Das könnte Ihnen auch gefallen

- Example 2Dokument5 SeitenExample 2malingapereraNoch keine Bewertungen

- All Sums CostingDokument14 SeitenAll Sums Costingshankarinadar100% (1)

- Budgetary Control: BY Animesh Kalita 2K10MKT37Dokument15 SeitenBudgetary Control: BY Animesh Kalita 2K10MKT37Animesh KalitaNoch keine Bewertungen

- تمارين +الحل اداريةDokument14 Seitenتمارين +الحل اداريةaec216320136Noch keine Bewertungen

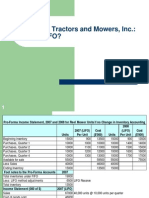

- FDP - Merrimack Tractors and Mowers, Inc.Dokument13 SeitenFDP - Merrimack Tractors and Mowers, Inc.Devyani SinghNoch keine Bewertungen

- ParticularDokument9 SeitenParticularPravat gurungNoch keine Bewertungen

- Power Cost Per Hour 20 Operator Cost Per Hour 45 Annual Repairs 40000 Depreciation 25000 Insurance 15000 Estimate Number of Hours 5000 Compute The Machine Hour Rate Computation of Machine Hour RateDokument12 SeitenPower Cost Per Hour 20 Operator Cost Per Hour 45 Annual Repairs 40000 Depreciation 25000 Insurance 15000 Estimate Number of Hours 5000 Compute The Machine Hour Rate Computation of Machine Hour Rateamitinfo_mishraNoch keine Bewertungen

- Acn 4Dokument3 SeitenAcn 4Navidul IslamNoch keine Bewertungen

- AFM-Session 25Dokument13 SeitenAFM-Session 25abhijit.kundu23-25Noch keine Bewertungen

- Income Statement OutputDokument2 SeitenIncome Statement OutputAsad HussainNoch keine Bewertungen

- Chapter 15Dokument7 SeitenChapter 15Rahila RafiqNoch keine Bewertungen

- CMA AssignmentDokument4 SeitenCMA AssignmentniranjanaNoch keine Bewertungen

- MEA AssignmentDokument13 SeitenMEA Assignmentankit07777100% (1)

- Ques On Process CostingDokument4 SeitenQues On Process CostingIsha ShaikhNoch keine Bewertungen

- Marginal CostingDokument9 SeitenMarginal CostingSharika EpNoch keine Bewertungen

- Management Accounting 21.1.11 QuestionsDokument5 SeitenManagement Accounting 21.1.11 QuestionsAmeya TalankiNoch keine Bewertungen

- Vakho Tako SalomeDokument27 SeitenVakho Tako SalomerbegalashviliNoch keine Bewertungen

- Chapter 4 ExerciseDokument7 SeitenChapter 4 ExerciseJoe DicksonNoch keine Bewertungen

- Accounting For Decision Making Xavier Institute of Management, Bhubaneswar PGDM - I, End TermDokument19 SeitenAccounting For Decision Making Xavier Institute of Management, Bhubaneswar PGDM - I, End TermAbhijeet DashNoch keine Bewertungen

- Cost SheetDokument3 SeitenCost Sheetruchi_rohilla9603Noch keine Bewertungen

- Going Rate PricingDokument3 SeitenGoing Rate PricingHarshitha RNoch keine Bewertungen

- Process CostingDokument17 SeitenProcess CostingSweta JaiswalNoch keine Bewertungen

- Decision Making1Dokument6 SeitenDecision Making1Sourav OjhaNoch keine Bewertungen

- Manufacturing Financial CostingDokument15 SeitenManufacturing Financial CostingJoeFSabaterNoch keine Bewertungen

- Cost Accounting 2013Dokument3 SeitenCost Accounting 2013GuruKPO0% (1)

- Assignment Cost Sheet SumsDokument3 SeitenAssignment Cost Sheet SumsMamta PrajapatiNoch keine Bewertungen

- Chapter 22Dokument14 SeitenChapter 22Nguyên BảoNoch keine Bewertungen

- Case 2 - Cost - Sheet - Pepe - Denim PDFDokument3 SeitenCase 2 - Cost - Sheet - Pepe - Denim PDFKrutarthChaudhariNoch keine Bewertungen

- Author: Author:: 290000 0.75 Due To Resale at Lesser Than Market PriceDokument16 SeitenAuthor: Author:: 290000 0.75 Due To Resale at Lesser Than Market PricektsnlNoch keine Bewertungen

- Problems On Cost SheetDokument3 SeitenProblems On Cost Sheetvikasevil75Noch keine Bewertungen

- CVP Analysis Inclass Ass Key 9qansDokument3 SeitenCVP Analysis Inclass Ass Key 9qansNaga NagendraNoch keine Bewertungen

- Budgetary Control, Mar Cost c0st ST, Res AcDokument29 SeitenBudgetary Control, Mar Cost c0st ST, Res AcYashasvi MohandasNoch keine Bewertungen

- Cost BehaviourDokument7 SeitenCost BehaviourAstu GraitoNoch keine Bewertungen

- Math Accounting by AtaurDokument28 SeitenMath Accounting by AtaurShajib KhanNoch keine Bewertungen

- MG T 402 Subjective SolvedDokument8 SeitenMG T 402 Subjective SolvedAhsan Khan KhanNoch keine Bewertungen

- Accounting Techniques For Decision MakingDokument24 SeitenAccounting Techniques For Decision MakingRima PrajapatiNoch keine Bewertungen

- Management AccountingDokument12 SeitenManagement AccountingKathlyn Ann MasilNoch keine Bewertungen

- Given:: Problem 6 - 21: Prepare & Reconcile Variable Costing StatementsDokument13 SeitenGiven:: Problem 6 - 21: Prepare & Reconcile Variable Costing StatementsimjiyaNoch keine Bewertungen

- Quiz For Finals For PrintingDokument4 SeitenQuiz For Finals For PrintingPopol KupaNoch keine Bewertungen

- BudgetDokument9 SeitenBudgetDrBharti KeswaniNoch keine Bewertungen

- Managerial Control & BudgetingDokument2 SeitenManagerial Control & Budgetingmohdzarrin77Noch keine Bewertungen

- Assignment ProblemDokument7 SeitenAssignment ProblemAnantha KrishnaNoch keine Bewertungen

- BudgetingDokument11 SeitenBudgetingTanuj LalchandaniNoch keine Bewertungen

- Chapter Xvii Decisions Involving Alternative Choices SolutionsDokument6 SeitenChapter Xvii Decisions Involving Alternative Choices Solutionsshital_vyas1987Noch keine Bewertungen

- Practical Problems On PV RatioDokument7 SeitenPractical Problems On PV Ratiohrmohan8667% (3)

- Cost SheetDokument5 SeitenCost Sheetpooja45650% (2)

- Management AccountingDokument68 SeitenManagement AccountingNekibur DeepNoch keine Bewertungen

- Cost Sheet ProblemsDokument22 SeitenCost Sheet ProblemsAvinash Tanawade100% (4)

- Budegetory ControlDokument34 SeitenBudegetory ControlDurdana NasserNoch keine Bewertungen

- Cost Volume Profit Analysis (Decision Making) - TaskDokument9 SeitenCost Volume Profit Analysis (Decision Making) - TaskAshwin KarthikNoch keine Bewertungen

- Pile cp2Dokument108 SeitenPile cp2casarokarNoch keine Bewertungen

- Primus Industries - TOC Case StudyDokument2 SeitenPrimus Industries - TOC Case StudySUJIT SONAWANENoch keine Bewertungen

- Variable and Absorption M 02Dokument6 SeitenVariable and Absorption M 02sm munNoch keine Bewertungen

- Merrion ProductsDokument11 SeitenMerrion ProductsVivek NarayananNoch keine Bewertungen

- Ma QuestionsDokument2 SeitenMa QuestionsnaxahejNoch keine Bewertungen

- Additional Flexible Budget ProblemDokument2 SeitenAdditional Flexible Budget Problemaishwarya raikarNoch keine Bewertungen

- Commercial & Service Industry Machinery, Miscellaneous World Summary: Market Values & Financials by CountryVon EverandCommercial & Service Industry Machinery, Miscellaneous World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- Steering & Steering Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryVon EverandSteering & Steering Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- Commercial & Industrial Equipment Repair & Maintenance Revenues World Summary: Market Values & Financials by CountryVon EverandCommercial & Industrial Equipment Repair & Maintenance Revenues World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- Equity Program FAQDokument14 SeitenEquity Program FAQNikhil SinghalNoch keine Bewertungen

- Real Estate Development by Ahmad Saifudin MutaqiDokument91 SeitenReal Estate Development by Ahmad Saifudin MutaqiKevin AnandaNoch keine Bewertungen

- Royalty and Hire PurchaseDokument4 SeitenRoyalty and Hire PurchaseJaved Khan100% (1)

- Eicher MotorsDokument16 SeitenEicher MotorsjehanbhadhaNoch keine Bewertungen

- Ghulam PDFDokument1 SeiteGhulam PDFNazir Ahmad GanieNoch keine Bewertungen

- IAS 17 LeaseDokument7 SeitenIAS 17 LeaseMaqsoodNoch keine Bewertungen

- Practicalweek48 0809answersDokument8 SeitenPracticalweek48 0809answersLaura BasalicNoch keine Bewertungen

- Linear Programming: I Sem LPP Quant-IDokument27 SeitenLinear Programming: I Sem LPP Quant-IBabitha RaghuNoch keine Bewertungen

- MIS PresentationDokument11 SeitenMIS PresentationAman Singh RajputNoch keine Bewertungen

- MAnagerial Economics - Lesson PlanDokument5 SeitenMAnagerial Economics - Lesson Planmukesh040% (1)

- Financial Analysis of Hul and GodrejDokument53 SeitenFinancial Analysis of Hul and GodrejJiwan Jot SinghNoch keine Bewertungen

- Gita Neraca LajurDokument1 SeiteGita Neraca LajurAndri RianNoch keine Bewertungen

- 2113T Feasibility Study TempateDokument27 Seiten2113T Feasibility Study TempateRA MagallanesNoch keine Bewertungen

- North South University: Introduction To Financial Management FIN254 Pharma Aids Limited Beacon Pharmaceuticals LimitedDokument33 SeitenNorth South University: Introduction To Financial Management FIN254 Pharma Aids Limited Beacon Pharmaceuticals LimitedShafin RahmanNoch keine Bewertungen

- ProblemsDokument4 SeitenProblemsUNKNOWNNNoch keine Bewertungen

- 403b PlansDokument2 Seiten403b Plansapi-246909910Noch keine Bewertungen

- Heritage Foods Discounted Cash Flow Valuation CaseDokument9 SeitenHeritage Foods Discounted Cash Flow Valuation CasePriya DurejaNoch keine Bewertungen

- Case Digest Cir vs. BoacDokument1 SeiteCase Digest Cir vs. BoacAnn SC100% (5)

- Business Plan Worksheet SpainDokument28 SeitenBusiness Plan Worksheet Spainsilcab67Noch keine Bewertungen

- H. Family IncomeDokument29 SeitenH. Family IncomeFahad AkmadNoch keine Bewertungen

- A Marketing Plan For HSBC NomanDokument8 SeitenA Marketing Plan For HSBC Nomanhassan_MuqarrabNoch keine Bewertungen

- City Government of San Pablo V ReyesDokument2 SeitenCity Government of San Pablo V ReyesNikita BayotNoch keine Bewertungen

- 1smied Vs CirDokument2 Seiten1smied Vs CirBam BathanNoch keine Bewertungen

- Case Digest Incomplete TaxDokument135 SeitenCase Digest Incomplete TaxHencel GumabayNoch keine Bewertungen

- Ticket To Your UC Retirement-UCRP Presentation Fall 2016 FinalDokument42 SeitenTicket To Your UC Retirement-UCRP Presentation Fall 2016 FinalkramynotNoch keine Bewertungen

- Lakme: Latest Quarterly/Halfyearly As On (Months)Dokument7 SeitenLakme: Latest Quarterly/Halfyearly As On (Months)Vikas UpadhyayNoch keine Bewertungen

- X Engineering EconomicsDokument39 SeitenX Engineering EconomicsMikaellaTeniolaNoch keine Bewertungen

- Capital Structure TheoriesDokument13 SeitenCapital Structure Theoriesಮಂಜುನಾಥ್ ರಂಪುರೆ ಎಸ್Noch keine Bewertungen

- Tally ERP 9 Notes + Practical Assignment - Free Download PDFDokument19 SeitenTally ERP 9 Notes + Practical Assignment - Free Download PDFHimanshu Saha50% (2)

- Pre-Feasibility Study: Tea CompanyDokument20 SeitenPre-Feasibility Study: Tea CompanyIPro PkNoch keine Bewertungen