Das könnte Ihnen auch gefallen

- THE DETERMINANTS OF PRICES OF NEWBUILDING IN THE VERY LARGE CRUDE CARRIERS (VLCC) SECTORVon EverandTHE DETERMINANTS OF PRICES OF NEWBUILDING IN THE VERY LARGE CRUDE CARRIERS (VLCC) SECTORNoch keine Bewertungen

- ORIGINAL (1) Cargo ManagementDokument61 SeitenORIGINAL (1) Cargo Managementlakshya211100% (1)

- Transport Cargo Econmics 01Dokument26 SeitenTransport Cargo Econmics 01LAMKADEMNoch keine Bewertungen

- Air CARGODokument74 SeitenAir CARGOFiliz MizrakNoch keine Bewertungen

- Global Dimensions of Supply Chains: Chandana HewegeDokument19 SeitenGlobal Dimensions of Supply Chains: Chandana Hewegenihar83Noch keine Bewertungen

- Transportation Engineering & Finance 2015-2016 (PART 6)Dokument22 SeitenTransportation Engineering & Finance 2015-2016 (PART 6)Allain DungoNoch keine Bewertungen

- Logistics SummaryDokument59 SeitenLogistics Summarysefa7703Noch keine Bewertungen

- Week 2 - Maritime Logistics PDFDokument42 SeitenWeek 2 - Maritime Logistics PDFHardy WidjajaNoch keine Bewertungen

- CHP 13Dokument17 SeitenCHP 13judefrancesNoch keine Bewertungen

- Introduction To The Airline Planning Process: MIT IcatDokument23 SeitenIntroduction To The Airline Planning Process: MIT IcatTalha HussainNoch keine Bewertungen

- Air Freight and Logistics Services: Fadila Kiso Abidin DeljaninDokument8 SeitenAir Freight and Logistics Services: Fadila Kiso Abidin DeljaninIonut VycentyuNoch keine Bewertungen

- LINCS TransportationOperations FullDokument196 SeitenLINCS TransportationOperations FullAlaVLatehNoch keine Bewertungen

- ECN Lecture 1 Economic EnvironmentDokument39 SeitenECN Lecture 1 Economic EnvironmentcarlosnavalmasterNoch keine Bewertungen

- Global Logistics ManagementDokument6 SeitenGlobal Logistics ManagementShiela Mae Clemente MasilangNoch keine Bewertungen

- W02 Transportmarketsindustries PDFDokument32 SeitenW02 Transportmarketsindustries PDF강철희Noch keine Bewertungen

- The Organization of The Shipping MarketDokument44 SeitenThe Organization of The Shipping MarketshannonNoch keine Bewertungen

- Transportation ServicesDokument50 SeitenTransportation ServicesNimish BhattNoch keine Bewertungen

- Aprendizaje 2: Evidencia 4: Resumen "¿Product Distribution: The Basics?" Neida Mendoza ZablaDokument6 SeitenAprendizaje 2: Evidencia 4: Resumen "¿Product Distribution: The Basics?" Neida Mendoza Zablaluis eduardo eduardoNoch keine Bewertungen

- Moving Freight Over The Road: Lecture ObjectivesDokument7 SeitenMoving Freight Over The Road: Lecture ObjectivesAlfath GhaniNoch keine Bewertungen

- Air Transportation: A Management PerspectiveDokument25 SeitenAir Transportation: A Management PerspectiveJavierNoch keine Bewertungen

- ManagementDokument108 SeitenManagementMidhul MineeshNoch keine Bewertungen

- Air TransportDokument40 SeitenAir TransportEuroline NtombouNoch keine Bewertungen

- Transportation ManagementDokument31 SeitenTransportation Managementpallab jyoti gogoiNoch keine Bewertungen

- Maritime LogisticsDokument22 SeitenMaritime LogisticsAnkita BediNoch keine Bewertungen

- Est May 2021Dokument5 SeitenEst May 2021Laiq Ur RahmanNoch keine Bewertungen

- Introduction To Marine TransportationDokument20 SeitenIntroduction To Marine TransportationNashphapaKanchanamuntana100% (2)

- Introduction To ShippingDokument33 SeitenIntroduction To Shippinganna anna100% (3)

- Container Industry Value ChainDokument14 SeitenContainer Industry Value ChainRasmus ArentsenNoch keine Bewertungen

- Moving Freight Over The Road: Lecture ObjectivesDokument8 SeitenMoving Freight Over The Road: Lecture ObjectivesSơn Nguyễn TrọngNoch keine Bewertungen

- Intermodal TransportDokument62 SeitenIntermodal TransportMert SabriNoch keine Bewertungen

- Transportation Services in International Market & Different Transport ModesDokument46 SeitenTransportation Services in International Market & Different Transport ModesGopesh VirmaniNoch keine Bewertungen

- Global Freight & Transportation Management SystemsDokument65 SeitenGlobal Freight & Transportation Management SystemsGabriele LorussoNoch keine Bewertungen

- 7 ReviewDokument2 Seiten7 ReviewFaqirullah SamimNoch keine Bewertungen

- Traffic Congestion: Transportation System Issues and ChallengesDokument6 SeitenTraffic Congestion: Transportation System Issues and ChallengesMatt Julius CorpuzNoch keine Bewertungen

- Lecture Solvay Business SchoolDokument37 SeitenLecture Solvay Business Schooljosephine delvigneNoch keine Bewertungen

- Chapter 6: Transport FundamentalsDokument40 SeitenChapter 6: Transport FundamentalssicrometricoNoch keine Bewertungen

- Moving Freight Over The Road: Lecture ObjectivesDokument4 SeitenMoving Freight Over The Road: Lecture Objectivessalma ezzouineNoch keine Bewertungen

- Est Examiners Report - Formatted Nov 21Dokument10 SeitenEst Examiners Report - Formatted Nov 21Laiq Ur RahmanNoch keine Bewertungen

- Liner Shipping: Introduction To Transportation and NavigationDokument17 SeitenLiner Shipping: Introduction To Transportation and NavigationSha Eem100% (1)

- Modes of TransportationDokument25 SeitenModes of TransportationRahul Saroha100% (1)

- Transportation - Supply ChainDokument55 SeitenTransportation - Supply Chainjaisi123Noch keine Bewertungen

- المحاضرة رقم 1Dokument25 Seitenالمحاضرة رقم 1Kholoud AtefNoch keine Bewertungen

- Modes of TranspoDokument6 SeitenModes of TranspoRegina SandovalNoch keine Bewertungen

- Chapter 6: Transport FundamentalsDokument40 SeitenChapter 6: Transport FundamentalsNashphapaKanchanamuntanaNoch keine Bewertungen

- Topic 4 - Bulk and Liner Service - Abril23Dokument58 SeitenTopic 4 - Bulk and Liner Service - Abril23Kawtar El Mouden DahbiNoch keine Bewertungen

- Logistics: Service CharacteristicsDokument6 SeitenLogistics: Service CharacteristicsMuhammad Usman KaimkhaniNoch keine Bewertungen

- Moving Freight Over The Road CourseraDokument7 SeitenMoving Freight Over The Road CourseraRonald FloresNoch keine Bewertungen

- Engleski Seminarski Air TransportationDokument11 SeitenEngleski Seminarski Air TransportationMarkoNoch keine Bewertungen

- Air Logistics: BY, Aarthi Ponnusamy Shanthi PriyadarshiniDokument11 SeitenAir Logistics: BY, Aarthi Ponnusamy Shanthi PriyadarshinitexcreaterNoch keine Bewertungen

- A Case Study On:: Utilisation of Container Movement-IRC: Import To ExportDokument22 SeitenA Case Study On:: Utilisation of Container Movement-IRC: Import To ExportCHAHATNoch keine Bewertungen

- Business Logistics Management: Marko BUDLERDokument27 SeitenBusiness Logistics Management: Marko BUDLEREconomics freakNoch keine Bewertungen

- Domestic U.S. & Global LogisticsDokument35 SeitenDomestic U.S. & Global LogisticsAshok Sharma100% (1)

- Topic 2 - Transportation Systems and Networks: A. B. C. DDokument32 SeitenTopic 2 - Transportation Systems and Networks: A. B. C. DArpan ShrivastavaNoch keine Bewertungen

- Air Cargo Logistics Mangement Project ReportDokument16 SeitenAir Cargo Logistics Mangement Project ReportMaaz MoidNoch keine Bewertungen

- Air Transportation Bien 2Dokument14 SeitenAir Transportation Bien 2Xavier LeroyNoch keine Bewertungen

- Imex Tham KhaoDokument11 SeitenImex Tham Khaohdanh0412Noch keine Bewertungen

- Transportation ModesDokument39 SeitenTransportation ModesChristine Anne PintacNoch keine Bewertungen

- Week 2 - Intermodal PortsDokument34 SeitenWeek 2 - Intermodal PortsEmile CornelissenNoch keine Bewertungen

- JPR Intermodal ITSDokument24 SeitenJPR Intermodal ITSCherry FeliciaNoch keine Bewertungen

- Free Trade Warehousing ZonesDokument20 SeitenFree Trade Warehousing Zonesarvindh92Noch keine Bewertungen

- Basics of SAP External Service ManagementDokument12 SeitenBasics of SAP External Service ManagementShane India RazaNoch keine Bewertungen

- Fact Sheet Customer - ReworkedDokument1 SeiteFact Sheet Customer - ReworkedSanthosh Chandran RNoch keine Bewertungen

- SAP Forecasting and Replenishment, Add-On For Fresh Products Administrator GuideDokument88 SeitenSAP Forecasting and Replenishment, Add-On For Fresh Products Administrator GuideSanthosh Chandran RNoch keine Bewertungen

- SAP Customer Activity Repository THE Omnichannel PlatformDokument67 SeitenSAP Customer Activity Repository THE Omnichannel PlatformSanthosh Chandran RNoch keine Bewertungen

- SAP Forecasting and Replenishment, Add-On For Fresh Products Application HelpDokument34 SeitenSAP Forecasting and Replenishment, Add-On For Fresh Products Application HelpSanthosh Chandran RNoch keine Bewertungen

- Schedule Agreement Release Processing: Overall ProcessDokument18 SeitenSchedule Agreement Release Processing: Overall Processpihua123Noch keine Bewertungen

- Satellite ComDokument54 SeitenSatellite ComSanthosh Chandran RNoch keine Bewertungen

- Fdocuments - in - Sap Forecasting Replenishment Sap Forecasting Replenishment 8 Years inDokument23 SeitenFdocuments - in - Sap Forecasting Replenishment Sap Forecasting Replenishment 8 Years inSanthosh Chandran RNoch keine Bewertungen

- Pareto Chart: Factors No. of Complaints PercentageDokument1 SeitePareto Chart: Factors No. of Complaints PercentageSanthosh Chandran RNoch keine Bewertungen

- QM SyllabusDokument2 SeitenQM SyllabusSanthosh Chandran RNoch keine Bewertungen

- 2-1 PerceptionDokument25 Seiten2-1 PerceptionSanthosh Chandran RNoch keine Bewertungen

- Logistics Industry: Make in IndiaDokument4 SeitenLogistics Industry: Make in IndiaSanthosh Chandran RNoch keine Bewertungen

- World's Largest Brewer: Global Beer ProductionDokument3 SeitenWorld's Largest Brewer: Global Beer ProductionSanthosh Chandran RNoch keine Bewertungen

- Qualcomm ProductsDokument18 SeitenQualcomm ProductsSanthosh Chandran RNoch keine Bewertungen

- Chapter 2Dokument8 SeitenChapter 2Santhosh Chandran RNoch keine Bewertungen

- Villupuram - CBSEDokument2 SeitenVillupuram - CBSESanthosh Chandran RNoch keine Bewertungen

- S.No DIA MM Dia D D MMDokument51 SeitenS.No DIA MM Dia D D MMSanthosh Chandran RNoch keine Bewertungen

- Unit 1Dokument92 SeitenUnit 1Santhosh Chandran RNoch keine Bewertungen

- Retail Sales and Softwares Used in Retail MarketingDokument12 SeitenRetail Sales and Softwares Used in Retail MarketingSanthosh Chandran RNoch keine Bewertungen

- Qualcomm ProductsDokument18 SeitenQualcomm ProductsSanthosh Chandran RNoch keine Bewertungen

- BUSINESS LAW - Important QuestionsDokument2 SeitenBUSINESS LAW - Important QuestionsSanthosh Chandran R100% (5)

- Treasure HuntDokument1 SeiteTreasure HuntSanthosh Chandran RNoch keine Bewertungen

- Chapter3 LodgingIndustryDokument17 SeitenChapter3 LodgingIndustrySanthosh Chandran RNoch keine Bewertungen

- CB SyllabusDokument2 SeitenCB SyllabusSanthosh Chandran RNoch keine Bewertungen

- Important Quenstions in Business EnvironmentDokument1 SeiteImportant Quenstions in Business EnvironmentSanthosh Chandran RNoch keine Bewertungen

- GARRIGOS Case Studies 24 Mars 2014Dokument9 SeitenGARRIGOS Case Studies 24 Mars 2014Santhosh Chandran RNoch keine Bewertungen

- Important Qns For Me: Part B-Analytic QuestionsDokument1 SeiteImportant Qns For Me: Part B-Analytic QuestionsSanthosh Chandran RNoch keine Bewertungen

- Case Study SRMDokument1 SeiteCase Study SRMSanthosh Chandran RNoch keine Bewertungen

- 04Dokument63 Seiten04Anchal ChhabraNoch keine Bewertungen

- BE - Case Study-The Hindu Nov 17, 2015Dokument2 SeitenBE - Case Study-The Hindu Nov 17, 2015Santhosh Chandran RNoch keine Bewertungen

- INCOTERMS 2010 Illustrated Guide PDFDokument28 SeitenINCOTERMS 2010 Illustrated Guide PDFmanoj262400/2Noch keine Bewertungen

- Built Up SectionsDokument2 SeitenBuilt Up Sectionslisan2053Noch keine Bewertungen

- Casting Process and Different Types of CastingsDokument31 SeitenCasting Process and Different Types of CastingsTejas KumarNoch keine Bewertungen

- Gati ProjectDokument45 SeitenGati ProjectHitesh RautNoch keine Bewertungen

- Mep SpecificationsDokument274 SeitenMep SpecificationsJoe Ps100% (6)

- Marine Insurance: Coverage Classes of Inland InsuranceDokument1 SeiteMarine Insurance: Coverage Classes of Inland InsuranceKit ChampNoch keine Bewertungen

- Normen Englisch Stand 09 2013Dokument9 SeitenNormen Englisch Stand 09 2013jmunjaNoch keine Bewertungen

- Comm ShippingDokument3 SeitenComm Shippingcapri33cornianNoch keine Bewertungen

- Flight International Nov 4-10, 2014Dokument56 SeitenFlight International Nov 4-10, 2014Brittany DunlapNoch keine Bewertungen

- Costa Concordia AccidentDokument40 SeitenCosta Concordia AccidentTrisha Venzon100% (1)

- Walmart CaseDokument2 SeitenWalmart CaseIliaskzNoch keine Bewertungen

- Imo MSC Circular 1222 - SVDRDokument6 SeitenImo MSC Circular 1222 - SVDRcaominhcuongNoch keine Bewertungen

- Aircraft at Pearl HarborDokument5 SeitenAircraft at Pearl HarborRichard Lund100% (1)

- Simpler Shipping Marks: Recommendation 15Dokument7 SeitenSimpler Shipping Marks: Recommendation 15Anup PanikerNoch keine Bewertungen

- TCS Smart Manager Case ContestDokument2 SeitenTCS Smart Manager Case ContestMangesh JoshiNoch keine Bewertungen

- FastenersDokument46 SeitenFastenerser_lalitgargNoch keine Bewertungen

- The Study of Li & Fung LimitedDokument19 SeitenThe Study of Li & Fung LimitedJames James ChowNoch keine Bewertungen

- Motor Insurance PSGDokument23 SeitenMotor Insurance PSGjeevanandamcNoch keine Bewertungen

- Good Sample of SOPEPDokument63 SeitenGood Sample of SOPEPGenghu Ye100% (3)

- 027-ITP For Pre - Cast Concrete PDFDokument11 Seiten027-ITP For Pre - Cast Concrete PDFKöksal Patan75% (4)

- Rehabilitacija - Okrugli Sto PrezentacijaDokument18 SeitenRehabilitacija - Okrugli Sto PrezentacijajovzareNoch keine Bewertungen

- Golden Palms BrochureDokument11 SeitenGolden Palms Brochurewawawa1Noch keine Bewertungen

- HOCHTIEF Projects - Werkschau - enDokument108 SeitenHOCHTIEF Projects - Werkschau - enffyuNoch keine Bewertungen

- Road CoastingDokument145 SeitenRoad CoastingBhavsar NilayNoch keine Bewertungen

- Introduction To Operations and Supply Chain Management Chapter 11Dokument5 SeitenIntroduction To Operations and Supply Chain Management Chapter 11dNoch keine Bewertungen

- Application Specification Guide: Section 17: Rubber LiningDokument7 SeitenApplication Specification Guide: Section 17: Rubber LiningEdgarDavidDiazCamposNoch keine Bewertungen

- Aircraft Accident ReportDokument9 SeitenAircraft Accident ReportChad ThomasNoch keine Bewertungen

- 5 Star Rated ACDokument3 Seiten5 Star Rated ACavr8784Noch keine Bewertungen

- Textile Industry InformationDokument6 SeitenTextile Industry InformationJasvinder SinghNoch keine Bewertungen

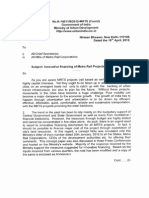

- Innovative Financing of Metro Rail ProjectsDokument8 SeitenInnovative Financing of Metro Rail ProjectsNivesh ChaudharyNoch keine Bewertungen