Das könnte Ihnen auch gefallen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Workshop 5. Balance SheetDokument7 SeitenWorkshop 5. Balance SheetNorma Melissa Cantillo CsNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Axix Bank ProjectDokument67 SeitenAxix Bank ProjectSâñjây BîñdNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- .Au Forms Change of Ownership FormDokument3 Seiten.Au Forms Change of Ownership FormLucas SchcolnikNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Far East Vs Gold PalaceDokument4 SeitenFar East Vs Gold PalaceGeeanNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Sale of Goods On Consignment AgreementDokument3 SeitenSale of Goods On Consignment AgreementJef PowellNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- English II MaterialsDokument46 SeitenEnglish II MaterialsRiyan NugrahaNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Latihan Soal Rekonsiliasi BankDokument1 SeiteLatihan Soal Rekonsiliasi BankIchsan WibowoNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Project For Midterm: Case Problem No. 1Dokument4 SeitenProject For Midterm: Case Problem No. 1Leanne Joyce QuintoNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- 1311 Remuneration Structures Study en 0Dokument187 Seiten1311 Remuneration Structures Study en 0Andrei SavvaNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Madoff's American Express Corporate Card StatementDokument30 SeitenMadoff's American Express Corporate Card StatementInvestor Protection100% (3)

- Banking in India For WbcsDokument29 SeitenBanking in India For WbcsSubhasis MaityNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

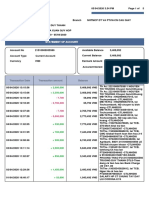

- Statement of Account: Transaction Amount Balance Transaction Details Transaction DateDokument5 SeitenStatement of Account: Transaction Amount Balance Transaction Details Transaction DatehyhNoch keine Bewertungen

- Generic Ic Disc PresentationDokument55 SeitenGeneric Ic Disc PresentationInternational Tax Magazine; David Greenberg PhD, MSA, EA, CPA; Tax Group International; 646-705-2910Noch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Statement On Impact of Audit Qualifications For The Period Ended March 31, 2016 (Company Update)Dokument3 SeitenStatement On Impact of Audit Qualifications For The Period Ended March 31, 2016 (Company Update)Shyam SunderNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Acc Project 2021 22Dokument14 SeitenAcc Project 2021 22Piyush GoyalNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- 1538139921616Dokument6 Seiten1538139921616Hena SharmaNoch keine Bewertungen

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDokument8 SeitenStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancePushkar PandeyNoch keine Bewertungen

- Liquidation FormDokument4 SeitenLiquidation FormMarlyn E. Azurin100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Code of Ethics and Republic Act 9298 PDFDokument18 SeitenThe Code of Ethics and Republic Act 9298 PDFShyrine EjemNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Methods and Procedures For Risk Profiling ofDokument18 SeitenMethods and Procedures For Risk Profiling ofRohith VijayanNoch keine Bewertungen

- LIC Jeevan Saral - Best Insurance Plan FromDokument18 SeitenLIC Jeevan Saral - Best Insurance Plan FromRohit JagtapNoch keine Bewertungen

- UK Financial Regulation Ed23-5 PDFDokument298 SeitenUK Financial Regulation Ed23-5 PDFVincenzo Somma100% (2)

- Earnings Insight FactSet 01-2019Dokument29 SeitenEarnings Insight FactSet 01-2019krg09Noch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- 4 6039689226176431369Dokument8 Seiten4 6039689226176431369Nárdï TêsfðýêNoch keine Bewertungen

- Account StatementDokument12 SeitenAccount StatementManu HegdeNoch keine Bewertungen

- Anmol JeevanDokument13 SeitenAnmol JeevanUtkarshNoch keine Bewertungen

- 1mca Education Loan SchemeDokument3 Seiten1mca Education Loan SchemeSurendran NagiahNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Statement 517057 86377450 18 06 2020 17 09 2020Dokument4 SeitenStatement 517057 86377450 18 06 2020 17 09 2020YeazeNoch keine Bewertungen

- Central Bank of India: New Business GroupDokument7 SeitenCentral Bank of India: New Business GroupAbhishek BoseNoch keine Bewertungen

- STMNT 112013 9773Dokument3 SeitenSTMNT 112013 9773redbird77100% (1)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)