Das könnte Ihnen auch gefallen

- Open Compensation Plan A Complete Guide - 2020 EditionVon EverandOpen Compensation Plan A Complete Guide - 2020 EditionNoch keine Bewertungen

- Questionnaire On Quality CircleDokument3 SeitenQuestionnaire On Quality CirclesumiNoch keine Bewertungen

- Public Service Motivation A Complete Guide - 2021 EditionVon EverandPublic Service Motivation A Complete Guide - 2021 EditionNoch keine Bewertungen

- Tata Mutual Fund 2Dokument14 SeitenTata Mutual Fund 2mahesh2037100% (1)

- Coca Cola RemonDokument6 SeitenCoca Cola Remonremon4hrNoch keine Bewertungen

- MHR Questions For QuizDokument2 SeitenMHR Questions For Quizratnesh737Noch keine Bewertungen

- A Presentation On Job Enrichment: Presented by C.SravanthiDokument9 SeitenA Presentation On Job Enrichment: Presented by C.SravanthiChandra SravanthiNoch keine Bewertungen

- Human Resource Selection and Development Across Cultures: Learning Objectives and Summary of The ChapterDokument31 SeitenHuman Resource Selection and Development Across Cultures: Learning Objectives and Summary of The ChapterLinh HoangNoch keine Bewertungen

- Drmrmbs GoDokument18 SeitenDrmrmbs GovenkatasubramaniyanNoch keine Bewertungen

- Research Project Report Template - Final MBADokument20 SeitenResearch Project Report Template - Final MBARajni KumariNoch keine Bewertungen

- 1 Questionnaire FinalDokument105 Seiten1 Questionnaire FinalKashif KhanNoch keine Bewertungen

- Student - Chapter 7Dokument3 SeitenStudent - Chapter 7Steven PaulNoch keine Bewertungen

- Competency Mapping - ToyotaDokument7 SeitenCompetency Mapping - ToyotaSureshNoch keine Bewertungen

- Project CHAPTER3Dokument28 SeitenProject CHAPTER3sailaja sasiNoch keine Bewertungen

- Questionnaire Business ResearchDokument9 SeitenQuestionnaire Business ResearchjebatmalanglagiNoch keine Bewertungen

- Modern Methods of Performance Appraisal by Anshul AryaDokument18 SeitenModern Methods of Performance Appraisal by Anshul AryaHardik KothiyalNoch keine Bewertungen

- Business Intelligence Unit 1 Chapter 2Dokument13 SeitenBusiness Intelligence Unit 1 Chapter 2vivekNoch keine Bewertungen

- A Study On Employee Welfare Measures in BhelDokument19 SeitenA Study On Employee Welfare Measures in BhelLovely ashwinNoch keine Bewertungen

- Questa Education Foundation Loan Terms and Conditions and Payment NoteDokument6 SeitenQuesta Education Foundation Loan Terms and Conditions and Payment NoteInstitute for Higher Education PolicyNoch keine Bewertungen

- Employee Development and Taklent ManagementDokument5 SeitenEmployee Development and Taklent ManagementIvan DanielNoch keine Bewertungen

- Questionnaire Layout Total Questions in A Questionnaire: Minimum 15Dokument18 SeitenQuestionnaire Layout Total Questions in A Questionnaire: Minimum 15suman v bhatNoch keine Bewertungen

- Module 3 Multiple Choice QuizDokument6 SeitenModule 3 Multiple Choice QuizMag9191Noch keine Bewertungen

- I-Sem-Statistical Methods For Decision MakingDokument1 SeiteI-Sem-Statistical Methods For Decision MakingVijayakannan VNoch keine Bewertungen

- Bharat ElectronicsDokument13 SeitenBharat ElectronicsKirti MishraNoch keine Bewertungen

- Sharpe Single Index ModelDokument11 SeitenSharpe Single Index ModelSai Mala100% (1)

- Summary, Findings, Conclusions and SuggestionsDokument23 SeitenSummary, Findings, Conclusions and Suggestionsashish kumalNoch keine Bewertungen

- PROJECT MANAGEMENT FINAL EXAM-shubham.033Dokument7 SeitenPROJECT MANAGEMENT FINAL EXAM-shubham.033Jæy SäwärñNoch keine Bewertungen

- Udai Pareek Chapter 2Dokument17 SeitenUdai Pareek Chapter 2Trilok BankerNoch keine Bewertungen

- Chap 027Dokument25 SeitenChap 027ducacapupuNoch keine Bewertungen

- Sumit Final Project of Work Life BalanceDokument102 SeitenSumit Final Project of Work Life BalancetejasNoch keine Bewertungen

- Job Description-Academic CounsellorDokument1 SeiteJob Description-Academic CounsellorChirag Jain CjNoch keine Bewertungen

- Conventional Versus Non Conventional Cash4079Dokument10 SeitenConventional Versus Non Conventional Cash4079Amna SaeedNoch keine Bewertungen

- Presentation On HR Department of Mobilink.Dokument18 SeitenPresentation On HR Department of Mobilink.Sadaf YaqoobNoch keine Bewertungen

- 2015JULB02046 - Wealth Management Assignment-1Dokument19 Seiten2015JULB02046 - Wealth Management Assignment-1Prasanth TalluriNoch keine Bewertungen

- Chap 02Dokument29 SeitenChap 02eh38Noch keine Bewertungen

- Reasoning Questions - Inequalities Set 2Dokument5 SeitenReasoning Questions - Inequalities Set 2kavinkumareceNoch keine Bewertungen

- Fair Enough? Big Business Embraces Fair TradeDokument4 SeitenFair Enough? Big Business Embraces Fair TradeMantas SinkeviciusNoch keine Bewertungen

- Poster Community Engagement - Final POSTERDokument1 SeitePoster Community Engagement - Final POSTERHafeez ShaikhNoch keine Bewertungen

- Perception of Employees On Performance AppraisalDokument76 SeitenPerception of Employees On Performance AppraisalRahul MinochaNoch keine Bewertungen

- The Impact of Non Financial Rewards On Employee Motivation in Apparel Industry in Nuwaraeliya DistrictDokument12 SeitenThe Impact of Non Financial Rewards On Employee Motivation in Apparel Industry in Nuwaraeliya Districtgeethanjali champikaNoch keine Bewertungen

- Question 1 FaDokument6 SeitenQuestion 1 Fajavariah irshadNoch keine Bewertungen

- Chapter 1Dokument13 SeitenChapter 1lishpa123Noch keine Bewertungen

- BRM SSSDokument17 SeitenBRM SSSAvinash SinghNoch keine Bewertungen

- Tuga Ketiga PMMKDokument3 SeitenTuga Ketiga PMMKERika PratiwiNoch keine Bewertungen

- The Career Maturity Inventory Revised A Preliminary Psychometric InvestigationDokument17 SeitenThe Career Maturity Inventory Revised A Preliminary Psychometric InvestigationJorge Luis Villacís Nieto100% (1)

- Human Resources Management System McdonaldDokument6 SeitenHuman Resources Management System McdonaldWaqas BaigNoch keine Bewertungen

- Chapter 1 Introduction To Employee Training and DevelopmentDokument20 SeitenChapter 1 Introduction To Employee Training and DevelopmentSadaf Waheed100% (1)

- Determination of Forward and Futures Prices: Practice QuestionsDokument3 SeitenDetermination of Forward and Futures Prices: Practice Questionshoai_hm2357Noch keine Bewertungen

- QUIZ - Revision - AnswersDokument8 SeitenQUIZ - Revision - AnswersSyakira WahidaNoch keine Bewertungen

- Gopal Cotton Mills LTD Case StudyDokument4 SeitenGopal Cotton Mills LTD Case StudyDeepanshu VarshneyNoch keine Bewertungen

- Reliance Communication HDokument4 SeitenReliance Communication HVansh SetiyaNoch keine Bewertungen

- CH (10) - Book AnswersDokument17 SeitenCH (10) - Book AnswersabdulraufdghaybeejNoch keine Bewertungen

- Kritika Questionnaire 1Dokument2 SeitenKritika Questionnaire 1Pulkit Jauhari100% (1)

- A Study On HR Kaleidoscope Career at Nediyosoft Technologies ChennaiDokument5 SeitenA Study On HR Kaleidoscope Career at Nediyosoft Technologies ChennaiVijay Anand0% (1)

- HRM PPT UpdatedDokument13 SeitenHRM PPT Updatedkannanb666Noch keine Bewertungen

- 2122promana HW5 G5Dokument10 Seiten2122promana HW5 G5Minh TríNoch keine Bewertungen

- SAPMDokument6 SeitenSAPMShivam PopatNoch keine Bewertungen

- FM Class Notes Day1Dokument5 SeitenFM Class Notes Day1febycvNoch keine Bewertungen

- On LevisDokument16 SeitenOn LevisMeenakshi Jayaraman0% (1)

- Practice Questions For Final ExamDokument8 SeitenPractice Questions For Final ExamChivajeetNoch keine Bewertungen

- Nature and Context of Research 2Dokument2 SeitenNature and Context of Research 2vanvunNoch keine Bewertungen

- The Central Bank & Monetary Policy PDFDokument9 SeitenThe Central Bank & Monetary Policy PDFvanvunNoch keine Bewertungen

- Investment Companies and Pension FundsDokument10 SeitenInvestment Companies and Pension FundsvanvunNoch keine Bewertungen

- The Central Bank & Monetary Policy PDFDokument9 SeitenThe Central Bank & Monetary Policy PDFvanvunNoch keine Bewertungen

- GK For Class TestDokument3 SeitenGK For Class TestvanvunNoch keine Bewertungen

- Multiple Choice Questions On Ratio and ProportionDokument1 SeiteMultiple Choice Questions On Ratio and ProportionvanvunNoch keine Bewertungen

- Nature and Context of Research 1Dokument16 SeitenNature and Context of Research 1vanvunNoch keine Bewertungen

- Notes For Students Amalgamation 2Dokument4 SeitenNotes For Students Amalgamation 2vanvunNoch keine Bewertungen

- LBC 12Dokument4 SeitenLBC 12vanvunNoch keine Bewertungen

- Logical ReasoningDokument3 SeitenLogical ReasoningvanvunNoch keine Bewertungen

- Business LawDokument3 SeitenBusiness LawvanvunNoch keine Bewertungen

- Business LawDokument3 SeitenBusiness LawvanvunNoch keine Bewertungen

- Multiple Choice Questions On Ratio and ProportionDokument1 SeiteMultiple Choice Questions On Ratio and Proportionvanvun100% (3)

- Interdependence Between Micro and Macro EconomicsDokument1 SeiteInterdependence Between Micro and Macro Economicsvanvun0% (1)

- Costing and Cost AccountingDokument1 SeiteCosting and Cost AccountingvanvunNoch keine Bewertungen

- Notes For Students Amalgamation 1Dokument3 SeitenNotes For Students Amalgamation 1vanvunNoch keine Bewertungen

- AmalgamationDokument8 SeitenAmalgamationvanvunNoch keine Bewertungen

- DRDokument2 SeitenDRvanvunNoch keine Bewertungen

- AmalgamationDokument8 SeitenAmalgamationvanvunNoch keine Bewertungen

- Importance of OBDokument1 SeiteImportance of OBvanvunNoch keine Bewertungen

- Capital Gain TaxDokument3 SeitenCapital Gain TaxvanvunNoch keine Bewertungen

- Capital Gain TaxDokument3 SeitenCapital Gain TaxvanvunNoch keine Bewertungen

- Importance of OBDokument3 SeitenImportance of OBvanvunNoch keine Bewertungen

- Concept of Commercial Banks of NepalDokument2 SeitenConcept of Commercial Banks of Nepalvanvun100% (1)

- Teacher Vacant Announcement 1Dokument2 SeitenTeacher Vacant Announcement 1vanvunNoch keine Bewertungen

- Implications of Baumol's Sales Revenue Maximization ModelDokument1 SeiteImplications of Baumol's Sales Revenue Maximization ModelvanvunNoch keine Bewertungen

- Importance of OBDokument1 SeiteImportance of OBvanvunNoch keine Bewertungen

- Concept of Commercial Banks of Nepa1Dokument8 SeitenConcept of Commercial Banks of Nepa1vanvunNoch keine Bewertungen

- Concept of Commercial Banks of NepalDokument2 SeitenConcept of Commercial Banks of Nepalvanvun100% (1)

- Liquidity Management in BanksDokument28 SeitenLiquidity Management in BanksvanvunNoch keine Bewertungen

- Investor Presentation As On 31st March 2019Dokument34 SeitenInvestor Presentation As On 31st March 2019Vaibhav ChauhanNoch keine Bewertungen

- ACT349 F13 Assignment and Solutions For Sep 25 Tutorial v12Dokument10 SeitenACT349 F13 Assignment and Solutions For Sep 25 Tutorial v12Crystal B. WongNoch keine Bewertungen

- Sample Interview QuestionsDokument4 SeitenSample Interview QuestionsDeepakNoch keine Bewertungen

- Accounting Records and SystemsDokument22 SeitenAccounting Records and SystemsMarai ParativoNoch keine Bewertungen

- The Bank of Nova ScotiaDokument18 SeitenThe Bank of Nova Scotiakash32192Noch keine Bewertungen

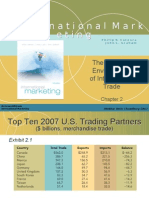

- International Marketing Chapter 2 (The Dynamic Environment of International Trade)Dokument39 SeitenInternational Marketing Chapter 2 (The Dynamic Environment of International Trade)Nitin Jain0% (1)

- Government of Tamil Nadu Department of Industries and CommerceDokument6 SeitenGovernment of Tamil Nadu Department of Industries and Commercesalam20064909100% (3)

- 2009-04-03 181856 ReviewDokument18 Seiten2009-04-03 181856 ReviewAnbang XiaoNoch keine Bewertungen

- CH15 16 SolutionsDokument22 SeitenCH15 16 Solutionsstaynam100% (2)

- Financial Institutions and Markets - Foreign Exchange MarketsDokument19 SeitenFinancial Institutions and Markets - Foreign Exchange MarketsSiddhartha saiNoch keine Bewertungen

- Absorption Vs Variable CostingDokument8 SeitenAbsorption Vs Variable CostingMary JaneNoch keine Bewertungen

- Galectin Therapeutics: Equity Research ReportDokument40 SeitenGalectin Therapeutics: Equity Research ReportResearchWorks360Noch keine Bewertungen

- FFMC Rbi DocsDokument51 SeitenFFMC Rbi DocsManikNoch keine Bewertungen

- CPA Quizzer v.1 by Themahatma (CPAR 2016)Dokument9 SeitenCPA Quizzer v.1 by Themahatma (CPAR 2016)John Mahatma Agripa100% (1)

- N7Dokument13 SeitenN7Hứa Trí TínNoch keine Bewertungen

- A Beginners' Guide To Commodity Market (Spot and Futures)Dokument47 SeitenA Beginners' Guide To Commodity Market (Spot and Futures)vintosh_pNoch keine Bewertungen

- PuregoldDokument9 SeitenPuregoldCarmina BacunganNoch keine Bewertungen

- Diversification Strategy KennyDokument5 SeitenDiversification Strategy KennyThanh Tu NguyenNoch keine Bewertungen

- Rax CollectionDokument46 SeitenRax CollectionNaveen Tharanga GunarathnaNoch keine Bewertungen

- Commercial Team Communication Plan: Project NameDokument2 SeitenCommercial Team Communication Plan: Project NameScribdNoch keine Bewertungen

- ManPro-6 Present Worth Analysis 2019Dokument45 SeitenManPro-6 Present Worth Analysis 2019Syifa Fauziah RustoniNoch keine Bewertungen

- "How Well Am I Doing?" Statement of Cash Flows: Mcgraw-Hill/IrwinDokument23 Seiten"How Well Am I Doing?" Statement of Cash Flows: Mcgraw-Hill/Irwinrayjoshua12Noch keine Bewertungen

- 18 007004 PDFDokument206 Seiten18 007004 PDFBrenda HerringNoch keine Bewertungen

- Tarsier Press Release Novosol JV March 3 2016Dokument2 SeitenTarsier Press Release Novosol JV March 3 2016api-299059809Noch keine Bewertungen

- 3660Dokument13 Seiten3660lengocthangNoch keine Bewertungen

- Reasonable AssuranceDokument12 SeitenReasonable AssuranceHossein DavaniNoch keine Bewertungen

- Greg - Speicher Ways To Improve Your Investment Process PDFDokument37 SeitenGreg - Speicher Ways To Improve Your Investment Process PDFRajeev BahugunaNoch keine Bewertungen

- Pinto 03Dokument19 SeitenPinto 03jahanzebNoch keine Bewertungen

- Distressed Debt PrezDokument32 SeitenDistressed Debt Prezmacondo06100% (2)

- Lecture 5 Optimal Risky PortfoliosDokument28 SeitenLecture 5 Optimal Risky PortfoliosLuisLoNoch keine Bewertungen

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNVon Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNBewertung: 4.5 von 5 Sternen4.5/5 (3)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaVon EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaBewertung: 4.5 von 5 Sternen4.5/5 (14)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisVon EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisBewertung: 5 von 5 Sternen5/5 (6)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialVon EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialBewertung: 4.5 von 5 Sternen4.5/5 (32)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthVon EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthBewertung: 4 von 5 Sternen4/5 (20)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successVon EverandReady, Set, Growth hack:: A beginners guide to growth hacking successBewertung: 4.5 von 5 Sternen4.5/5 (93)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistVon EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistBewertung: 4.5 von 5 Sternen4.5/5 (73)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursVon EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursBewertung: 4.5 von 5 Sternen4.5/5 (8)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingVon EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingBewertung: 4.5 von 5 Sternen4.5/5 (17)

- Finance Basics (HBR 20-Minute Manager Series)Von EverandFinance Basics (HBR 20-Minute Manager Series)Bewertung: 4.5 von 5 Sternen4.5/5 (32)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaVon EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaBewertung: 3.5 von 5 Sternen3.5/5 (8)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelVon Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNoch keine Bewertungen

- Private Equity and Venture Capital in Europe: Markets, Techniques, and DealsVon EverandPrivate Equity and Venture Capital in Europe: Markets, Techniques, and DealsBewertung: 5 von 5 Sternen5/5 (1)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistVon EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistBewertung: 4 von 5 Sternen4/5 (32)

- Financial Risk Management: A Simple IntroductionVon EverandFinancial Risk Management: A Simple IntroductionBewertung: 4.5 von 5 Sternen4.5/5 (7)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanVon EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanBewertung: 4.5 von 5 Sternen4.5/5 (79)

- Mind over Money: The Psychology of Money and How to Use It BetterVon EverandMind over Money: The Psychology of Money and How to Use It BetterBewertung: 4 von 5 Sternen4/5 (24)

- Joy of Agility: How to Solve Problems and Succeed SoonerVon EverandJoy of Agility: How to Solve Problems and Succeed SoonerBewertung: 4 von 5 Sternen4/5 (1)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetVon EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetBewertung: 5 von 5 Sternen5/5 (2)

- Creating Shareholder Value: A Guide For Managers And InvestorsVon EverandCreating Shareholder Value: A Guide For Managers And InvestorsBewertung: 4.5 von 5 Sternen4.5/5 (8)

- How to Measure Anything: Finding the Value of Intangibles in BusinessVon EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessBewertung: 3.5 von 5 Sternen3.5/5 (4)

- Value: The Four Cornerstones of Corporate FinanceVon EverandValue: The Four Cornerstones of Corporate FinanceBewertung: 4.5 von 5 Sternen4.5/5 (18)