Das könnte Ihnen auch gefallen

- Petition For GuardianshipDokument2 SeitenPetition For GuardianshipJules VosotrosNoch keine Bewertungen

- Mint Error News Magazine Issue 14Dokument137 SeitenMint Error News Magazine Issue 14Ryan WalkerNoch keine Bewertungen

- Stanley Fischer - Essays From A Time of Crisis PDFDokument550 SeitenStanley Fischer - Essays From A Time of Crisis PDFIsmael ValverdeNoch keine Bewertungen

- IMF & Developing Countries - An Argumentative EssayDokument19 SeitenIMF & Developing Countries - An Argumentative EssayMaas Riyaz Malik100% (7)

- A Fistful of DollarsDokument78 SeitenA Fistful of DollarsGalen LinderNoch keine Bewertungen

- Answer:: ch07: Dealing With Foreign ExchangeDokument10 SeitenAnswer:: ch07: Dealing With Foreign ExchangeTong Yuen ShunNoch keine Bewertungen

- Currency Stability and a Country’s Prosperity: "Does a Mandatory Currency Stability Law Determine the Stability and or Prosperity of a Country?"Von EverandCurrency Stability and a Country’s Prosperity: "Does a Mandatory Currency Stability Law Determine the Stability and or Prosperity of a Country?"Noch keine Bewertungen

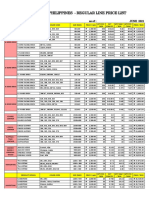

- PHOMI Regular Line June 2021Dokument3 SeitenPHOMI Regular Line June 2021Agus AsnafiNoch keine Bewertungen

- Financial Crises: Lessons From The Past, Preparation For The FutureDokument298 SeitenFinancial Crises: Lessons From The Past, Preparation For The FutureJayeshNoch keine Bewertungen

- Messari Report Asia Crypto LandscapeDokument99 SeitenMessari Report Asia Crypto LandscapeDicky IrwansyahNoch keine Bewertungen

- Introduction of Imf: 1.1 MeaningDokument58 SeitenIntroduction of Imf: 1.1 MeaningRiSHI KeSH GawaINoch keine Bewertungen

- International Financial ArchitectureDokument6 SeitenInternational Financial ArchitectureMuthu NainarNoch keine Bewertungen

- Modelo Presupuesto Inglés ExcelDokument2 SeitenModelo Presupuesto Inglés ExcelJorge Martinez100% (1)

- 102 80 1443647577194 Gutner30Sept2015Dokument24 Seiten102 80 1443647577194 Gutner30Sept2015jomiljkovicNoch keine Bewertungen

- The International Lender of Last ResortDokument28 SeitenThe International Lender of Last ResortchalikanoNoch keine Bewertungen

- WP 1820Dokument42 SeitenWP 1820USR4Noch keine Bewertungen

- Reading - What Is The Role of The IMF and The World Bank - International BusinessDokument24 SeitenReading - What Is The Role of The IMF and The World Bank - International BusinessMichaella PurgananNoch keine Bewertungen

- Macroeconomic RelevanceDokument41 SeitenMacroeconomic RelevanceTBP_Think_TankNoch keine Bewertungen

- D T Llewellyn, R Ortner, H Stepic, S K Zapotocky Is There A Future For Regional Banks and Regional Exchanges The Strategies of Selected Austrian Finance InstitutionsDokument551 SeitenD T Llewellyn, R Ortner, H Stepic, S K Zapotocky Is There A Future For Regional Banks and Regional Exchanges The Strategies of Selected Austrian Finance InstitutionsHekuran ZoguNoch keine Bewertungen

- The IMF and Economic Policy Unit 1 Macroeconomic Stabilisation and The Role of The IMFDokument37 SeitenThe IMF and Economic Policy Unit 1 Macroeconomic Stabilisation and The Role of The IMFR SHEGIWALNoch keine Bewertungen

- The Battle For The Bank: by Ngaire WoodsDokument8 SeitenThe Battle For The Bank: by Ngaire WoodsAfnan DouglasNoch keine Bewertungen

- Banking Crises and Financial Stability: Draft Syllabus: GLBL 311, GLBL 781 and Econ 480Dokument8 SeitenBanking Crises and Financial Stability: Draft Syllabus: GLBL 311, GLBL 781 and Econ 480Tyler Hayashi SapsfordNoch keine Bewertungen

- ImfDokument47 SeitenImfJash ShethiaNoch keine Bewertungen

- World Bank and ImfDokument14 SeitenWorld Bank and ImfSaket ShahareNoch keine Bewertungen

- Q.1 Highlight The Role of International Monetary Fund (IMF) and World Bank in Economies of The Developing NationsDokument27 SeitenQ.1 Highlight The Role of International Monetary Fund (IMF) and World Bank in Economies of The Developing NationsSheikh Fareed AliNoch keine Bewertungen

- 4-Regulation and Responsibility of Credit Rating Agencies Vis-À-Vis Current Economic CrisisDokument21 Seiten4-Regulation and Responsibility of Credit Rating Agencies Vis-À-Vis Current Economic CrisisManisha SharmaNoch keine Bewertungen

- Banking Law: DR Ram Manohar Lohiya National Law UniversityDokument4 SeitenBanking Law: DR Ram Manohar Lohiya National Law UniversityParth ChowdheryNoch keine Bewertungen

- THESIS Henri Erti FinalDokument66 SeitenTHESIS Henri Erti FinalHenri ErtiNoch keine Bewertungen

- BCN Working Paper FinalDokument78 SeitenBCN Working Paper Finalnishant6907Noch keine Bewertungen

- Evaluating The International Monetary System and The Availability To Move Towards One Single Global CurrencyDokument25 SeitenEvaluating The International Monetary System and The Availability To Move Towards One Single Global Currencyboomfox17Noch keine Bewertungen

- Overview On IMF Reform: Edwin M. TrumanDokument96 SeitenOverview On IMF Reform: Edwin M. Trumannasir hussainNoch keine Bewertungen

- Role of The International Monetary Fund in The Recent Global Financial CrisisDokument9 SeitenRole of The International Monetary Fund in The Recent Global Financial Crisissimmi kaushikNoch keine Bewertungen

- International Financial InstitutionsDokument9 SeitenInternational Financial InstitutionsgzalyNoch keine Bewertungen

- Top and Emerging RisksDokument16 SeitenTop and Emerging RisksHani ChkessNoch keine Bewertungen

- Bretton Woods InstitutionsDokument23 SeitenBretton Woods InstitutionsJeanNoch keine Bewertungen

- Structural Causes of The Global Financial Crisis: A Critical Assessment of The "New Financial Architecture"Dokument63 SeitenStructural Causes of The Global Financial Crisis: A Critical Assessment of The "New Financial Architecture"ejazsulemanNoch keine Bewertungen

- Bispap79 Re-Thinking The Lender of Last ResortDokument140 SeitenBispap79 Re-Thinking The Lender of Last ResortElidas SwesiNoch keine Bewertungen

- International Business Hill 9th Edition Solutions ManualDokument16 SeitenInternational Business Hill 9th Edition Solutions ManualJessicaJohnsonqfzm100% (37)

- Imf and It'S Surveillance: Dr. Ram Manohar Lohiya National Law UniversityDokument15 SeitenImf and It'S Surveillance: Dr. Ram Manohar Lohiya National Law UniversityAditya Pratap SinghNoch keine Bewertungen

- Project Report On Internatinal Monetary FundDokument60 SeitenProject Report On Internatinal Monetary FundRiSHI KeSH GawaINoch keine Bewertungen

- Selected Indicators of Financial Stability: William R. Nelson and Roberto PerliDokument30 SeitenSelected Indicators of Financial Stability: William R. Nelson and Roberto PerliManish KumarNoch keine Bewertungen

- Eichengreen, Lombardi, Malkin - Multilayered Governance and The International Financial Architecture... (2018)Dokument14 SeitenEichengreen, Lombardi, Malkin - Multilayered Governance and The International Financial Architecture... (2018)Bautista GriffiniNoch keine Bewertungen

- Desdolarizacion PeruanaDokument25 SeitenDesdolarizacion PeruanaAnonymous RLfGsm7lvWNoch keine Bewertungen

- The Power of The Borrower: Imf Responsiveness To Emerging Market EconomiesDokument44 SeitenThe Power of The Borrower: Imf Responsiveness To Emerging Market EconomiesManju PalegarNoch keine Bewertungen

- Axel Dreher: Hwwa Discussion PaperDokument66 SeitenAxel Dreher: Hwwa Discussion Papersalim bay1982Noch keine Bewertungen

- Dissertation FinalDokument39 SeitenDissertation FinalSarvesh Raj MehtaNoch keine Bewertungen

- Monetary FundDokument18 SeitenMonetary FundDaria BuhusNoch keine Bewertungen

- WP 1773Dokument41 SeitenWP 1773Diego HongNoch keine Bewertungen

- Global Banking Glut and Loan Risk PremiumDokument46 SeitenGlobal Banking Glut and Loan Risk PremiumNaufal SanaullahNoch keine Bewertungen

- What Does Excess Bank Liquidity Say About The Loan Market in Less Developed Countries?Dokument16 SeitenWhat Does Excess Bank Liquidity Say About The Loan Market in Less Developed Countries?SafiqHasanNoch keine Bewertungen

- Adbi wp297 PDFDokument31 SeitenAdbi wp297 PDFgilangNoch keine Bewertungen

- Berger, A., & Bouwman, C. (2009) .Dokument59 SeitenBerger, A., & Bouwman, C. (2009) .Vita NataliaNoch keine Bewertungen

- The Reform of The Governance of The IFIs - A Critical AssessmentDokument25 SeitenThe Reform of The Governance of The IFIs - A Critical AssessmentkipkarNoch keine Bewertungen

- Department of Economics Working Paper SeriesDokument37 SeitenDepartment of Economics Working Paper SeriesPrakhar GuptaNoch keine Bewertungen

- Dealing With Quantitative Easing Spillovers in East Asia: The Role of Institutions and Macroprudential PolicyDokument32 SeitenDealing With Quantitative Easing Spillovers in East Asia: The Role of Institutions and Macroprudential PolicyADBI PublicationsNoch keine Bewertungen

- Pr021213 LetterDokument8 SeitenPr021213 Letterpetere056Noch keine Bewertungen

- Organization Structure and Functing of WTO, IMF, IBRD, IfC, ADB and Their Role of Managing International Liquidity ProblemDokument22 SeitenOrganization Structure and Functing of WTO, IMF, IBRD, IfC, ADB and Their Role of Managing International Liquidity Problemmd.jewel rana100% (2)

- The Changing Role of Central Banks (Goodhart 2010)Dokument33 SeitenThe Changing Role of Central Banks (Goodhart 2010)MarcoKreNoch keine Bewertungen

- 59 Understanding The Dynamics of Foreign Reserve Management The Central Bankintervention Policy and The Exchange Rate FundamentalsDokument47 Seiten59 Understanding The Dynamics of Foreign Reserve Management The Central Bankintervention Policy and The Exchange Rate FundamentalsMailNoch keine Bewertungen

- Development, The IMF, & Institutional Investors: The Mexican Financial CrisisDokument24 SeitenDevelopment, The IMF, & Institutional Investors: The Mexican Financial CrisisBhanu MehraNoch keine Bewertungen

- Finance and Economics Discussion SeriesDokument38 SeitenFinance and Economics Discussion SeriesChong PengNoch keine Bewertungen

- Epr 2022 Fima-Repo ChoiDokument22 SeitenEpr 2022 Fima-Repo ChoiKelvin MishoshoNoch keine Bewertungen

- Tam505 Case Imf & South KoreaDokument11 SeitenTam505 Case Imf & South Koreayeiry27Noch keine Bewertungen

- This Content Downloaded From 49.127.79.168 On Thu, 04 Mar 2021 22:27:34 UTCDokument23 SeitenThis Content Downloaded From 49.127.79.168 On Thu, 04 Mar 2021 22:27:34 UTCNgoc NguyenNoch keine Bewertungen

- ADBI News: Volume 1 Number 2 (2007)Dokument8 SeitenADBI News: Volume 1 Number 2 (2007)ADBI PublicationsNoch keine Bewertungen

- MNYTHEO TranscriptDokument6 SeitenMNYTHEO TranscriptJelly AceNoch keine Bewertungen

- Trade & Finance Bulletin December 2011Dokument12 SeitenTrade & Finance Bulletin December 2011rodobejaranoNoch keine Bewertungen

- Bulletin 2010 Sep 7Dokument5 SeitenBulletin 2010 Sep 7rodobejaranoNoch keine Bewertungen

- Bulletin 2010 Sep 7Dokument5 SeitenBulletin 2010 Sep 7rodobejaranoNoch keine Bewertungen

- Bulletin Nov 02 2010Dokument6 SeitenBulletin Nov 02 2010rodobejaranoNoch keine Bewertungen

- Bulletin 2010 Aug 3Dokument17 SeitenBulletin 2010 Aug 3rodobejaranoNoch keine Bewertungen

- Bulletin 2010 Jul 7Dokument10 SeitenBulletin 2010 Jul 7rodobejaranoNoch keine Bewertungen

- Bulletin 2010 May 5Dokument8 SeitenBulletin 2010 May 5rodobejaranoNoch keine Bewertungen

- Bulletin 09 Nov 27Dokument8 SeitenBulletin 09 Nov 27rodobejaranoNoch keine Bewertungen

- Bulletin 2010 Mar 11Dokument8 SeitenBulletin 2010 Mar 11rodobejaranoNoch keine Bewertungen

- Bulletin 09 Dec 15Dokument7 SeitenBulletin 09 Dec 15rodobejaranoNoch keine Bewertungen

- Bulletin 09 Sep 29Dokument8 SeitenBulletin 09 Sep 29rodobejaranoNoch keine Bewertungen

- Bulletin 09 Oct 28Dokument12 SeitenBulletin 09 Oct 28rodobejaranoNoch keine Bewertungen

- Bulletin 09 Sep 11Dokument6 SeitenBulletin 09 Sep 11rodobejaranoNoch keine Bewertungen

- Bulletin 09 July 20Dokument10 SeitenBulletin 09 July 20rodobejaranoNoch keine Bewertungen

- Bulletin 09 July 02Dokument5 SeitenBulletin 09 July 02rodobejaranoNoch keine Bewertungen

- Bulletin 09 May 10Dokument10 SeitenBulletin 09 May 10rodobejarano100% (2)

- Navigating Rough Tides AheadDokument63 SeitenNavigating Rough Tides AheadSamiul21Noch keine Bewertungen

- The UK TodayDokument3 SeitenThe UK TodayMeimeBlumsNoch keine Bewertungen

- Resolution No. 15-Adopting The 1% BCPCDokument2 SeitenResolution No. 15-Adopting The 1% BCPCBarangay MambaliliNoch keine Bewertungen

- Social Studies Worksheet PDFDokument10 SeitenSocial Studies Worksheet PDFRay-Shaun Bourne100% (2)

- Final Chapter 1 5 - MergedDokument77 SeitenFinal Chapter 1 5 - MergedMolleno MichelleNoch keine Bewertungen

- Global Debt and Equity MarketsDokument6 SeitenGlobal Debt and Equity MarketsAzael May PenaroyoNoch keine Bewertungen

- Solution To Problems - Chapter 9Dokument25 SeitenSolution To Problems - Chapter 9GFGSHSNoch keine Bewertungen

- Cash Flow by QuarterDokument1 SeiteCash Flow by QuarterJay DisomimbaNoch keine Bewertungen

- International Financial Management: Course Coordinator: V. Raveendra Saradhi Course Credit: 3Dokument4 SeitenInternational Financial Management: Course Coordinator: V. Raveendra Saradhi Course Credit: 3Tanu GuptaNoch keine Bewertungen

- Math Form Two April Holiday Assignment 2024Dokument4 SeitenMath Form Two April Holiday Assignment 2024Anderson YaendiNoch keine Bewertungen

- Exchange Rate MechanismDokument42 SeitenExchange Rate Mechanismpriya nNoch keine Bewertungen

- Free Numerical Reasoning Test QuestionsDokument16 SeitenFree Numerical Reasoning Test QuestionsCristina Iv100% (1)

- Assessment Instrument ChecklistDokument2 SeitenAssessment Instrument Checklistapi-351531345Noch keine Bewertungen

- 2019 Q3 CushWake Jakarta IndustrialDokument2 Seiten2019 Q3 CushWake Jakarta IndustrialCookiesNoch keine Bewertungen

- Crypto Analytical RebuttalsDokument8 SeitenCrypto Analytical RebuttalsoesmfpomsepofNoch keine Bewertungen

- SA110 LW200xxx ServiceanleitungDokument24 SeitenSA110 LW200xxx ServiceanleitungKarl-Heinz WellerNoch keine Bewertungen

- Motion To Compel Production of Evidence Seized at TrialDokument4 SeitenMotion To Compel Production of Evidence Seized at TrialCarl MullanNoch keine Bewertungen

- JAFIDVol 2Dokument230 SeitenJAFIDVol 2Oyebisi OpeyemiNoch keine Bewertungen

- Thermal: Q) "Korba" Super Thermal Power Plant Is Situated in - ?Dokument36 SeitenThermal: Q) "Korba" Super Thermal Power Plant Is Situated in - ?geeteshjadhavNoch keine Bewertungen

- Presentation of The Philippine Public Sector Accounting Standards (Ppsas)Dokument23 SeitenPresentation of The Philippine Public Sector Accounting Standards (Ppsas)Leonardo Don Alis CordovaNoch keine Bewertungen

- Yr 12 Economics Textbook 2024Dokument416 SeitenYr 12 Economics Textbook 2024bradendent2Noch keine Bewertungen

- 2004 Technical - Analysis - of - FOREX - by - RSI - Indic PDFDokument7 Seiten2004 Technical - Analysis - of - FOREX - by - RSI - Indic PDFAli AzizNoch keine Bewertungen

- Macro Practice - QuestionsDokument4 SeitenMacro Practice - QuestionsShiva MehtaNoch keine Bewertungen

- Chile - The Latin American Tiger - v1 1Dokument17 SeitenChile - The Latin American Tiger - v1 1Ramyaa RameshNoch keine Bewertungen