Das könnte Ihnen auch gefallen

- 08 Interest Rates Exchange Rates and InflationDokument39 Seiten08 Interest Rates Exchange Rates and InflationEneida HaskoNoch keine Bewertungen

- Relationships Among Inflation, Interest Rates, and Exchange RatesDokument29 SeitenRelationships Among Inflation, Interest Rates, and Exchange RatesClaudia ChavarriaNoch keine Bewertungen

- Inflation Vs Interest RatesDokument12 SeitenInflation Vs Interest RatesanshuldceNoch keine Bewertungen

- International Financial Management: by Jeff MaduraDokument39 SeitenInternational Financial Management: by Jeff MaduraBe Like ComsianNoch keine Bewertungen

- Relationships Between Inflation, Interest Rates, and Exchange RatesDokument35 SeitenRelationships Between Inflation, Interest Rates, and Exchange RatesFahimHossainNitolNoch keine Bewertungen

- Relationships Among Inflation, Interest Rates and Exchange RatesDokument20 SeitenRelationships Among Inflation, Interest Rates and Exchange RatesHina ThakurNoch keine Bewertungen

- Chapter ObjectivesDokument20 SeitenChapter ObjectivesTajrian Ahmmed 1512588630Noch keine Bewertungen

- IFM - Chapter 6Dokument36 SeitenIFM - Chapter 6Đoàn Thị QuỳnhNoch keine Bewertungen

- Purchasing Power Prity and Internatinal FIsher EffectDokument37 SeitenPurchasing Power Prity and Internatinal FIsher EffectshreyaaamisraNoch keine Bewertungen

- Bekaert 2e SM Ch10Dokument11 SeitenBekaert 2e SM Ch10Xinyi Kimmy LiangNoch keine Bewertungen

- IFM - Chapter 6Dokument36 SeitenIFM - Chapter 6storkyddNoch keine Bewertungen

- Exchange RateDokument23 SeitenExchange Ratearchie_gangradeNoch keine Bewertungen

- International Parity Conditions: Reading: Chapter 4Dokument40 SeitenInternational Parity Conditions: Reading: Chapter 4Mahima AgrawalNoch keine Bewertungen

- CH 08Dokument20 SeitenCH 08PetersonNoch keine Bewertungen

- Multinational Business Finance 12th Edition Slides Chapter 07Dokument38 SeitenMultinational Business Finance 12th Edition Slides Chapter 07Alli Tobba100% (1)

- Link Between Money Supply and Interest Rates NotesDokument5 SeitenLink Between Money Supply and Interest Rates NotesHusseinNoch keine Bewertungen

- How inflation impacts exchange rates and interest ratesDokument18 SeitenHow inflation impacts exchange rates and interest ratesjahirul munnaNoch keine Bewertungen

- Relationships Among Inflation, Interest Rates, and Exchange RatesDokument15 SeitenRelationships Among Inflation, Interest Rates, and Exchange RatesFeriel El IlmiNoch keine Bewertungen

- International Parity Relations ExplainedDokument34 SeitenInternational Parity Relations ExplainedMotiram paudelNoch keine Bewertungen

- Foreign Exchange Market and Management of Foreign Exchange RiskDokument56 SeitenForeign Exchange Market and Management of Foreign Exchange RiskCedric ZvinavasheNoch keine Bewertungen

- International Finance Parity ConditionsDokument34 SeitenInternational Finance Parity ConditionsEdward Joseph A. RamosNoch keine Bewertungen

- PPT-4 Parity Conditions and Currency ForecastingDokument42 SeitenPPT-4 Parity Conditions and Currency ForecastingKamal KantNoch keine Bewertungen

- IFE Theory Test of Selected Industrialized CountriesDokument11 SeitenIFE Theory Test of Selected Industrialized CountriesSetyo Tyas JarwantoNoch keine Bewertungen

- Session 1bDokument29 SeitenSession 1bRohil SanilNoch keine Bewertungen

- Chapter 5 FinanceDokument18 SeitenChapter 5 FinancePia Eriksson0% (1)

- International Financial Management Canadian Canadian 3rd Edition Brean Solutions ManualDokument16 SeitenInternational Financial Management Canadian Canadian 3rd Edition Brean Solutions ManualAmberFranklinegrn100% (41)

- Theories of Foreign ExchangeDokument19 SeitenTheories of Foreign Exchangerockstarchandresh0% (1)

- Unit 4 International Parity Relation: SomtuDokument35 SeitenUnit 4 International Parity Relation: SomtuSabin ShresthaNoch keine Bewertungen

- International Finance Policy and Practice LevischDokument7 SeitenInternational Finance Policy and Practice LevischvikbitNoch keine Bewertungen

- 6 IpcDokument30 Seiten6 IpcSHOBANA96Noch keine Bewertungen

- Lec 4+5 _ chapter 7&9Dokument66 SeitenLec 4+5 _ chapter 7&9The flying peguine CụtNoch keine Bewertungen

- International Parity Relationship: Topic 4Dokument32 SeitenInternational Parity Relationship: Topic 4sittmoNoch keine Bewertungen

- Multinational Business Finance Eiteman 12th Edition Solutions ManualDokument5 SeitenMultinational Business Finance Eiteman 12th Edition Solutions ManualGeorgePalmerkqgd100% (29)

- Parity Conditions AND Currency ForecastingDokument39 SeitenParity Conditions AND Currency ForecastingSauryadeep DwivediNoch keine Bewertungen

- Ifm8e Im Ch08Dokument20 SeitenIfm8e Im Ch08jonathan1401Noch keine Bewertungen

- Exchange Rate TheoriesDokument28 SeitenExchange Rate TheoriesRavinder Singh AtwalNoch keine Bewertungen

- International Financial Management 3Dokument46 SeitenInternational Financial Management 3胡依然Noch keine Bewertungen

- Week 4 - Ex DeterminationDokument36 SeitenWeek 4 - Ex DeterminationwinfldNoch keine Bewertungen

- BX3031 - L2 - International Parity Conditions - TaggedDokument54 SeitenBX3031 - L2 - International Parity Conditions - TaggedSe SeNoch keine Bewertungen

- 3.1 International Parity ConditionsDokument41 Seiten3.1 International Parity ConditionsSanaFatimaNoch keine Bewertungen

- Parity Conditions and International Finance ForecastingDokument31 SeitenParity Conditions and International Finance ForecastingMahima AgrawalNoch keine Bewertungen

- 1 FMDokument31 Seiten1 FMSheryl KishanNoch keine Bewertungen

- 1.3. Exchange Rate Determination TheoriesDokument15 Seiten1.3. Exchange Rate Determination TheoriesDuong NguyenNoch keine Bewertungen

- Parity Conditions and Currency ForecastingDokument49 SeitenParity Conditions and Currency Forecastingsiti hasmahNoch keine Bewertungen

- Parity Conditions and Currency ForecastingDokument39 SeitenParity Conditions and Currency ForecastingZeeman28Noch keine Bewertungen

- Chapter 6 International Parity Relationships Suggested Answers and Solutions To End-Of-Chapter Questions and ProblemsDokument12 SeitenChapter 6 International Parity Relationships Suggested Answers and Solutions To End-Of-Chapter Questions and ProblemsRicky_Patel_9352Noch keine Bewertungen

- Does Beth's strategy support the IFEDokument11 SeitenDoes Beth's strategy support the IFEAnonymous Jf9PYY2E8Noch keine Bewertungen

- Purchasing Power ParityDokument25 SeitenPurchasing Power Parityspurtbd0% (1)

- 8 Purchasing Power ParityDokument28 Seiten8 Purchasing Power Parityjq7gsm6zb2Noch keine Bewertungen

- Exchange Rates, Interest Rates, and Inflation RatesDokument19 SeitenExchange Rates, Interest Rates, and Inflation RatesAnNa SouLsNoch keine Bewertungen

- 2.1exchange Rate Parity Currency ForecastingDokument30 Seiten2.1exchange Rate Parity Currency ForecastingFATIN NADJWA MAZLANNoch keine Bewertungen

- Multinational Business Finance: Fifteenth EditionDokument57 SeitenMultinational Business Finance: Fifteenth EditionTruc PhanNoch keine Bewertungen

- International Parity ConditionsDokument35 SeitenInternational Parity ConditionsRashique Ul LatifNoch keine Bewertungen

- International financial management: Parity ConditionsDokument47 SeitenInternational financial management: Parity ConditionsABHIJEET BHUNIA MBA 2021-23 (Delhi)Noch keine Bewertungen

- Intdiff Ltot Ldisrat Lusdisrat Lusprod LrexrDokument4 SeitenIntdiff Ltot Ldisrat Lusdisrat Lusprod LrexrsrieconomistNoch keine Bewertungen

- Session 2Dokument33 SeitenSession 2Soumik MutsuddiNoch keine Bewertungen

- Chapter 6 International Parity Relationships and Forecasting Foreign Exchange Rates Answers & Solutions To End-Of-Chapter Questions and ProblemsDokument16 SeitenChapter 6 International Parity Relationships and Forecasting Foreign Exchange Rates Answers & Solutions To End-Of-Chapter Questions and ProblemsZuka GabaidzeNoch keine Bewertungen

- The Euro - Dollar Exchange Rate & Pakistan Economy: Sulaiman D. MohammadDokument10 SeitenThe Euro - Dollar Exchange Rate & Pakistan Economy: Sulaiman D. Mohammadhassan48Noch keine Bewertungen

- Quantum Strategy II: Winning Strategies of Professional InvestmentVon EverandQuantum Strategy II: Winning Strategies of Professional InvestmentNoch keine Bewertungen

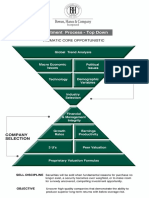

- Bowen Investment Process PDFDokument1 SeiteBowen Investment Process PDFbildyNoch keine Bewertungen

- Indonesia Employment Outlook and Salary Guide 2016Dokument36 SeitenIndonesia Employment Outlook and Salary Guide 2016eriwirandanaNoch keine Bewertungen

- Business Plan: " Pondok Organik "Dokument15 SeitenBusiness Plan: " Pondok Organik "bildyNoch keine Bewertungen

- Aivazian, Ge and Qiu - 2005Dokument15 SeitenAivazian, Ge and Qiu - 2005bildyNoch keine Bewertungen

- Market Basedmanagement 120210064429 Phpapp01Dokument32 SeitenMarket Basedmanagement 120210064429 Phpapp01bildyNoch keine Bewertungen

- BCA AR 2015 Eng PDFDokument602 SeitenBCA AR 2015 Eng PDFbildyNoch keine Bewertungen

- Usm-Icoss 2015 Proceedings PDFDokument664 SeitenUsm-Icoss 2015 Proceedings PDFbildyNoch keine Bewertungen

- Bowen Investment ProcessDokument1 SeiteBowen Investment ProcessbildyNoch keine Bewertungen

- Indonesia Employment Outlook and Salary Guide 2016Dokument36 SeitenIndonesia Employment Outlook and Salary Guide 2016eriwirandanaNoch keine Bewertungen

- Journal MarketingDokument11 SeitenJournal MarketingbildyNoch keine Bewertungen

- Building Brand Identity in Competitive Markets - A Conceptual ModelDokument9 SeitenBuilding Brand Identity in Competitive Markets - A Conceptual ModelAndré Pereira AzedoNoch keine Bewertungen

- Chap005 091214023954 Phpapp01 Internal AnalysisDokument31 SeitenChap005 091214023954 Phpapp01 Internal AnalysisbildyNoch keine Bewertungen

- Building Brand Identity in Competitive Markets - A Conceptual ModelDokument9 SeitenBuilding Brand Identity in Competitive Markets - A Conceptual ModelAndré Pereira AzedoNoch keine Bewertungen

- Aqua 2008-2009Dokument52 SeitenAqua 2008-2009Ryzki Nia November100% (1)

- Ctset Research Systems: This Is The Limited Version of The Factset Research Systems Company ProfileDokument12 SeitenCtset Research Systems: This Is The Limited Version of The Factset Research Systems Company ProfileSri HariniNoch keine Bewertungen

- Globalistation Mini Case StudiesDokument4 SeitenGlobalistation Mini Case StudiesFahad AwanNoch keine Bewertungen

- 15-Rural & Urban Development PDFDokument19 Seiten15-Rural & Urban Development PDFShradha SmoneeNoch keine Bewertungen

- 3 Major Financial Statements: Three Sections of The Statement of Cash FlowsDokument3 Seiten3 Major Financial Statements: Three Sections of The Statement of Cash FlowsPrecious Ivy FernandezNoch keine Bewertungen

- AFISCO v. CADokument2 SeitenAFISCO v. CASophiaFrancescaEspinosa100% (1)

- Income Tax - 2 AssignmentDokument4 SeitenIncome Tax - 2 AssignmentAnkit AgrawalNoch keine Bewertungen

- Forward MarketDokument18 SeitenForward MarketsachinremaNoch keine Bewertungen

- Meezan Bank Report FinalDokument61 SeitenMeezan Bank Report FinalMuhammad JamilNoch keine Bewertungen

- 7.0 Inventory ManagementDokument24 Seiten7.0 Inventory Managementrohanfyaz00Noch keine Bewertungen

- Lafarge AR 2017Dokument173 SeitenLafarge AR 2017Junwen LeeNoch keine Bewertungen

- IFC, Aldwych International, and Six Telecoms Partner To Develop 100 MW Wind Farm in Tanzania.Dokument2 SeitenIFC, Aldwych International, and Six Telecoms Partner To Develop 100 MW Wind Farm in Tanzania.dewjiblogNoch keine Bewertungen

- LEGASPI y NAVERA Vs People PDFDokument1 SeiteLEGASPI y NAVERA Vs People PDFethan pulveraNoch keine Bewertungen

- APTDokument7 SeitenAPTStefanNoch keine Bewertungen

- Chapt-3 Concepts of IncomeDokument4 SeitenChapt-3 Concepts of Incomehumnarvios50% (2)

- IV Sem MBA - TM - Strategic Management Model Paper 2013Dokument2 SeitenIV Sem MBA - TM - Strategic Management Model Paper 2013vikramvsuNoch keine Bewertungen

- Finbar Realty Investment AnalysisDokument20 SeitenFinbar Realty Investment AnalysisPrecious Santos CorpuzNoch keine Bewertungen

- RIghtNow TechnologiesDokument2 SeitenRIghtNow Technologiesuygh gNoch keine Bewertungen

- Corp Finance HBS Case Study: Debt Policy at UST IncDokument4 SeitenCorp Finance HBS Case Study: Debt Policy at UST IncTang LeiNoch keine Bewertungen

- Bombardier Annual Report 2004Dokument142 SeitenBombardier Annual Report 2004bombardierwatchNoch keine Bewertungen

- Green Brick Partners, Inc. GRBK - The Best Kept Secret On Wall StreetDokument3 SeitenGreen Brick Partners, Inc. GRBK - The Best Kept Secret On Wall StreetThe Focused Stock TraderNoch keine Bewertungen

- TVM Exercises in Cash Flow Mapping 1Dokument2 SeitenTVM Exercises in Cash Flow Mapping 1Cherry Anne TolentinoNoch keine Bewertungen

- P4-1: Consolidated Financials for Pea Corp and Subsidiary Sen CorpDokument21 SeitenP4-1: Consolidated Financials for Pea Corp and Subsidiary Sen Corpnancy tomanda100% (1)

- Data Stream Global Equity ManualDokument72 SeitenData Stream Global Equity Manualfariz888Noch keine Bewertungen

- Synopsis of Financial Analysis of Indian Overseas BankDokument8 SeitenSynopsis of Financial Analysis of Indian Overseas BankAmit MishraNoch keine Bewertungen

- Virtual Stock Trading Journal: in Partial Fulfilment of The RequirementsDokument13 SeitenVirtual Stock Trading Journal: in Partial Fulfilment of The RequirementsIrahq Yarte TorrejosNoch keine Bewertungen

- Review Jurnal Psikologi The LONG MEMORYDokument4 SeitenReview Jurnal Psikologi The LONG MEMORYDiah Dwi Putri IriantoNoch keine Bewertungen

- MicroCap Review Spring 2018Dokument110 SeitenMicroCap Review Spring 2018Planet MicroCap Review MagazineNoch keine Bewertungen

- Atul Ltd.Dokument4 SeitenAtul Ltd.Fast SwiftNoch keine Bewertungen

- Barclays - Improving VWAP Execution - Jan 2014Dokument10 SeitenBarclays - Improving VWAP Execution - Jan 2014tabbforumNoch keine Bewertungen

- TACTICAL FINANCING DECISIONSDokument24 SeitenTACTICAL FINANCING DECISIONSAccounting TeamNoch keine Bewertungen