Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Vault Guide - Energy IndustryDokument172 SeitenVault Guide - Energy IndustrymerollinsNoch keine Bewertungen

- Vault Guide To Private EquityDokument336 SeitenVault Guide To Private Equitydosikeow50% (2)

- Presentation For UCLDokument33 SeitenPresentation For UCLkarimbandari100% (2)

- Vault Guide To Technology Careers (2004)Dokument128 SeitenVault Guide To Technology Careers (2004)ZhiminXuNoch keine Bewertungen

- Problem Solving With McKinsey MethodDokument23 SeitenProblem Solving With McKinsey MethodRafiq Batcha96% (27)

- Vault GuideDokument126 SeitenVault GuideDeepshikha SinghNoch keine Bewertungen

- Chamada Publica FEPprospec0311 Relatorio7 Sumario InglesDokument30 SeitenChamada Publica FEPprospec0311 Relatorio7 Sumario InglesfwfsdNoch keine Bewertungen

- BAIN BRIEF Steering Through The Oil StormDokument8 SeitenBAIN BRIEF Steering Through The Oil StormfwfsdNoch keine Bewertungen

- Problem Solving With McKinsey MethodDokument23 SeitenProblem Solving With McKinsey MethodRafiq Batcha96% (27)

- BB Right SizingDokument12 SeitenBB Right SizingfwfsdNoch keine Bewertungen

- 7973278Dokument147 Seiten7973278fwfsdNoch keine Bewertungen

- Eight Key Levers For Effective Large-Capex-Project ManagementDokument21 SeitenEight Key Levers For Effective Large-Capex-Project ManagementIndrajeet RoyNoch keine Bewertungen

- Project WHO Investor Presentation VFDokument31 SeitenProject WHO Investor Presentation VFfwfsdNoch keine Bewertungen

- BPV Organisational EnablersDokument10 SeitenBPV Organisational EnablersfwfsdNoch keine Bewertungen

- Jennifer Howells 0Dokument27 SeitenJennifer Howells 0fwfsdNoch keine Bewertungen

- B00PWE81VE Strategic StorytellingDokument161 SeitenB00PWE81VE Strategic Storytellingmoidodyr50% (2)

- BPV ApproachDokument13 SeitenBPV ApproachfwfsdNoch keine Bewertungen

- 2014 Las Session 11Dokument57 Seiten2014 Las Session 11fwfsdNoch keine Bewertungen

- 07 Heinz Private EquityDokument27 Seiten07 Heinz Private EquityfwfsdNoch keine Bewertungen

- 8291490Dokument98 Seiten8291490fwfsdNoch keine Bewertungen

- Organization:: Overview of Core FrameworksDokument91 SeitenOrganization:: Overview of Core FrameworksfwfsdNoch keine Bewertungen

- Decision Handbook IntroDokument9 SeitenDecision Handbook IntrofwfsdNoch keine Bewertungen

- 2014 Dec Spee Operational Excellence CarusoDokument36 Seiten2014 Dec Spee Operational Excellence CarusofwfsdNoch keine Bewertungen

- MCkinsey Internal Guide - BiomassDokument23 SeitenMCkinsey Internal Guide - BiomassfwfsdNoch keine Bewertungen

- Presentation 131107 Davis Lambert How Unconventionals Changing MarketsDokument36 SeitenPresentation 131107 Davis Lambert How Unconventionals Changing MarketsfwfsdNoch keine Bewertungen

- TechUK McKinseyPresentation VFDokument15 SeitenTechUK McKinseyPresentation VFfwfsdNoch keine Bewertungen

- JMcKinsey - Juden - FinalDokument31 SeitenJMcKinsey - Juden - FinalfwfsdNoch keine Bewertungen

- Derkach McKinsey ATOMEXPO 2014Dokument12 SeitenDerkach McKinsey ATOMEXPO 2014fwfsdNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Ali UblDokument135 SeitenAli UblMuhammad SajidNoch keine Bewertungen

- Automatic PaymentsDokument12 SeitenAutomatic PaymentsfinerpmanyamNoch keine Bewertungen

- Business EnvironmentDokument58 SeitenBusiness EnvironmentKalpita DhuriNoch keine Bewertungen

- Prulink Elite Protector Series BrochureDokument2 SeitenPrulink Elite Protector Series BrochureSakurako ChachamiNoch keine Bewertungen

- Fundamentals of Auditing and Assurance Services OverviewDokument8 SeitenFundamentals of Auditing and Assurance Services OverviewSkye LeeNoch keine Bewertungen

- Eng. Book PDFDokument93 SeitenEng. Book PDFSelvaraj VillyNoch keine Bewertungen

- Notes On MicrofinanceDokument8 SeitenNotes On MicrofinanceMapuia Lal Pachuau100% (2)

- Teknik AkersonDokument60 SeitenTeknik Akerson060098401Noch keine Bewertungen

- Nse BookDokument393 SeitenNse BookBright ThomasNoch keine Bewertungen

- Deposit, Mutuum, CommudatumDokument33 SeitenDeposit, Mutuum, CommudatumkimuchosNoch keine Bewertungen

- Unit 1 - IS-LM-PCDokument27 SeitenUnit 1 - IS-LM-PCGunjan ChoudharyNoch keine Bewertungen

- Banking AwarenessDokument130 SeitenBanking AwarenessDAX LABORATORY100% (2)

- Icici Bank Financial AnalysisDokument46 SeitenIcici Bank Financial AnalysisPiyush Goyal88% (8)

- 1910dsycp 11600Dokument2 Seiten1910dsycp 11600brandiwinde41Noch keine Bewertungen

- Chapter 4 Uses and Sources of STF and LTFDokument49 SeitenChapter 4 Uses and Sources of STF and LTFChristopher Beltran CauanNoch keine Bewertungen

- Bansi Khakhkhar PDFDokument74 SeitenBansi Khakhkhar PDFVishu MakwanaNoch keine Bewertungen

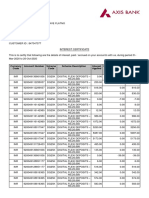

- Interest CertificateDokument2 SeitenInterest CertificatesumitNoch keine Bewertungen

- Capital Structure Policy I Ebit-Eps Analysis: Page 1 of 2Dokument2 SeitenCapital Structure Policy I Ebit-Eps Analysis: Page 1 of 2Danzo ShahNoch keine Bewertungen

- Audit of CashDokument9 SeitenAudit of CashEmma Mariz Garcia25% (8)

- Module 5 - Extinguishment of An ObligationDokument19 SeitenModule 5 - Extinguishment of An ObligationCriselyne BernabeNoch keine Bewertungen

- Malaysia and The Global Financial Crisis, The Case of Malaysia As A Plan-Rationality State in Responding The CrisisDokument22 SeitenMalaysia and The Global Financial Crisis, The Case of Malaysia As A Plan-Rationality State in Responding The CrisisErika Angelika60% (5)

- Far: Property, Plant, and Equipment: I. Definition and NatureDokument13 SeitenFar: Property, Plant, and Equipment: I. Definition and NatureAl ChuaNoch keine Bewertungen

- Banking RatiosDokument7 SeitenBanking Ratioszhalak04Noch keine Bewertungen

- Recruiters Sites TetenDokument83 SeitenRecruiters Sites TetenArvinthNoch keine Bewertungen

- Annual Report 2019 - 0Dokument116 SeitenAnnual Report 2019 - 0Junaid MalikNoch keine Bewertungen

- Skanray Technologies Pvt. LTD: Company ProfileDokument33 SeitenSkanray Technologies Pvt. LTD: Company ProfileMars NaspekovNoch keine Bewertungen

- MPS - Budget TemplateDokument4 SeitenMPS - Budget TemplateADETUNJI ADENIYI SAMUELNoch keine Bewertungen

- Alanis Parks Department: Analyze and Chart Financial DataDokument7 SeitenAlanis Parks Department: Analyze and Chart Financial DataJacob SheridanNoch keine Bewertungen

- Notes in Tax On IndividualsDokument4 SeitenNotes in Tax On IndividualsPaula BatulanNoch keine Bewertungen

- CFD Forex Broker Report - 7th EditionDokument75 SeitenCFD Forex Broker Report - 7th EditiongghghgfhfghNoch keine Bewertungen