Das könnte Ihnen auch gefallen

- Berjaya Sports Toto Berhad: BCorp Aborts Sports Betting Deal - 28/06/2010Dokument2 SeitenBerjaya Sports Toto Berhad: BCorp Aborts Sports Betting Deal - 28/06/2010Rhb InvestNoch keine Bewertungen

- Berjaya Sports Toto Berhad : Struck by Pool Betting Duty Hike - 02/07/2010Dokument3 SeitenBerjaya Sports Toto Berhad : Struck by Pool Betting Duty Hike - 02/07/2010Rhb InvestNoch keine Bewertungen

- Kinsteel Berhad: Better Demand Ahead - 10/03/2010Dokument3 SeitenKinsteel Berhad: Better Demand Ahead - 10/03/2010Rhb InvestNoch keine Bewertungen

- YTL Cement Berhad: Acquiring Remaining 35.16% Stake in Perak - Hanjoong Simen For RM200m - 27/09/2010Dokument2 SeitenYTL Cement Berhad: Acquiring Remaining 35.16% Stake in Perak - Hanjoong Simen For RM200m - 27/09/2010Rhb InvestNoch keine Bewertungen

- YTL Cement Berhad: 3QFY06/10 Performance Rises On One-Off Gains Anticipating Better 4Q - 31/5/2010Dokument3 SeitenYTL Cement Berhad: 3QFY06/10 Performance Rises On One-Off Gains Anticipating Better 4Q - 31/5/2010Rhb InvestNoch keine Bewertungen

- PLUS Expressways Berhad: Obtains Approval To Construct Fourth Lane For Certain Stretches of NSE & NKVE - 7/7/2010Dokument2 SeitenPLUS Expressways Berhad: Obtains Approval To Construct Fourth Lane For Certain Stretches of NSE & NKVE - 7/7/2010Rhb InvestNoch keine Bewertungen

- Berjaya Sports Toto BHD: of Sports Betting and More - 29/6/2010Dokument2 SeitenBerjaya Sports Toto BHD: of Sports Betting and More - 29/6/2010Rhb InvestNoch keine Bewertungen

- CSC Steel Berhad: 1QFY12/10 Net Profit Soars On Improved Margins Near-Term Outlook Remains Positive - 10/5/2010Dokument3 SeitenCSC Steel Berhad: 1QFY12/10 Net Profit Soars On Improved Margins Near-Term Outlook Remains Positive - 10/5/2010Rhb InvestNoch keine Bewertungen

- Malayan Banking Berhad: On Course For Strong Rebound in Earnings - 16/08/2010Dokument3 SeitenMalayan Banking Berhad: On Course For Strong Rebound in Earnings - 16/08/2010Rhb InvestNoch keine Bewertungen

- Top Glove Corporation Berhad: Proposes 1-For-1 Bonus Issue-27/04/2010Dokument2 SeitenTop Glove Corporation Berhad: Proposes 1-For-1 Bonus Issue-27/04/2010Rhb InvestNoch keine Bewertungen

- Ta Ann Holdings Berhad: Earnings Expected To Pick Up From 2QFY12/10 - 31/5/2010Dokument4 SeitenTa Ann Holdings Berhad: Earnings Expected To Pick Up From 2QFY12/10 - 31/5/2010Rhb InvestNoch keine Bewertungen

- Public Bank Berhad: Starting Off On Strong Footing - 16/04/2010Dokument5 SeitenPublic Bank Berhad: Starting Off On Strong Footing - 16/04/2010Rhb InvestNoch keine Bewertungen

- CSC Steel Berhad: 1HFY12/10 Performance Soars On Improved Margins - 10/08/2010Dokument3 SeitenCSC Steel Berhad: 1HFY12/10 Performance Soars On Improved Margins - 10/08/2010Rhb InvestNoch keine Bewertungen

- Kinsteel Berhad: 2QFY12/10 Net Profit Falls 64% On Higher Input Costs and Weaker Sales Volumes - 30/08/2010Dokument3 SeitenKinsteel Berhad: 2QFY12/10 Net Profit Falls 64% On Higher Input Costs and Weaker Sales Volumes - 30/08/2010Rhb InvestNoch keine Bewertungen

- AEON Co. (M) Berhad: Slower-Than-Expected SSS Growth in 1HFY12/10-10/08/2010Dokument4 SeitenAEON Co. (M) Berhad: Slower-Than-Expected SSS Growth in 1HFY12/10-10/08/2010Rhb InvestNoch keine Bewertungen

- Emas Kiara Industries Berhad: 1QFY12/10 Net Profit Grows 23% YoY - 31/5/2010Dokument7 SeitenEmas Kiara Industries Berhad: 1QFY12/10 Net Profit Grows 23% YoY - 31/5/2010Rhb InvestNoch keine Bewertungen

- Fajarbaru Builder Group Berhad: To Embark On A Greenfield Hotel Project in Melaka - 31/5/2010Dokument5 SeitenFajarbaru Builder Group Berhad: To Embark On A Greenfield Hotel Project in Melaka - 31/5/2010Rhb InvestNoch keine Bewertungen

- Petra Perdana Berhad: Proposes Private Placement and Renounceable Right - 12/5/2010Dokument3 SeitenPetra Perdana Berhad: Proposes Private Placement and Renounceable Right - 12/5/2010Rhb InvestNoch keine Bewertungen

- Genting Malaysia Berhad: Wins New York Racino Bid - 04/08/2010Dokument3 SeitenGenting Malaysia Berhad: Wins New York Racino Bid - 04/08/2010Rhb InvestNoch keine Bewertungen

- Freight Management: Disposes of Leasehold Land in Klang - 24/6/2010Dokument2 SeitenFreight Management: Disposes of Leasehold Land in Klang - 24/6/2010Rhb InvestNoch keine Bewertungen

- Tenaga Nasional Berhad: A Decent 4QFY10 Expected - 15/10/2010Dokument3 SeitenTenaga Nasional Berhad: A Decent 4QFY10 Expected - 15/10/2010Rhb InvestNoch keine Bewertungen

- Lafarge (M) Cement Berhad :FY12/09 Performance Boosted by Margin Expansion - 01/03/2010Dokument3 SeitenLafarge (M) Cement Berhad :FY12/09 Performance Boosted by Margin Expansion - 01/03/2010Rhb InvestNoch keine Bewertungen

- IJM Land Berhad: Disposes of Aeon Bandaraya Melaka - 25/6/2010Dokument3 SeitenIJM Land Berhad: Disposes of Aeon Bandaraya Melaka - 25/6/2010Rhb InvestNoch keine Bewertungen

- Hong Leong Bank Berhad: Stronger Net Profit, But Mainly Due To Low Tax Rate - 25/05/2010Dokument5 SeitenHong Leong Bank Berhad: Stronger Net Profit, But Mainly Due To Low Tax Rate - 25/05/2010Rhb InvestNoch keine Bewertungen

- M'sian Resources Corp Berhad: Construction and Property Development Activities Gather Momentum in 1QFY12/10 - 19/5/2010Dokument4 SeitenM'sian Resources Corp Berhad: Construction and Property Development Activities Gather Momentum in 1QFY12/10 - 19/5/2010Rhb InvestNoch keine Bewertungen

- Freight Management Berhad: 1HFY06/10 Net Profit Rises 20% YoY - 01/03/2010Dokument3 SeitenFreight Management Berhad: 1HFY06/10 Net Profit Rises 20% YoY - 01/03/2010Rhb InvestNoch keine Bewertungen

- Fajarbaru Builder Group Berhad: Eyeing RM400m PFI Teaching-Hospital in Kuantan - 12/03/2010Dokument4 SeitenFajarbaru Builder Group Berhad: Eyeing RM400m PFI Teaching-Hospital in Kuantan - 12/03/2010Rhb InvestNoch keine Bewertungen

- RCE Capital Berhad: Strong Start To The Year - 16/08/2010Dokument3 SeitenRCE Capital Berhad: Strong Start To The Year - 16/08/2010Rhb InvestNoch keine Bewertungen

- IJM Plantations Berhad: Buys More Land in Indonesia - 04/08/2010Dokument2 SeitenIJM Plantations Berhad: Buys More Land in Indonesia - 04/08/2010Rhb InvestNoch keine Bewertungen

- Hiap Teck Venture Berhad :2QFY07/10 Net Profit Dips QoQ - 31/03/2010Dokument3 SeitenHiap Teck Venture Berhad :2QFY07/10 Net Profit Dips QoQ - 31/03/2010Rhb InvestNoch keine Bewertungen

- Mah Sing Group Berhad :getting Stronger-27/08/2010Dokument4 SeitenMah Sing Group Berhad :getting Stronger-27/08/2010Rhb InvestNoch keine Bewertungen

- Tenaga Nasional Berhad: 3QFY10 Results Dampened by Higher Coal Cost and Provisions - 15/7/2010Dokument6 SeitenTenaga Nasional Berhad: 3QFY10 Results Dampened by Higher Coal Cost and Provisions - 15/7/2010Rhb InvestNoch keine Bewertungen

- Capitamalls Malaysia Trust: New ListingDokument7 SeitenCapitamalls Malaysia Trust: New ListingRhb InvestNoch keine Bewertungen

- Misc Berhad: FY03/10 A Washout - 7/5/2010Dokument3 SeitenMisc Berhad: FY03/10 A Washout - 7/5/2010Rhb InvestNoch keine Bewertungen

- Tenaga Nasional Berhad: Demand Growth Turning Out Stronger Than Expected - 21/04/2010Dokument5 SeitenTenaga Nasional Berhad: Demand Growth Turning Out Stronger Than Expected - 21/04/2010Rhb InvestNoch keine Bewertungen

- Mah Sing Group Berhad: To Take Over A Mahajaya's Project in Kinrara - 6/7/2010Dokument3 SeitenMah Sing Group Berhad: To Take Over A Mahajaya's Project in Kinrara - 6/7/2010Rhb InvestNoch keine Bewertungen

- Emas Kiara Industries Berhad: Decent FY12/09 Performance Despite Economic Uncertainty - 01/03/2010Dokument7 SeitenEmas Kiara Industries Berhad: Decent FY12/09 Performance Despite Economic Uncertainty - 01/03/2010Rhb InvestNoch keine Bewertungen

- JAKS Resources Berhad: Powering Up-14/04/2010Dokument9 SeitenJAKS Resources Berhad: Powering Up-14/04/2010Rhb InvestNoch keine Bewertungen

- KPJ Healthcare Berhad: On Track To Meet Its 2012 Target - 01/03/2010Dokument3 SeitenKPJ Healthcare Berhad: On Track To Meet Its 2012 Target - 01/03/2010Rhb InvestNoch keine Bewertungen

- Axiata Berhad: Likely To Report Strong 1Q10 Performance - 21/5/2010Dokument3 SeitenAxiata Berhad: Likely To Report Strong 1Q10 Performance - 21/5/2010Rhb InvestNoch keine Bewertungen

- Malayan Banking Berhad: Dishing Out Dividends - 23/08/2010Dokument7 SeitenMalayan Banking Berhad: Dishing Out Dividends - 23/08/2010Rhb InvestNoch keine Bewertungen

- KPJ Healthcare Berhad: Injecting Another Three Hospitals Into KPJ REIT - 10/03/2010Dokument2 SeitenKPJ Healthcare Berhad: Injecting Another Three Hospitals Into KPJ REIT - 10/03/2010Rhb InvestNoch keine Bewertungen

- Fajarbaru Builder Group Berhad: FY06/10 Results To Beat Our Expectation - 04/08/2010Dokument3 SeitenFajarbaru Builder Group Berhad: FY06/10 Results To Beat Our Expectation - 04/08/2010Rhb InvestNoch keine Bewertungen

- Tanjong PLC :awaiting The Next Rerating Catalyst - 13/04/2010Dokument5 SeitenTanjong PLC :awaiting The Next Rerating Catalyst - 13/04/2010Rhb InvestNoch keine Bewertungen

- Puncak Niaga Holdings Berhad: FY12/09 Net Profit Underpinned by GovernmentCompensation Yet To Be Received - 01/03/2010Dokument3 SeitenPuncak Niaga Holdings Berhad: FY12/09 Net Profit Underpinned by GovernmentCompensation Yet To Be Received - 01/03/2010Rhb InvestNoch keine Bewertungen

- EON Capital Berhad: Starting Off On A Strong Note - 24/05/2010Dokument6 SeitenEON Capital Berhad: Starting Off On A Strong Note - 24/05/2010Rhb InvestNoch keine Bewertungen

- CSC Steel Berhad: 1QFY12/10 Results To Beat Expectations - 30/04/2010Dokument2 SeitenCSC Steel Berhad: 1QFY12/10 Results To Beat Expectations - 30/04/2010Rhb InvestNoch keine Bewertungen

- MISC Berhad: 1QFY03/11 Net Profit Jumps 83% YoY On Reduced Container Liner Losses - 20/08/2010Dokument3 SeitenMISC Berhad: 1QFY03/11 Net Profit Jumps 83% YoY On Reduced Container Liner Losses - 20/08/2010Rhb InvestNoch keine Bewertungen

- Lafarge (M) Cement Berhad: 1Q FY12/10 Performance Declines 47% On Weak - 27/05/2010Dokument3 SeitenLafarge (M) Cement Berhad: 1Q FY12/10 Performance Declines 47% On Weak - 27/05/2010Rhb InvestNoch keine Bewertungen

- Dialog Group Berhad: Secured E&C Contract Worth SG$21.3mDokument3 SeitenDialog Group Berhad: Secured E&C Contract Worth SG$21.3mRhb InvestNoch keine Bewertungen

- Hai-O Enterprise Berhad: FY04/11 Membership To Contract - 29/07/2010Dokument5 SeitenHai-O Enterprise Berhad: FY04/11 Membership To Contract - 29/07/2010Rhb InvestNoch keine Bewertungen

- IJM Land Berhad: On Track - 01/03/2010Dokument4 SeitenIJM Land Berhad: On Track - 01/03/2010Rhb InvestNoch keine Bewertungen

- EON Capital Berhad: Shareholders Approve HL Bank's Offer - 28/09/2010Dokument3 SeitenEON Capital Berhad: Shareholders Approve HL Bank's Offer - 28/09/2010Rhb InvestNoch keine Bewertungen

- Hock Seng Lee - Secures A RM72.5m Road Job in Sarawak - 10/6/2010Dokument2 SeitenHock Seng Lee - Secures A RM72.5m Road Job in Sarawak - 10/6/2010Rhb InvestNoch keine Bewertungen

- Sunway City Berhad: Aggressive Launches of New Properties - 01/09/2010Dokument6 SeitenSunway City Berhad: Aggressive Launches of New Properties - 01/09/2010Rhb InvestNoch keine Bewertungen

- Banking: More Licences, But Competition Should Not Deter Growth - 31/03/2010Dokument7 SeitenBanking: More Licences, But Competition Should Not Deter Growth - 31/03/2010Rhb InvestNoch keine Bewertungen

- Hock Seng Lee Berhad: Poised To Top RM500m Orderbook Target in FY12/10 - 19/5/2010Dokument4 SeitenHock Seng Lee Berhad: Poised To Top RM500m Orderbook Target in FY12/10 - 19/5/2010Rhb InvestNoch keine Bewertungen

- KNM Group Berhad: Still Weak - 01/09/2010Dokument3 SeitenKNM Group Berhad: Still Weak - 01/09/2010Rhb InvestNoch keine Bewertungen

- Kencana Petroleum Berhad: Going Into IPF-20/04/2010Dokument5 SeitenKencana Petroleum Berhad: Going Into IPF-20/04/2010Rhb InvestNoch keine Bewertungen

- RHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Dokument4 SeitenRHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Rhb InvestNoch keine Bewertungen

- WCT Berhad: Secures RM1.36bn Building Job in Qatar and RM128m Hospital Project in Sabah - 21/10/2010Dokument3 SeitenWCT Berhad: Secures RM1.36bn Building Job in Qatar and RM128m Hospital Project in Sabah - 21/10/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights - Inflation Unexpectedly Eased in September - 25/10/2010Dokument3 SeitenEconomic Highlights - Inflation Unexpectedly Eased in September - 25/10/2010Rhb InvestNoch keine Bewertungen

- Commodities & Currencies - Yet Another Sign of A Rebound On The Greenback - 25/10/2010Dokument3 SeitenCommodities & Currencies - Yet Another Sign of A Rebound On The Greenback - 25/10/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights - Foreign Exchange Reserves Rose To US$104.6bn As at 15 October - 25/10/2010Dokument2 SeitenEconomic Highlights - Foreign Exchange Reserves Rose To US$104.6bn As at 15 October - 25/10/2010Rhb InvestNoch keine Bewertungen

- Puncak Niaga Berhad: Eyeing Hogenakkal Water Project in India - 21/10/2010Dokument2 SeitenPuncak Niaga Berhad: Eyeing Hogenakkal Water Project in India - 21/10/2010Rhb InvestNoch keine Bewertungen

- Rubber Glove Sector Update: Still Cautious On Near-Term Outlook - 21/10/2010Dokument2 SeitenRubber Glove Sector Update: Still Cautious On Near-Term Outlook - 21/10/2010Rhb InvestNoch keine Bewertungen

- RHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Dokument4 SeitenRHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Rhb InvestNoch keine Bewertungen

- Corporate Highlights - 22/10/2010Dokument2 SeitenCorporate Highlights - 22/10/2010Rhb InvestNoch keine Bewertungen

- RHB Equity 360° - 21 October 2010 (Media, Rubber Gloves, Puncak Niaga, WCT, Axis REIT, BAT Technical: AFG)Dokument4 SeitenRHB Equity 360° - 21 October 2010 (Media, Rubber Gloves, Puncak Niaga, WCT, Axis REIT, BAT Technical: AFG)Rhb InvestNoch keine Bewertungen

- Motor Sector Update - Lower TIV On Shorter Working Month - 20/10/2010Dokument6 SeitenMotor Sector Update - Lower TIV On Shorter Working Month - 20/10/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights - Decline in Manufacturing Investment Approvals Narrowed in The 2Q - 20/10/2010Dokument3 SeitenEconomic Highlights - Decline in Manufacturing Investment Approvals Narrowed in The 2Q - 20/10/2010Rhb InvestNoch keine Bewertungen

- Corporate Highlights - 21/10/2010Dokument2 SeitenCorporate Highlights - 21/10/2010Rhb InvestNoch keine Bewertungen

- British American Tobacco: Corporate HighlightsDokument4 SeitenBritish American Tobacco: Corporate HighlightsRhb InvestNoch keine Bewertungen

- RHB Equity 360° - 20 October 2010 (Property, Motor, Quill Capita Technical: Kump. Hartanah Selangor)Dokument3 SeitenRHB Equity 360° - 20 October 2010 (Property, Motor, Quill Capita Technical: Kump. Hartanah Selangor)Rhb InvestNoch keine Bewertungen

- Economic Highlights - Leading Index Bounced Back in August, Pointing To A Resilient Economic Activities Ahead - 20/10/2010Dokument2 SeitenEconomic Highlights - Leading Index Bounced Back in August, Pointing To A Resilient Economic Activities Ahead - 20/10/2010Rhb InvestNoch keine Bewertungen

- Axis REIT: Quattro West Started To Contribute - 21/10/2010Dokument3 SeitenAxis REIT: Quattro West Started To Contribute - 21/10/2010Rhb InvestNoch keine Bewertungen

- Quill Capita Trust: Flattish 3Q10 Numbers - 20/10/2010Dokument3 SeitenQuill Capita Trust: Flattish 3Q10 Numbers - 20/10/2010Rhb InvestNoch keine Bewertungen

- Tracking The World Economy... - 19/10/2010Dokument3 SeitenTracking The World Economy... - 19/10/2010Rhb InvestNoch keine Bewertungen

- Corporate Highlights - 20/10/2010Dokument2 SeitenCorporate Highlights - 20/10/2010Rhb InvestNoch keine Bewertungen

- RHB Equity 360° - 19 October 2010 (ILB, Public Bank Technical: Ann Joo)Dokument3 SeitenRHB Equity 360° - 19 October 2010 (ILB, Public Bank Technical: Ann Joo)Rhb InvestNoch keine Bewertungen

- Corporate Highlights - 19/10/2010Dokument2 SeitenCorporate Highlights - 19/10/2010Rhb InvestNoch keine Bewertungen

- RHB Equity 360° - 18 October 2010 (Budget, PLUS Technical: Axiata, CMS)Dokument3 SeitenRHB Equity 360° - 18 October 2010 (Budget, PLUS Technical: Axiata, CMS)Rhb InvestNoch keine Bewertungen

- Tracking The World Economy... - 18/10/2010Dokument2 SeitenTracking The World Economy... - 18/10/2010Rhb InvestNoch keine Bewertungen

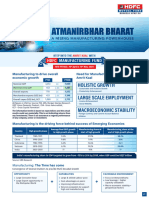

- NFO Leaflet - HDFC Manufacturing Fund - 240422 - 142358Dokument2 SeitenNFO Leaflet - HDFC Manufacturing Fund - 240422 - 142358bitsthechampNoch keine Bewertungen

- Use The Following Information To Answer Items 1 To 3:: FARQ 218 Page 1 of 3Dokument3 SeitenUse The Following Information To Answer Items 1 To 3:: FARQ 218 Page 1 of 3Irvin LevieNoch keine Bewertungen

- Financial Management Midterm ExamDokument4 SeitenFinancial Management Midterm ExamJoody CatacutanNoch keine Bewertungen

- ReplacedDokument4 SeitenReplacedLuno coin100% (1)

- Variable Costing & Segment Reporting-FINALDokument29 SeitenVariable Costing & Segment Reporting-FINALTin Bernadette DominicoNoch keine Bewertungen

- Entrepreneurship Successfully Launching New Ventures 5th Edition Ebook PDFDokument41 SeitenEntrepreneurship Successfully Launching New Ventures 5th Edition Ebook PDFsilvia.duran185Noch keine Bewertungen

- Share Based Payments - Problems: Problem 1Dokument79 SeitenShare Based Payments - Problems: Problem 1tan dinhNoch keine Bewertungen

- Deal StructuringDokument2 SeitenDeal StructuringFreemind HunkNoch keine Bewertungen

- Cfas - Reviewer PDFDokument21 SeitenCfas - Reviewer PDFMira Monica D. VillacastinNoch keine Bewertungen

- Theory of Finance NotesDokument36 SeitenTheory of Finance Notesroberto piccinottiNoch keine Bewertungen

- FM-1 Course Handout 2021-22Dokument4 SeitenFM-1 Course Handout 2021-22Apoorva PattnaikNoch keine Bewertungen

- Financially Yours: Session-IIDokument36 SeitenFinancially Yours: Session-IIRaviSinghNoch keine Bewertungen

- Financial Reporting and Analysis 13th Edition Gibson Solutions Manual 1Dokument20 SeitenFinancial Reporting and Analysis 13th Edition Gibson Solutions Manual 1james100% (41)

- Dividends and Other PayoutsDokument29 SeitenDividends and Other PayoutsArif AlamgirNoch keine Bewertungen

- Bharti Airtel Ltd. (India) : SourceDokument6 SeitenBharti Airtel Ltd. (India) : SourceDivyagarapatiNoch keine Bewertungen

- South-Western Federal Taxation 2017 Corporations Partnerships Estates and Trusts 40th Edition Hoffman Test Bank 1Dokument41 SeitenSouth-Western Federal Taxation 2017 Corporations Partnerships Estates and Trusts 40th Edition Hoffman Test Bank 1donna100% (40)

- ACP 312 Week 6-7Dokument62 SeitenACP 312 Week 6-7Chara etang100% (1)

- Marketing Metrics: Ts. Lê Thùy Hương Khoa MarketingDokument23 SeitenMarketing Metrics: Ts. Lê Thùy Hương Khoa MarketingDuy TrầnNoch keine Bewertungen

- Corporate Finance ManualDokument135 SeitenCorporate Finance Manualsanu sayedNoch keine Bewertungen

- 2012 Final Exam SolutionDokument14 Seiten2012 Final Exam SolutionOmar Ahmed ElkhalilNoch keine Bewertungen

- L 2 Ss 5 Los 16Dokument5 SeitenL 2 Ss 5 Los 16Edgar LayNoch keine Bewertungen

- This Study Resource Was: Process Costing - AverageDokument7 SeitenThis Study Resource Was: Process Costing - AverageIllion IllionNoch keine Bewertungen

- IA Chapter-1-3Dokument7 SeitenIA Chapter-1-3Christine Joyce EnriquezNoch keine Bewertungen

- Financial Modelling Internal-1 Britannia IndustriesDokument4 SeitenFinancial Modelling Internal-1 Britannia IndustriesanushaNoch keine Bewertungen

- CH 5-6 AccDokument25 SeitenCH 5-6 AccKaashifNoch keine Bewertungen

- Chapter 9 Financial Forecasting For Strategic GrowthDokument18 SeitenChapter 9 Financial Forecasting For Strategic GrowthMa. Jhoan DailyNoch keine Bewertungen

- Chapter 10 and 12 GitmanDokument32 SeitenChapter 10 and 12 GitmanLBL_LowkeeNoch keine Bewertungen

- Private Equity Valuation - BrochureDokument5 SeitenPrivate Equity Valuation - BrochureJustine9910% (1)

- 3.4.accounting For Income TaxesDokument65 Seiten3.4.accounting For Income TaxesPranjal pandeyNoch keine Bewertungen

- Audit Entry Sheet 2Dokument43 SeitenAudit Entry Sheet 2Charles MarkeyNoch keine Bewertungen

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamVon EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNoch keine Bewertungen

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialVon EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNoch keine Bewertungen

- The Value of a Whale: On the Illusions of Green CapitalismVon EverandThe Value of a Whale: On the Illusions of Green CapitalismBewertung: 5 von 5 Sternen5/5 (2)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaVon EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaBewertung: 3.5 von 5 Sternen3.5/5 (8)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthVon EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthBewertung: 4 von 5 Sternen4/5 (20)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNVon Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNBewertung: 4.5 von 5 Sternen4.5/5 (3)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaVon EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaBewertung: 4.5 von 5 Sternen4.5/5 (14)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successVon EverandReady, Set, Growth hack:: A beginners guide to growth hacking successBewertung: 4.5 von 5 Sternen4.5/5 (93)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialVon EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialBewertung: 4.5 von 5 Sternen4.5/5 (32)

- Creating Shareholder Value: A Guide For Managers And InvestorsVon EverandCreating Shareholder Value: A Guide For Managers And InvestorsBewertung: 4.5 von 5 Sternen4.5/5 (8)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyVon EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyBewertung: 3 von 5 Sternen3/5 (1)

- Corporate Finance Formulas: A Simple IntroductionVon EverandCorporate Finance Formulas: A Simple IntroductionBewertung: 4 von 5 Sternen4/5 (8)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingVon EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingBewertung: 4.5 von 5 Sternen4.5/5 (17)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceVon EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceBewertung: 4 von 5 Sternen4/5 (1)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisVon EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisBewertung: 5 von 5 Sternen5/5 (6)

- Mastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsVon EverandMastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsBewertung: 4.5 von 5 Sternen4.5/5 (21)

- Value: The Four Cornerstones of Corporate FinanceVon EverandValue: The Four Cornerstones of Corporate FinanceBewertung: 5 von 5 Sternen5/5 (2)

- Product-Led Growth: How to Build a Product That Sells ItselfVon EverandProduct-Led Growth: How to Build a Product That Sells ItselfBewertung: 5 von 5 Sternen5/5 (1)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorVon EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNoch keine Bewertungen

- Finance Basics (HBR 20-Minute Manager Series)Von EverandFinance Basics (HBR 20-Minute Manager Series)Bewertung: 4.5 von 5 Sternen4.5/5 (32)

- Financial Leadership for Nonprofit Executives: Guiding Your Organization to Long-Term SuccessVon EverandFinancial Leadership for Nonprofit Executives: Guiding Your Organization to Long-Term SuccessBewertung: 4 von 5 Sternen4/5 (2)

- Mind over Money: The Psychology of Money and How to Use It BetterVon EverandMind over Money: The Psychology of Money and How to Use It BetterBewertung: 4 von 5 Sternen4/5 (24)

- YouTube Marketing: Comprehensive Beginners Guide to Learn YouTube Marketing, Tips & Secrets to Growth Hacking Your Channel and Building Profitable Passive Income Business OnlineVon EverandYouTube Marketing: Comprehensive Beginners Guide to Learn YouTube Marketing, Tips & Secrets to Growth Hacking Your Channel and Building Profitable Passive Income Business OnlineBewertung: 4.5 von 5 Sternen4.5/5 (2)

- The Illusion of Innovation: Escape "Efficiency" and Unleash Radical ProgressVon EverandThe Illusion of Innovation: Escape "Efficiency" and Unleash Radical ProgressNoch keine Bewertungen