Das könnte Ihnen auch gefallen

- Nathan Lyttle: ExperienceDokument1 SeiteNathan Lyttle: ExperienceNathan LyttleNoch keine Bewertungen

- Macquarie Fact SheetDokument2 SeitenMacquarie Fact SheetNathan LyttleNoch keine Bewertungen

- 2017 City of Whitesburg ExaminationDokument80 Seiten2017 City of Whitesburg ExaminationNathan LyttleNoch keine Bewertungen

- Judge Wingate's Order Involving KHSAA and Perry Central PlayersDokument8 SeitenJudge Wingate's Order Involving KHSAA and Perry Central PlayersNathan LyttleNoch keine Bewertungen

- KRCC Homeless Shelter Open LetterDokument1 SeiteKRCC Homeless Shelter Open LetterNathan LyttleNoch keine Bewertungen

- Eric C. Conn News ReleaseDokument2 SeitenEric C. Conn News ReleaseNathan LyttleNoch keine Bewertungen

- TestDokument3 SeitenTestNathan LyttleNoch keine Bewertungen

- 2017 Church SurveyDokument30 Seiten2017 Church SurveyNathan LyttleNoch keine Bewertungen

- KHSAA StatsDokument6 SeitenKHSAA StatsNathan LyttleNoch keine Bewertungen

- FNU News ReleaseDokument2 SeitenFNU News ReleaseNathan LyttleNoch keine Bewertungen

- McKesson Record $150M SettlementDokument2 SeitenMcKesson Record $150M SettlementNathan LyttleNoch keine Bewertungen

- Jerry Fannin IndictmentDokument5 SeitenJerry Fannin IndictmentNathan LyttleNoch keine Bewertungen

- Media Statement - April 21, 2016Dokument1 SeiteMedia Statement - April 21, 2016Nathan LyttleNoch keine Bewertungen

- EKY WORKS Rollout PresentationDokument51 SeitenEKY WORKS Rollout PresentationNathan LyttleNoch keine Bewertungen

- Gibson IndictmentDokument4 SeitenGibson IndictmentNathan LyttleNoch keine Bewertungen

- Owsley AuditDokument5 SeitenOwsley AuditNathan LyttleNoch keine Bewertungen

- Stewart/Morris IndictmentDokument4 SeitenStewart/Morris IndictmentNathan LyttleNoch keine Bewertungen

- 2016 NCAA Tourney BracketDokument1 Seite2016 NCAA Tourney BracketNathan LyttleNoch keine Bewertungen

- GRAPHIC: Willard Hall AffidavitDokument21 SeitenGRAPHIC: Willard Hall AffidavitNathan Lyttle100% (2)

- Beshear Bevin SuitDokument202 SeitenBeshear Bevin SuitNathan LyttleNoch keine Bewertungen

- Executive Order 2016-270 Reorganizing Boxing and Wrestling CommissionDokument7 SeitenExecutive Order 2016-270 Reorganizing Boxing and Wrestling CommissionNathan LyttleNoch keine Bewertungen

- Conn HearingDokument1 SeiteConn HearingNathan LyttleNoch keine Bewertungen

- Jason GibsonDokument4 SeitenJason GibsonNathan LyttleNoch keine Bewertungen

- Wrestlemania ScorecardDokument1 SeiteWrestlemania ScorecardNathan LyttleNoch keine Bewertungen

- Adoption GuideDokument16 SeitenAdoption GuideGustavo PalaciosNoch keine Bewertungen

- UK Stony Brook Box ScoreDokument1 SeiteUK Stony Brook Box ScoreNathan LyttleNoch keine Bewertungen

- IndictmentDokument5 SeitenIndictmentNathan LyttleNoch keine Bewertungen

- ReleaseDokument1 SeiteReleaseNathan LyttleNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- AuditingDokument20 SeitenAuditingAmey ManchekarNoch keine Bewertungen

- Temecula Quality Plating AS9100 REV C MANUALDokument13 SeitenTemecula Quality Plating AS9100 REV C MANUALHoang TanNoch keine Bewertungen

- Online ShoppingDokument54 SeitenOnline ShoppingVaryam Pandey50% (6)

- Kerala Abkari Workers' Welfare Fund ActDokument19 SeitenKerala Abkari Workers' Welfare Fund Actneet1Noch keine Bewertungen

- Manual Operations & Emergency Procedures Guide: October 2015Dokument20 SeitenManual Operations & Emergency Procedures Guide: October 2015Ronald RonaldNoch keine Bewertungen

- Comaprison LatestDokument30 SeitenComaprison Latestbunnyplays823Noch keine Bewertungen

- SOX 404 & IT Controls: IT Control Recommendations For Small and Mid-Size Companies byDokument21 SeitenSOX 404 & IT Controls: IT Control Recommendations For Small and Mid-Size Companies byDeepthi Suresh100% (1)

- AuditeurDokument2 SeitenAuditeurMed Khalil FarhatNoch keine Bewertungen

- AGM Minutes Dec 2014Dokument4 SeitenAGM Minutes Dec 2014kradNoch keine Bewertungen

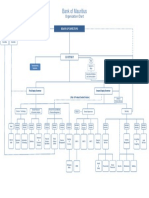

- Organisation Structure Bank of MauritiusDokument1 SeiteOrganisation Structure Bank of MauritiuscvikasguptaNoch keine Bewertungen

- ISO PrinciplesDokument4 SeitenISO PrincipleshasibNoch keine Bewertungen

- Case 4.4 Waste ManagementDokument6 SeitenCase 4.4 Waste ManagementNurul SyahirahNoch keine Bewertungen

- HSBC CaseDokument9 SeitenHSBC Casemanea ba fakihNoch keine Bewertungen

- Supplier Quality & Food Safety Audit: Your LogoDokument6 SeitenSupplier Quality & Food Safety Audit: Your LogokarupukamalNoch keine Bewertungen

- 72 CL 001.7 17021-1 2015 e 20151123 v1.6Dokument34 Seiten72 CL 001.7 17021-1 2015 e 20151123 v1.6Ferdous Khan RubelNoch keine Bewertungen

- Maastricht School of Management 2014-11-11Dokument47 SeitenMaastricht School of Management 2014-11-11agusNoch keine Bewertungen

- Ethiopia's Accounting and Auditing Standards and PracticesDokument24 SeitenEthiopia's Accounting and Auditing Standards and PracticesKenn Mwangii100% (2)

- Insider Loan FraudDokument42 SeitenInsider Loan FraudCarrieonicNoch keine Bewertungen

- Three Arrows Capital Singapore ReturnDokument46 SeitenThree Arrows Capital Singapore ReturnSam ReynoldsNoch keine Bewertungen

- CASE DIGEST Labor Case BTCH 2 1-15Dokument39 SeitenCASE DIGEST Labor Case BTCH 2 1-15twenty19 lawNoch keine Bewertungen

- Gbermic Internal Control CabreraDokument5 SeitenGbermic Internal Control CabreraÌÐølJåyskëiUvNoch keine Bewertungen

- Audit Checklist in Production AreaDokument5 SeitenAudit Checklist in Production AreaPrince Moni100% (2)

- Government Staffing and Capacity SurveyDokument6 SeitenGovernment Staffing and Capacity SurveydennisNoch keine Bewertungen

- Audit Plan: Wasi Steel Industries Factory CoDokument4 SeitenAudit Plan: Wasi Steel Industries Factory CoMuhammad IrfanNoch keine Bewertungen

- Universal Standards On Social Performance ManagementDokument21 SeitenUniversal Standards On Social Performance ManagementTherese MarieNoch keine Bewertungen

- Tier 1 Firms - Overview: Audit Quality Inspection and Supervision ReportDokument37 SeitenTier 1 Firms - Overview: Audit Quality Inspection and Supervision ReportAbdelmadjid djibrineNoch keine Bewertungen

- Risk Maturity Determines Framework CompletenessDokument186 SeitenRisk Maturity Determines Framework CompletenessNagendra KrishnamurthyNoch keine Bewertungen

- Risk-Based IA Planning - Important ConsiderationsDokument14 SeitenRisk-Based IA Planning - Important ConsiderationsRajitha LakmalNoch keine Bewertungen

- Contractor Registration Board of TanzaniDokument92 SeitenContractor Registration Board of TanzaniChristian Nicolaus MbiseNoch keine Bewertungen

- G - Cash Examination Report Template MDJ 110713Dokument4 SeitenG - Cash Examination Report Template MDJ 110713Hoven Macasinag100% (3)