Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Police PatrolDokument130 SeitenPolice PatrolEcho EchoNoch keine Bewertungen

- #25 Magno V CADokument2 Seiten#25 Magno V CAGladys CubiasNoch keine Bewertungen

- Proposal For The Crestwood Plaza Redevelopment Area by UrbanStreet - Crestwood, MODokument52 SeitenProposal For The Crestwood Plaza Redevelopment Area by UrbanStreet - Crestwood, MOnextSTL.comNoch keine Bewertungen

- 1 Mile.: # Speed Last Race # Prime Power # Class Rating # Best Speed at DistDokument8 Seiten1 Mile.: # Speed Last Race # Prime Power # Class Rating # Best Speed at DistNick RamboNoch keine Bewertungen

- The Lion of Judah PDFDokument19 SeitenThe Lion of Judah PDFMichael SympsonNoch keine Bewertungen

- Fund Selector EditionDokument3 SeitenFund Selector Editionapi-26324170Noch keine Bewertungen

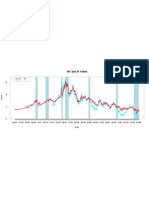

- 10Y and 2Y YieldsDokument1 Seite10Y and 2Y Yieldsapi-26324170Noch keine Bewertungen

- 10yr 2yrDokument1 Seite10yr 2yrapi-26324170Noch keine Bewertungen

- Equities and Tobin's QDokument18 SeitenEquities and Tobin's Qapi-26324170Noch keine Bewertungen

- Gold and Your PortfolioDokument7 SeitenGold and Your Portfolioapi-26324170Noch keine Bewertungen

- Growth of $1 Invested in S&P 500 During 1970s: 10YR - BONDDokument1 SeiteGrowth of $1 Invested in S&P 500 During 1970s: 10YR - BONDapi-26324170Noch keine Bewertungen

- Nomura EquityResearch The Business of AgeingDokument136 SeitenNomura EquityResearch The Business of Ageingstarbak777Noch keine Bewertungen

- Where's The Smoking Gun? A Study of Underwriting Standards For US Subprime MortgagesDokument38 SeitenWhere's The Smoking Gun? A Study of Underwriting Standards For US Subprime Mortgagesapi-26324170Noch keine Bewertungen

- RHYTHM JAIN - RKMP - NZM - 8april23 - 8201794717Dokument3 SeitenRHYTHM JAIN - RKMP - NZM - 8april23 - 8201794717Puru AppNoch keine Bewertungen

- All India Bank Officers AssociationDokument14 SeitenAll India Bank Officers AssociationIndiranNoch keine Bewertungen

- Jones v. Superior CourtDokument4 SeitenJones v. Superior CourtKerriganJamesRoiMaulitNoch keine Bewertungen

- RangeRover P38Dokument75 SeitenRangeRover P3812logapoloNoch keine Bewertungen

- Blends and Digraphs PassagesDokument27 SeitenBlends and Digraphs PassagesAnu Gupta100% (3)

- Read The Passage Given Carefully and Answer The QuestionsDokument2 SeitenRead The Passage Given Carefully and Answer The QuestionsgovinjementahNoch keine Bewertungen

- Civil Application E039 of 2021Dokument4 SeitenCivil Application E039 of 2021Edward NjorogeNoch keine Bewertungen

- Saran Blackbook FinalDokument78 SeitenSaran Blackbook FinalVishnuNadar100% (3)

- Commercial Law Case Digest: List of CasesDokument57 SeitenCommercial Law Case Digest: List of CasesJean Mary AutoNoch keine Bewertungen

- Evidence C13Dokument29 SeitenEvidence C13Aditya SubbaNoch keine Bewertungen

- Ifrs 9 Financial Instruments Using Models in Impairment - AshxDokument38 SeitenIfrs 9 Financial Instruments Using Models in Impairment - Ashxwan nur anisahNoch keine Bewertungen

- Gentileschi's Judith Slaying HolofernesDokument2 SeitenGentileschi's Judith Slaying Holofernesplanet2o100% (3)

- A76XX Series - Dual SIM - Application Note - V1.02Dokument20 SeitenA76XX Series - Dual SIM - Application Note - V1.02vakif.techNoch keine Bewertungen

- Icpo Tesb 2023 1089Dokument6 SeitenIcpo Tesb 2023 1089artificalr1979Noch keine Bewertungen

- Transfer of Property Act ProjectDokument10 SeitenTransfer of Property Act ProjectAshirbad SahooNoch keine Bewertungen

- Minutes of The Meeting GadDokument10 SeitenMinutes of The Meeting GadERIC PASIONNoch keine Bewertungen

- Freedom - What Is Bible Freedom. What Does John 8:32 Promise?Dokument64 SeitenFreedom - What Is Bible Freedom. What Does John 8:32 Promise?kgdieckNoch keine Bewertungen

- Ang Alamat NG GubatDokument5 SeitenAng Alamat NG GubatJason SebastianNoch keine Bewertungen

- "Broken Things" Nehemiah SermonDokument7 Seiten"Broken Things" Nehemiah SermonSarah Collins PrinceNoch keine Bewertungen

- Presentation On Home Loan DocumentationDokument16 SeitenPresentation On Home Loan Documentationmesba_17Noch keine Bewertungen

- Mt. Carmel School of Siargao, Inc.: (Surigao Diocesan School System)Dokument1 SeiteMt. Carmel School of Siargao, Inc.: (Surigao Diocesan School System)EDMAR POLVOROZANoch keine Bewertungen

- HC Bars New Licence For Builders Using Groundwater in GurgaonDokument7 SeitenHC Bars New Licence For Builders Using Groundwater in GurgaonRakeshNoch keine Bewertungen

- Simulation 7 - Payroll Spring-2020Dokument13 SeitenSimulation 7 - Payroll Spring-2020api-519066587Noch keine Bewertungen

- Autocorp Group Vs CA (2004) G.R. No. 157553Dokument2 SeitenAutocorp Group Vs CA (2004) G.R. No. 157553Thea P PorrasNoch keine Bewertungen

- +status Note On Npa/ Stressed Borrower (Rs.5 Crores N Above) Branch-Chennai Zone - Chennai NBG-South M/s Hallmark Living Space Private LimitedDokument2 Seiten+status Note On Npa/ Stressed Borrower (Rs.5 Crores N Above) Branch-Chennai Zone - Chennai NBG-South M/s Hallmark Living Space Private LimitedAbhijit TripathiNoch keine Bewertungen