Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- GFAL Sample ComputationDokument14 SeitenGFAL Sample ComputationIsaac Daplas Rosario73% (11)

- CFA Research Report - Team APUDokument30 SeitenCFA Research Report - Team APUAnonymous 6A1OAiGidZNoch keine Bewertungen

- A Comparative Study of Maritime Operations in IndiaDokument93 SeitenA Comparative Study of Maritime Operations in IndiaSteel Ships100% (1)

- Think Marketing 3rd Edition Tuckwell Test BankDokument24 SeitenThink Marketing 3rd Edition Tuckwell Test BankKitchen UselessNoch keine Bewertungen

- Dahej SIR PresentationDokument26 SeitenDahej SIR PresentationDeepak ThakkerNoch keine Bewertungen

- Coordinate Geometry Calculus PDFDokument6 SeitenCoordinate Geometry Calculus PDFAadithNoch keine Bewertungen

- Fundamentals:: Active Ownership: Driving The ChangeDokument8 SeitenFundamentals:: Active Ownership: Driving The ChangeAadithNoch keine Bewertungen

- Fundamentals May 2015Dokument8 SeitenFundamentals May 2015AadithNoch keine Bewertungen

- Aqa 7404 7405 TN Mass SpectrometryDokument9 SeitenAqa 7404 7405 TN Mass SpectrometryAadithNoch keine Bewertungen

- DNA AS Biology GCE For AQADokument41 SeitenDNA AS Biology GCE For AQAAadith100% (1)

- Central Bank Review: Jimmy Apaa Okello, Beatrice K. Mkenda, Eliab LuvandaDokument14 SeitenCentral Bank Review: Jimmy Apaa Okello, Beatrice K. Mkenda, Eliab LuvandaAdriana AlarcónNoch keine Bewertungen

- Ulrich KohliDokument24 SeitenUlrich KohliyoussefasaadNoch keine Bewertungen

- Sharkhan Valueguide 2016Dokument68 SeitenSharkhan Valueguide 2016Nitesh BajajNoch keine Bewertungen

- 10th Five Year PlanDokument10 Seiten10th Five Year PlanKrishnaveni MurugeshNoch keine Bewertungen

- BIBM101 Class ExerciseDokument4 SeitenBIBM101 Class ExercisePauu HMNoch keine Bewertungen

- Turizmi Ne Jug Te ShqiperiseDokument28 SeitenTurizmi Ne Jug Te Shqiperisediploma detyraNoch keine Bewertungen

- CAT 2000 - Explanations PDFDokument11 SeitenCAT 2000 - Explanations PDFSudiv GullaNoch keine Bewertungen

- Chapter 1 Individuals and GovernmentDokument26 SeitenChapter 1 Individuals and GovernmentHassan Diab SalahNoch keine Bewertungen

- Macroeconomics Principles and Policy 13th Edition Baumol Test Bank 1Dokument70 SeitenMacroeconomics Principles and Policy 13th Edition Baumol Test Bank 1gloria100% (60)

- Prioritization of Food Safety Issues 2019Dokument20 SeitenPrioritization of Food Safety Issues 2019Francis Mwangi ChegeNoch keine Bewertungen

- Chapter-2: Literature ReviewDokument3 SeitenChapter-2: Literature ReviewPushti DattaniNoch keine Bewertungen

- Assignment 3 Introduction To EconomicsDokument8 SeitenAssignment 3 Introduction To EconomicsLAIBA WAHABNoch keine Bewertungen

- Journal Ijarems Published March 2013Dokument13 SeitenJournal Ijarems Published March 2013api-248461761Noch keine Bewertungen

- ENTREPRENEURSHIP - FinalsDokument8 SeitenENTREPRENEURSHIP - FinalsPolNoch keine Bewertungen

- Topper Rushikesh Reddy Upsc Prelims Quick Revision Material Clearias PDFDokument272 SeitenTopper Rushikesh Reddy Upsc Prelims Quick Revision Material Clearias PDFAnkitha KavyaNoch keine Bewertungen

- Stress Testing of Non Performing Assets in Priority Sector LendingDokument11 SeitenStress Testing of Non Performing Assets in Priority Sector Lendingmakvar7465Noch keine Bewertungen

- COMM 223 Team ProjectDokument14 SeitenCOMM 223 Team ProjectAna100% (2)

- Fountain International School Economics 4Th Quarterly ExamDokument5 SeitenFountain International School Economics 4Th Quarterly ExamMaika ElaNoch keine Bewertungen

- Bird y Slack (2002)Dokument48 SeitenBird y Slack (2002)paulamszNoch keine Bewertungen

- Listed Investment BanksDokument3 SeitenListed Investment BanksYasir Aftab BachaniNoch keine Bewertungen

- TRL163Dokument25 SeitenTRL163Anil MarsaniNoch keine Bewertungen

- Centino Castano 2019Dokument21 SeitenCentino Castano 2019Ngân NgânNoch keine Bewertungen

- EMIS Insights - India Insurance Sector Report 2020 - 2024Dokument79 SeitenEMIS Insights - India Insurance Sector Report 2020 - 2024Kathiravan Rajendran100% (1)

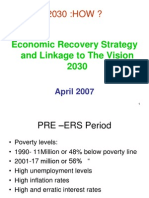

- ERS and Vision 2030 - April 2008Dokument64 SeitenERS and Vision 2030 - April 2008Elijah NyangwaraNoch keine Bewertungen

- SET5Dokument3 SeitenSET5SANDEEP GAMING ALLNoch keine Bewertungen