Das könnte Ihnen auch gefallen

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideVon EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNoch keine Bewertungen

- Property, Plant and Equipment Property, Plant and EquipmentDokument5 SeitenProperty, Plant and Equipment Property, Plant and EquipmentWertdie stanNoch keine Bewertungen

- Accounting For PPE - PAS 16Dokument39 SeitenAccounting For PPE - PAS 16Marriel Fate Cullano100% (1)

- Chapter 15 - Pas 16 PpeDokument36 SeitenChapter 15 - Pas 16 PpeMarriel Fate CullanoNoch keine Bewertungen

- Chapter 15 - Property, Plant, and EquipmentDokument3 SeitenChapter 15 - Property, Plant, and EquipmentFerb CruzadaNoch keine Bewertungen

- Chapter 14 - Pas 16 Property, Plant and Equipment: Measurement After RecognitionDokument5 SeitenChapter 14 - Pas 16 Property, Plant and Equipment: Measurement After RecognitionVince PeredaNoch keine Bewertungen

- Ias 16Dokument26 SeitenIas 16Niharika MishraNoch keine Bewertungen

- Property Plant and EquipmentDokument16 SeitenProperty Plant and EquipmentArly Kurt TorresNoch keine Bewertungen

- Ia 2 - Ppe SheDokument22 SeitenIa 2 - Ppe SheAlisonNoch keine Bewertungen

- Pas 16Dokument8 SeitenPas 16Maxyne Dheil CastroNoch keine Bewertungen

- Property Plant and EquipmentDokument5 SeitenProperty Plant and EquipmentSinead ErelahNoch keine Bewertungen

- PSBA - Property, Plant and EquipmentDokument13 SeitenPSBA - Property, Plant and EquipmentAbdulmajed Unda MimbantasNoch keine Bewertungen

- Historical Cost of Property, Plant and EquipmentDokument9 SeitenHistorical Cost of Property, Plant and EquipmentChinchin Ilagan DatayloNoch keine Bewertungen

- INTACC 1 - PPE ReviewerDokument2 SeitenINTACC 1 - PPE ReviewerRandom VidsNoch keine Bewertungen

- Ia 2 Ppe She 1Dokument22 SeitenIa 2 Ppe She 1AlisonNoch keine Bewertungen

- Script Ending Pork EmpanadaDokument3 SeitenScript Ending Pork EmpanadaRose MarieNoch keine Bewertungen

- PAS 16 Property, Plant and EquipmentDokument4 SeitenPAS 16 Property, Plant and Equipmentpanda 1Noch keine Bewertungen

- Chapter 17 - Ppe - AssignmentDokument16 SeitenChapter 17 - Ppe - Assignmentsabina del monteNoch keine Bewertungen

- Module 7 - PAS 16 PPEDokument6 SeitenModule 7 - PAS 16 PPEbladdor DG.Noch keine Bewertungen

- IntAcc1 - CHAPTER 23 and 25Dokument10 SeitenIntAcc1 - CHAPTER 23 and 25Clyde Justine CablingNoch keine Bewertungen

- Studet Practical Accounting Ch17 PPE AcquisitionDokument16 SeitenStudet Practical Accounting Ch17 PPE Acquisitionsabina del monteNoch keine Bewertungen

- Ppe MarbellaDokument5 SeitenPpe MarbellaDazzelle BasarteNoch keine Bewertungen

- Chapter 22 Investment Property (Cash Surrender Value)Dokument5 SeitenChapter 22 Investment Property (Cash Surrender Value)Liana LopezNoch keine Bewertungen

- Chapter 10 Property, Plant and EquipmentDokument11 SeitenChapter 10 Property, Plant and EquipmentAngelica Joy ManaoisNoch keine Bewertungen

- Summary PpeDokument8 SeitenSummary PpeJenilyn CalaraNoch keine Bewertungen

- (Acctg 112) Pas 16 & 23Dokument4 Seiten(Acctg 112) Pas 16 & 23Mae PandoraNoch keine Bewertungen

- PpeDokument5 SeitenPpeXairah Kriselle de OcampoNoch keine Bewertungen

- Transition To PFRS (The Beginning of The Earliest Period For Which Entity Presents Full Comparative InformationDokument8 SeitenTransition To PFRS (The Beginning of The Earliest Period For Which Entity Presents Full Comparative InformationMary Joy Morales BuquiranNoch keine Bewertungen

- Property Plant and Equipment Adacp Outline Chapter 10Dokument9 SeitenProperty Plant and Equipment Adacp Outline Chapter 10raderpinaNoch keine Bewertungen

- Notes On Intermediate AccountingDokument4 SeitenNotes On Intermediate AccountingJanna DolorNoch keine Bewertungen

- Date of Transition To PFRS (The Beginning of The Earliest Period For Which Entity Presents FullDokument20 SeitenDate of Transition To PFRS (The Beginning of The Earliest Period For Which Entity Presents FullMary Joy Morales BuquiranNoch keine Bewertungen

- Non-Current Assets - Ppe: Conceptual Framework & Accounting StandardsDokument14 SeitenNon-Current Assets - Ppe: Conceptual Framework & Accounting StandardsDebbie Grace Latiban LinazaNoch keine Bewertungen

- Technical SummaryDokument2 SeitenTechnical Summarysza_13100% (2)

- Smes - Equity Share-Based Payment Specialized Activities HyperinflationDokument13 SeitenSmes - Equity Share-Based Payment Specialized Activities HyperinflationToni Rose Hernandez LualhatiNoch keine Bewertungen

- Property, Plant and Equipment (IAS 16)Dokument4 SeitenProperty, Plant and Equipment (IAS 16)Yunus AlamgeerNoch keine Bewertungen

- IAS16Dokument2 SeitenIAS16Atif RehmanNoch keine Bewertungen

- EXAMDokument13 SeitenEXAMJess SiazonNoch keine Bewertungen

- Intacc Ass 4Dokument5 SeitenIntacc Ass 4Pixie CanaveralNoch keine Bewertungen

- PPE (Property, Plant and Equipment)Dokument4 SeitenPPE (Property, Plant and Equipment)Avika Ainsley Abique TakahataNoch keine Bewertungen

- Blessed Me LordDokument168 SeitenBlessed Me LordBoa HancockNoch keine Bewertungen

- 17 Property Plant and Equipment PART 1 PDFDokument25 Seiten17 Property Plant and Equipment PART 1 PDFJay Aubrey PinedaNoch keine Bewertungen

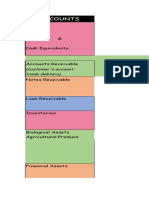

- Accounts: (Customer's Account, Trade Debtors)Dokument48 SeitenAccounts: (Customer's Account, Trade Debtors)RaphaelleNoch keine Bewertungen

- Philippine Accounting Standards 16 & 23 (PPE and Borrowing Cost)Dokument32 SeitenPhilippine Accounting Standards 16 & 23 (PPE and Borrowing Cost)Ecka Tubay33% (3)

- Module 7 PPEDokument6 SeitenModule 7 PPECha Eun WooNoch keine Bewertungen

- Chapter 10 NotesDokument22 SeitenChapter 10 NotesSittie Ainna Acmed UnteNoch keine Bewertungen

- Ias 16 Property Plant Equipment v1 080713Dokument7 SeitenIas 16 Property Plant Equipment v1 080713Phebieon MukwenhaNoch keine Bewertungen

- Lecture Notes On PPE - Acq & RecDokument6 SeitenLecture Notes On PPE - Acq & Recjudel ArielNoch keine Bewertungen

- Chapter 10 PropertyDokument10 SeitenChapter 10 Propertymaria isabellaNoch keine Bewertungen

- Reviewer in PPEDokument16 SeitenReviewer in PPEDewi Leigh Ann Mangubat50% (2)

- StalasaDokument23 SeitenStalasajessa mae zerdaNoch keine Bewertungen

- IAS 16 PPE - LectureDokument11 SeitenIAS 16 PPE - LectureBeatrice Ella DomingoNoch keine Bewertungen

- Intangible Assets Under Pfrs ScopeDokument12 SeitenIntangible Assets Under Pfrs ScopeYsabella ChenNoch keine Bewertungen

- BOSCOMDokument18 SeitenBOSCOMArah Opalec100% (1)

- PPEDokument5 SeitenPPERodelia MalacastaNoch keine Bewertungen

- Module 4Dokument10 SeitenModule 4bhettyna noayNoch keine Bewertungen

- Intangible Assets and LiabilitiesDokument13 SeitenIntangible Assets and LiabilitiesApril ManjaresNoch keine Bewertungen

- PPE NotesDokument7 SeitenPPE Noteszxc vbnNoch keine Bewertungen

- Mega Project Assurance: Volume One - The Terminological DictionaryVon EverandMega Project Assurance: Volume One - The Terminological DictionaryNoch keine Bewertungen

- HO FS AnalsisDokument15 SeitenHO FS AnalsisGva Umayam0% (2)

- (Chp10-12) Pas 2 - Inventory, Inventory Valuation and Inventory EstimationDokument10 Seiten(Chp10-12) Pas 2 - Inventory, Inventory Valuation and Inventory Estimationbigbaek0% (3)

- Installment Home Branch Liquidation LT Constn ContractsDokument47 SeitenInstallment Home Branch Liquidation LT Constn ContractsbigbaekNoch keine Bewertungen

- TBCH10Dokument10 SeitenTBCH10rockerNoch keine Bewertungen

- COSO-2013-Diapositivas en InglesDokument39 SeitenCOSO-2013-Diapositivas en InglesAnonymous 9ThJkQrYNoch keine Bewertungen

- Business Combination Problem SetDokument6 SeitenBusiness Combination Problem SetbigbaekNoch keine Bewertungen

- (Chp10-12) Pas 2 - Inventory, Inventory Valuation and Inventory EstimationDokument10 Seiten(Chp10-12) Pas 2 - Inventory, Inventory Valuation and Inventory Estimationbigbaek0% (3)

- TBCH10Dokument10 SeitenTBCH10rockerNoch keine Bewertungen

- Strategic ControlDokument43 SeitenStrategic ControlbigbaekNoch keine Bewertungen

- Prologue PowerpointDokument66 SeitenPrologue PowerpointbigbaekNoch keine Bewertungen

- Mas CVPQ1Dokument2 SeitenMas CVPQ1bigbaekNoch keine Bewertungen

- Chapter 2 - Transfer Taxes and Basic Succession2013Dokument6 SeitenChapter 2 - Transfer Taxes and Basic Succession2013iamjan_10150% (4)

- Inventory MGMT ComprehensiveDokument4 SeitenInventory MGMT ComprehensivebigbaekNoch keine Bewertungen

- Conceptual FrameworkDokument1 SeiteConceptual FrameworkbigbaekNoch keine Bewertungen

- Words UsedDokument1 SeiteWords UsedbigbaekNoch keine Bewertungen

- Excuse LetterDokument1 SeiteExcuse LetterbigbaekNoch keine Bewertungen

- Audit of Cash and Cash EquivalentsDokument38 SeitenAudit of Cash and Cash Equivalentsxxxxxxxxx86% (81)

- I Am Currently Employed As The University NurseDokument2 SeitenI Am Currently Employed As The University NursebigbaekNoch keine Bewertungen

- 5mm Boxes PaperDokument1 Seite5mm Boxes PaperbigbaekNoch keine Bewertungen

- Contract of AgreementDokument1 SeiteContract of AgreementbigbaekNoch keine Bewertungen

- The CommandmentsDokument12 SeitenThe CommandmentsbigbaekNoch keine Bewertungen

- 5e Apollo Shoes CaseDokument163 Seiten5e Apollo Shoes CaseenergizerabbyNoch keine Bewertungen

- Enron Effect SummaryDokument2 SeitenEnron Effect SummarybigbaekNoch keine Bewertungen

- Summary of LAW101Dokument16 SeitenSummary of LAW101bigbaekNoch keine Bewertungen

- Chapter 1 Advanced Acctg. SolmanDokument20 SeitenChapter 1 Advanced Acctg. SolmanLaraNoch keine Bewertungen

- SGV & Co EngagemnetsDokument27 SeitenSGV & Co Engagemnetsbigbaek100% (2)

- Multiple Choice Answers and Solutions: Aquino Locsin David HizonDokument26 SeitenMultiple Choice Answers and Solutions: Aquino Locsin David HizonclaudettegasendoNoch keine Bewertungen

- Blood Pressure Pulse Respiration Temperature O2 Sat Glucose Weight (KG) Blood Pressure Pulse Respiration Temperature O2 Sat Glucose Weight (KG)Dokument2 SeitenBlood Pressure Pulse Respiration Temperature O2 Sat Glucose Weight (KG) Blood Pressure Pulse Respiration Temperature O2 Sat Glucose Weight (KG)bigbaekNoch keine Bewertungen

- Basic Finance in The PhilippinesDokument8 SeitenBasic Finance in The PhilippinesbigbaekNoch keine Bewertungen

- Chapter 2 - Cost Terminology and Cost Behaviors: LO1 LO2 LO3 LO4 LO5Dokument29 SeitenChapter 2 - Cost Terminology and Cost Behaviors: LO1 LO2 LO3 LO4 LO5Chem Mae100% (4)

- Logistics CostDokument3 SeitenLogistics CostSurekha RammoorthyNoch keine Bewertungen

- Cost Classification and Terminologies Harambe University CollegeDokument12 SeitenCost Classification and Terminologies Harambe University Collegeአረጋዊ ሐይለማርያምNoch keine Bewertungen

- Masterpad Solution PresentationDokument19 SeitenMasterpad Solution PresentationnoursfoodforthoughtNoch keine Bewertungen

- PM - MGT1103E - A01E - Group 4 - DIANA UNICHARMDokument57 SeitenPM - MGT1103E - A01E - Group 4 - DIANA UNICHARMKhánh Nguyễn Thị KimNoch keine Bewertungen

- Attest Services VS Advisory Services Advisory - Professional Services OfferedDokument2 SeitenAttest Services VS Advisory Services Advisory - Professional Services OfferedDANIELLE TORRANCE ESPIRITUNoch keine Bewertungen

- ABM 11 - FABM 1 - Q3 - W2 - Module 2-v2Dokument15 SeitenABM 11 - FABM 1 - Q3 - W2 - Module 2-v2Erra Peñaflorida - PedroNoch keine Bewertungen

- Basic Microeconomics REVIEWER - Theory of ProductionDokument2 SeitenBasic Microeconomics REVIEWER - Theory of ProductionJig PerfectoNoch keine Bewertungen

- Borrowing Cost CH 25 Ia Ppe GGDokument4 SeitenBorrowing Cost CH 25 Ia Ppe GGZes ONoch keine Bewertungen

- Marketing Assignment 2021Dokument12 SeitenMarketing Assignment 2021Huzaifa Bin AtaNoch keine Bewertungen

- Job Costing & Contract Costing WorksheetDokument7 SeitenJob Costing & Contract Costing Worksheetakash borseNoch keine Bewertungen

- AUD Southampton PLCDokument3 SeitenAUD Southampton PLCAivie Pangilinan0% (1)

- Test Bank For Macroeconomics 5th Edition Paul Krugman Robin WellsDokument36 SeitenTest Bank For Macroeconomics 5th Edition Paul Krugman Robin Wellsmohur.auszug.zai8x100% (48)

- Commercial ReturnablesDokument70 SeitenCommercial ReturnablesAncaNoch keine Bewertungen

- Chemical Engineering Plant EconomicsDokument7 SeitenChemical Engineering Plant EconomicsRoed Alejandro LlagaNoch keine Bewertungen

- Solution Manual - RANTE COST ACCDokument127 SeitenSolution Manual - RANTE COST ACCray57% (7)

- Cost Acc Unit 1 AssignmentDokument7 SeitenCost Acc Unit 1 AssignmentPrasant EkkaNoch keine Bewertungen

- Chapter 7 Tutorial Solution ManualDokument10 SeitenChapter 7 Tutorial Solution ManualMun Lutfi100% (1)

- United States v. Arthur Pena, 268 F.3d 215, 3rd Cir. (2001)Dokument9 SeitenUnited States v. Arthur Pena, 268 F.3d 215, 3rd Cir. (2001)Scribd Government DocsNoch keine Bewertungen

- SFI - Business Model CanvasDokument10 SeitenSFI - Business Model CanvasThanh HằngNoch keine Bewertungen

- Cost Behaviour 43 Mins: The Following Information Relates To Questions 4.3 To 4.7Dokument5 SeitenCost Behaviour 43 Mins: The Following Information Relates To Questions 4.3 To 4.7Waqas Younas BandukdaNoch keine Bewertungen

- Cost Accounting Foundations and Evolutions: Activity-Based Management and Activity-Based CostingDokument48 SeitenCost Accounting Foundations and Evolutions: Activity-Based Management and Activity-Based CostingPaolo Angel De VeraNoch keine Bewertungen

- Annual Statement: 1 July 2021 - 30 June 2022Dokument6 SeitenAnnual Statement: 1 July 2021 - 30 June 2022Thong THAONoch keine Bewertungen

- Contemporary Financial Management Moyer 12th Edition Solutions ManualDokument16 SeitenContemporary Financial Management Moyer 12th Edition Solutions ManualSteveJacobsafjg100% (37)

- Cfas NotesDokument14 SeitenCfas NotesNoreen CarlosNoch keine Bewertungen

- Feasibility Study-Lecture 4Dokument23 SeitenFeasibility Study-Lecture 4Said ElhantaouiNoch keine Bewertungen

- Brief Explanation of Various Types of Costs in Cost Accounting With Examples PDFDokument6 SeitenBrief Explanation of Various Types of Costs in Cost Accounting With Examples PDFmayankNoch keine Bewertungen

- Management Accounting Tools and Techniques For Reduce CostDokument8 SeitenManagement Accounting Tools and Techniques For Reduce CostFYAJ ROHANNoch keine Bewertungen

- ACCTG 201 Illustrative ProblemsDokument4 SeitenACCTG 201 Illustrative ProblemsJewel Anne RentumaNoch keine Bewertungen