keine Bewertungen

- Reynaldo Gulane CleanersDokument3 SeitenReynaldo Gulane CleanersshaneemacasiNoch keine Bewertungen

- Advanced Taxation - Solutions To Pilot Questions Suggested Solution To Question 1Dokument23 SeitenAdvanced Taxation - Solutions To Pilot Questions Suggested Solution To Question 1Oyebisi OpeyemiNoch keine Bewertungen

- FIN254 Project NSU (Excel File)Dokument6 SeitenFIN254 Project NSU (Excel File)Sirazum SaadNoch keine Bewertungen

- Winding Up of A CompanyDokument14 SeitenWinding Up of A CompanyUday KiranNoch keine Bewertungen

- Analysis and Interpretation of Financial StatementsDokument16 SeitenAnalysis and Interpretation of Financial StatementsKimberly FloresNoch keine Bewertungen

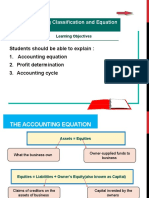

- Accounting Equation and Profit DeterminationDokument19 SeitenAccounting Equation and Profit DeterminationNor LailyNoch keine Bewertungen

- Full Download Corporate Finance A Focused Approach 5th Edition Ehrhardt Solutions ManualDokument36 SeitenFull Download Corporate Finance A Focused Approach 5th Edition Ehrhardt Solutions Manualkisslingcicelypro100% (34)

- Free Cash FlowsDokument8 SeitenFree Cash FlowsParvesh AghiNoch keine Bewertungen

- Samsung Understanding FS Tutorial QuestionsDokument5 SeitenSamsung Understanding FS Tutorial QuestionsLim ShawnNoch keine Bewertungen

- Financial Management (FM) Solution Pack: S. No ACCA Exam Paper Topics CoveredDokument64 SeitenFinancial Management (FM) Solution Pack: S. No ACCA Exam Paper Topics CoveredKoketso MogweNoch keine Bewertungen

- Insurance Business Plan Template SummaryDokument15 SeitenInsurance Business Plan Template SummarygargramNoch keine Bewertungen

- Finanzas Internacionales: Ejercicios de La Tarea 2Dokument8 SeitenFinanzas Internacionales: Ejercicios de La Tarea 2gerardoNoch keine Bewertungen

- 4PPT Financial StatementsDokument21 Seiten4PPT Financial Statements이시연Noch keine Bewertungen

- 8 Source A4: 9706/33/INSERT/O/N/21 © UCLES 2021Dokument2 Seiten8 Source A4: 9706/33/INSERT/O/N/21 © UCLES 2021Ayesha sheikhNoch keine Bewertungen

- Top 10 CFO responsibilities under 40 charactersDokument3 SeitenTop 10 CFO responsibilities under 40 charactersMita Mandal0% (1)

- Audit of Cash and Cash Equivalents Internal ControlsDokument7 SeitenAudit of Cash and Cash Equivalents Internal ControlsmoNoch keine Bewertungen

- SBI@ Your Door StepDokument2 SeitenSBI@ Your Door StepDynamic LevelsNoch keine Bewertungen