Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Allergen Guide NandosDokument6 SeitenAllergen Guide NandosShaka ZuluNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- TahoDokument43 SeitenTahoVj Delatado76% (17)

- Microbiological Quality Control of Soymilk Sold in Kogi StateDokument5 SeitenMicrobiological Quality Control of Soymilk Sold in Kogi StateIJAR JOURNALNoch keine Bewertungen

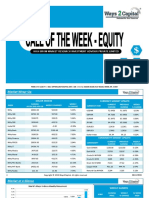

- Commodity Research Report 06 March 2019 Ways2CapitalDokument13 SeitenCommodity Research Report 06 March 2019 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 21 January 2019 Ways2CapitalDokument13 SeitenCommodity Research Report 21 January 2019 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 12 March 2019 Ways2CapitalDokument13 SeitenCommodity Research Report 12 March 2019 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Equity Research Report 27 November 2018 Ways2CapitalDokument17 SeitenEquity Research Report 27 November 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 03 December 2018 Ways2CapitalDokument13 SeitenCommodity Research Report 03 December 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 18 December 2018 Ways2CapitalDokument13 SeitenCommodity Research Report 18 December 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 11 December 2018 Ways2CapitalDokument13 SeitenCommodity Research Report 11 December 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Equity Research Report 06 November 2018 Ways2CapitalDokument17 SeitenEquity Research Report 06 November 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 27november 2018 Ways2CapitalDokument13 SeitenCommodity Research Report 27november 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Equity Research Report 13 November 2018 Ways2CapitalDokument17 SeitenEquity Research Report 13 November 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 16 October 2018 Ways2CapitalDokument13 SeitenCommodity Research Report 16 October 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 20 November 2018 Ways2CapitalDokument13 SeitenCommodity Research Report 20 November 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 23 October 2018 Ways2CapitalDokument13 SeitenCommodity Research Report 23 October 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 09 October 2018 Ways2CapitalDokument13 SeitenCommodity Research Report 09 October 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 12 September 2018 Ways2CapitalDokument13 SeitenCommodity Research Report 12 September 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 18 September 2018 Ways2CapitalDokument13 SeitenCommodity Research Report 18 September 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 04 September 2018 Ways2CapitalDokument13 SeitenCommodity Research Report 04 September 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 25 September 2018 Ways2CapitalDokument13 SeitenCommodity Research Report 25 September 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Commodity Research Report 21 August 2018 Ways2CapitalDokument13 SeitenCommodity Research Report 21 August 2018 Ways2CapitalWays2CapitalNoch keine Bewertungen

- Pregnancy BrochureDokument2 SeitenPregnancy Brochureapi-253611488Noch keine Bewertungen

- CowpeaDokument71 SeitenCowpeaAngela RedNoch keine Bewertungen

- FEDNA 2017 NR Pedersen - Actividad Enzimática Por Microscopía PDFDokument33 SeitenFEDNA 2017 NR Pedersen - Actividad Enzimática Por Microscopía PDFNinfa PedersenNoch keine Bewertungen

- Duckweed: A Sustainable Protein Supplement For The FutureDokument6 SeitenDuckweed: A Sustainable Protein Supplement For The FutureInternational Aquafeed magazine100% (1)

- The Road To Good NutritionDokument221 SeitenThe Road To Good NutritionSenyum SehatNoch keine Bewertungen

- Project Topics and Materials in Food Science and TechnologyDokument44 SeitenProject Topics and Materials in Food Science and TechnologyGrace OparaNoch keine Bewertungen

- Aquatic Plant Extracts-2004!02!14Dokument18 SeitenAquatic Plant Extracts-2004!02!14pedro41Noch keine Bewertungen

- Raise Organic HogsDokument103 SeitenRaise Organic HogsVimarce Culi100% (1)

- Technology FoodDokument5 SeitenTechnology FoodBarnali DuttaNoch keine Bewertungen

- Guyiti Tengi FULL PROJECT FinalDokument51 SeitenGuyiti Tengi FULL PROJECT FinalJemalNoch keine Bewertungen

- Uganda PDFDokument114 SeitenUganda PDFMadhu KumarNoch keine Bewertungen

- Manufacturing Compounded Feeds in Developing CountriesDokument33 SeitenManufacturing Compounded Feeds in Developing CountriesjoynulNoch keine Bewertungen

- 934072institutional Presentation CRESUD IIIQ22Dokument20 Seiten934072institutional Presentation CRESUD IIIQ22JohanyCaroNoch keine Bewertungen

- Radhwa International SchoolDokument45 SeitenRadhwa International Schoolsafamanz001 safaNoch keine Bewertungen

- Poultry Nutrition and FeedingDokument16 SeitenPoultry Nutrition and FeedingYaserAbbasiNoch keine Bewertungen

- Kirkman DigestiveEnzymesGuideDokument40 SeitenKirkman DigestiveEnzymesGuideeptanNoch keine Bewertungen

- Spring Farm and FieldDokument64 SeitenSpring Farm and FieldJason LewtonNoch keine Bewertungen

- Coconut FermentationDokument9 SeitenCoconut FermentationPedro Peláez Sánchez100% (1)

- Tables Composition Nutritional Values Organically Feed Materials Pigs PoultryDokument39 SeitenTables Composition Nutritional Values Organically Feed Materials Pigs PoultryJ Jesus Bustamante Gro100% (1)

- 2-Jrefarticle 1Dokument17 Seiten2-Jrefarticle 1manibhargaviNoch keine Bewertungen

- Fertilizer Industry OverviewDokument33 SeitenFertilizer Industry Overviewapi-199688590% (1)

- Nutrition Guidelines For Stomach HeatDokument21 SeitenNutrition Guidelines For Stomach Heatmarcia yadavNoch keine Bewertungen

- Arbonne Essentials Protein Shake MixDokument2 SeitenArbonne Essentials Protein Shake Mixapi-240485683Noch keine Bewertungen

- Preparation of Soya Bean Milk and Its Comparison With Natural Milk With Respect To Curd Formation, Effect of Temperature.Dokument15 SeitenPreparation of Soya Bean Milk and Its Comparison With Natural Milk With Respect To Curd Formation, Effect of Temperature.Mayank Singh100% (1)

- Rishab Garg Major ProjrctDokument10 SeitenRishab Garg Major ProjrctHIMANSHU RAWATNoch keine Bewertungen

- WASDE Jan 2008Dokument40 SeitenWASDE Jan 2008kcolombiniNoch keine Bewertungen

- 2006 Vegetarian Diets - Nutritional Considerations For AthletesDokument14 Seiten2006 Vegetarian Diets - Nutritional Considerations For AthletesAni Fran SolarNoch keine Bewertungen