Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Early Release Superannuation Approval 7115569398585Dokument1 SeiteEarly Release Superannuation Approval 7115569398585DanielWildSheepZaninNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Chap 003 SolutionsDokument10 SeitenChap 003 SolutionsFreeBooksandMaterialNoch keine Bewertungen

- 2012 Towers Watson Global Workforce StudyDokument24 Seiten2012 Towers Watson Global Workforce StudySumit RoyNoch keine Bewertungen

- TGDokument2 SeitenTGpr995Noch keine Bewertungen

- Legal Aid ApplicationDokument8 SeitenLegal Aid ApplicationFiona VinerNoch keine Bewertungen

- Partial Withdrawal Form1Dokument2 SeitenPartial Withdrawal Form1KANGSA banikNoch keine Bewertungen

- TVM Assignment 1Dokument1 SeiteTVM Assignment 1Mohammad TayyabNoch keine Bewertungen

- Part A: PersonalDokument2 SeitenPart A: PersonalAacif AliNoch keine Bewertungen

- FMI7e ch25Dokument61 SeitenFMI7e ch25lehoangthuchienNoch keine Bewertungen

- PM Kisan Maan Dhan YojanaDokument1 SeitePM Kisan Maan Dhan YojanaRadhey Shyam KumawatNoch keine Bewertungen

- Essentials of Accounting For Governmental and Not For Profit Organizations 13th Edition Copley Test Bank Full Chapter PDFDokument68 SeitenEssentials of Accounting For Governmental and Not For Profit Organizations 13th Edition Copley Test Bank Full Chapter PDFarianytebh100% (12)

- Salary Tax FormatDokument10 SeitenSalary Tax Formathizbullah chandioNoch keine Bewertungen

- ERIN LEWIS - MARS-Member Annual Retirement Statement - 2023Dokument2 SeitenERIN LEWIS - MARS-Member Annual Retirement Statement - 2023Erin LewisNoch keine Bewertungen

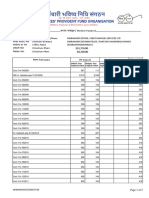

- Employees Provident Fund Organization: - Declaration FormDokument1 SeiteEmployees Provident Fund Organization: - Declaration FormRajeshNoch keine Bewertungen

- Marriage in Iowa Law - Complete ResultsDokument109 SeitenMarriage in Iowa Law - Complete ResultsDavid ShaferNoch keine Bewertungen

- Passbook PFDokument5 SeitenPassbook PFDarshan SarodeNoch keine Bewertungen

- Tax and Estate PlanningDokument32 SeitenTax and Estate PlanningVallabiNoch keine Bewertungen

- How To Fill Up - 2020 Blank Application Form - 12 May 2021Dokument3 SeitenHow To Fill Up - 2020 Blank Application Form - 12 May 2021Bai QianNoch keine Bewertungen

- Financial Ombudsman Claim DRN7791511Dokument12 SeitenFinancial Ombudsman Claim DRN7791511hyenadogNoch keine Bewertungen

- Policy Loans Including Foreclosure Revival Alteration Duplicate Policy RepositoryDokument23 SeitenPolicy Loans Including Foreclosure Revival Alteration Duplicate Policy Repositorykushal patilNoch keine Bewertungen

- SSGC Final UpdateDokument212 SeitenSSGC Final Updateemzeday100% (1)

- Letter-4 To Chairman From PFRDADokument2 SeitenLetter-4 To Chairman From PFRDAsantoshkumarNoch keine Bewertungen

- Deductions From Gross Total IncomeDokument91 SeitenDeductions From Gross Total Incomeheena4647Noch keine Bewertungen

- t4079 enDokument37 Seitent4079 enXolani LungaNoch keine Bewertungen

- GPF FinaDokument8 SeitenGPF Finateja ptoNoch keine Bewertungen

- Piyoosh BajoriaDokument17 SeitenPiyoosh BajoriaPunitValaNoch keine Bewertungen

- Issues in Financial Accounting 16th Edition Henderson Solutions ManualDokument27 SeitenIssues in Financial Accounting 16th Edition Henderson Solutions Manualcomplinofficialjasms100% (26)

- Stryker India PVT LTD: Payslip For The Month of April 2019Dokument4 SeitenStryker India PVT LTD: Payslip For The Month of April 2019Anonymous scxyMokpNoch keine Bewertungen

- Request For Withdrawal of GSIS Retirement Benefit Application FormatDokument1 SeiteRequest For Withdrawal of GSIS Retirement Benefit Application FormatLina Rhea0% (1)

- Seperation Agreement Family Law 11Dokument29 SeitenSeperation Agreement Family Law 11api-305856222100% (1)