Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Sales ForecastDokument2 SeitenSales ForecastRafaelKwongNoch keine Bewertungen

- MOS FY09 Financial Data PDFDokument9 SeitenMOS FY09 Financial Data PDFRafaelKwongNoch keine Bewertungen

- Burger King-10K2009 PDFDokument128 SeitenBurger King-10K2009 PDFRafaelKwongNoch keine Bewertungen

- Ma - Capital Expenditure AnalysisDokument3 SeitenMa - Capital Expenditure AnalysisRafaelKwongNoch keine Bewertungen

- Cost Control and AnalysisDokument2 SeitenCost Control and AnalysisRafaelKwongNoch keine Bewertungen

- Pizza Hutt 2009annualreportDokument220 SeitenPizza Hutt 2009annualreportevojulzNoch keine Bewertungen

- Competitor AnalysisDokument4 SeitenCompetitor AnalysisRafaelKwong100% (1)

- MA DisadvantageDokument1 SeiteMA DisadvantageRafaelKwongNoch keine Bewertungen

- Case Study (Section 2.4)Dokument5 SeitenCase Study (Section 2.4)RafaelKwongNoch keine Bewertungen

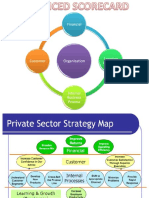

- Balanced Scorecard - Wells Fargo (BUSI0027D) PDFDokument12 SeitenBalanced Scorecard - Wells Fargo (BUSI0027D) PDFRafaelKwong50% (4)

- MADokument12 SeitenMARafaelKwongNoch keine Bewertungen

- Management Accounting - Project 1Dokument7 SeitenManagement Accounting - Project 1RafaelKwongNoch keine Bewertungen

- Management Accounting - Project 2Dokument3 SeitenManagement Accounting - Project 2RafaelKwongNoch keine Bewertungen

- Advantages of Balanced ScorecardDokument1 SeiteAdvantages of Balanced ScorecardRafaelKwongNoch keine Bewertungen

- IS PictureDokument1 SeiteIS PictureRafaelKwongNoch keine Bewertungen

- MA Project 2 - McDonaldsDokument11 SeitenMA Project 2 - McDonaldsRafaelKwongNoch keine Bewertungen

- McDonald's Advertising and Pricing IIDokument2 SeitenMcDonald's Advertising and Pricing IIRafaelKwongNoch keine Bewertungen

- Inventory Management of McDonald'sDokument2 SeitenInventory Management of McDonald'sRafaelKwongNoch keine Bewertungen

- Cash BudgetDokument1 SeiteCash BudgetRafaelKwongNoch keine Bewertungen

- Management Accounting Project 2 - D6 (Finalized) PDFDokument20 SeitenManagement Accounting Project 2 - D6 (Finalized) PDFRafaelKwongNoch keine Bewertungen

- Income Statement NeatDokument2 SeitenIncome Statement NeatRafaelKwongNoch keine Bewertungen

- Budgeted Balance SheetDokument2 SeitenBudgeted Balance SheetRafaelKwongNoch keine Bewertungen

- Mini Interview Instruction SheetDokument2 SeitenMini Interview Instruction SheetRafaelKwongNoch keine Bewertungen

- Taxation Q21 Handout v3 PDFDokument11 SeitenTaxation Q21 Handout v3 PDFRafaelKwongNoch keine Bewertungen

- Management Accounting - Project 2Dokument3 SeitenManagement Accounting - Project 2RafaelKwongNoch keine Bewertungen

- 1011 Group Project AssignmentDokument1 Seite1011 Group Project AssignmentRafaelKwongNoch keine Bewertungen

- Answers For Question 2Dokument1 SeiteAnswers For Question 2RafaelKwongNoch keine Bewertungen

- Chapter 16 LeadershipDokument18 SeitenChapter 16 LeadershipRafaelKwongNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Gender Champions GuidelinesDokument9 SeitenGender Champions GuidelinesJuhi NeogiNoch keine Bewertungen

- Solution Focused Counseling With Nvoluntary ClientsDokument13 SeitenSolution Focused Counseling With Nvoluntary ClientsJuanaNoch keine Bewertungen

- Rotational Hex Designs LessonDokument6 SeitenRotational Hex Designs Lessonapi-373975702Noch keine Bewertungen

- Critical Pedagogy in Higher Education: Insights From English Language TeachersDokument243 SeitenCritical Pedagogy in Higher Education: Insights From English Language TeachersMilaziNoch keine Bewertungen

- Updated All College List With Course DetailssDokument3 SeitenUpdated All College List With Course DetailssfhdxxNoch keine Bewertungen

- Hypermedia Lesson PlanDokument4 SeitenHypermedia Lesson PlanJeanne SearfoorceNoch keine Bewertungen

- Unit 14 - Strategic Supply Chain Management and LogisticsDokument8 SeitenUnit 14 - Strategic Supply Chain Management and Logisticsanis_kasmani98800% (1)

- ASNT UT Level 3 Results (2018 2021)Dokument25 SeitenASNT UT Level 3 Results (2018 2021)wintwah.myantestNoch keine Bewertungen

- Phil 104, Wednesday, December 1, 2010 Stevenson, "The Emotive Meaning of Ethical Terms" The AimDokument3 SeitenPhil 104, Wednesday, December 1, 2010 Stevenson, "The Emotive Meaning of Ethical Terms" The Aimatls23Noch keine Bewertungen

- Chapter 1Dokument2 SeitenChapter 1Inigo BogiasNoch keine Bewertungen

- Aue@chem - Ucsb.edu: Instructor Code For Aue's 109A: MCAUE06615)Dokument4 SeitenAue@chem - Ucsb.edu: Instructor Code For Aue's 109A: MCAUE06615)Allison ChangNoch keine Bewertungen

- PromoDokument40 SeitenPromoEno PraiseNoch keine Bewertungen

- InfluenceDokument3 SeitenInfluenceLucky YohNoch keine Bewertungen

- Beginner FrenchDokument252 SeitenBeginner Frenchpeppermintpatty1951100% (15)

- Fractions - 3rd Grade Learning Support - Madalyn EquiDokument5 SeitenFractions - 3rd Grade Learning Support - Madalyn Equiapi-549445196Noch keine Bewertungen

- Dissertation On Education in IndiaDokument8 SeitenDissertation On Education in IndiaManchester100% (1)

- The BSK Voice, Vol. 9, No. 1 (Spring 2012)Dokument6 SeitenThe BSK Voice, Vol. 9, No. 1 (Spring 2012)Baptist Seminary of KentuckyNoch keine Bewertungen

- Nikki Chwatt ResumeDokument1 SeiteNikki Chwatt ResumeNikki ChwattNoch keine Bewertungen

- UPS 04 (BI) - Application For Appointment On Contract Basis For Academic StaffDokument6 SeitenUPS 04 (BI) - Application For Appointment On Contract Basis For Academic Staffkhairul danialNoch keine Bewertungen

- Nursing Final DraftDokument2 SeitenNursing Final Draftapi-272895943Noch keine Bewertungen

- HW 0Dokument1 SeiteHW 0Kumar RajputNoch keine Bewertungen

- Daily Lesson Log Template SampleDokument5 SeitenDaily Lesson Log Template SampleNonie Beth CervantesNoch keine Bewertungen

- The Rcem ApproachDokument3 SeitenThe Rcem ApproachMANICA92% (12)

- RPH (Body Coordination)Dokument115 SeitenRPH (Body Coordination)Mohd Aidil UbaidillahNoch keine Bewertungen

- Stop Asking Me My MajorDokument5 SeitenStop Asking Me My MajorPandita Gamer27YTNoch keine Bewertungen

- Building With Commercial Spaces at Nalsian, Calasiao, Pangasinan"Dokument3 SeitenBuilding With Commercial Spaces at Nalsian, Calasiao, Pangasinan"Mark DotoNoch keine Bewertungen

- Semi-Detailed Lesson PlanDokument3 SeitenSemi-Detailed Lesson Planedrine100% (1)

- Test Bank For Social Development 2nd Edition by Clarke Stewart ParkeDokument24 SeitenTest Bank For Social Development 2nd Edition by Clarke Stewart Parkekellywalkerdasbgefrwx100% (41)

- Bengkel Penulisan Clo Dan SLT Serta Kemaskini SilibusDokument128 SeitenBengkel Penulisan Clo Dan SLT Serta Kemaskini SilibusAbdul Rasman Abdul Rashid0% (1)

- Betty Neumann System TheoryDokument8 SeitenBetty Neumann System TheoryAnnapurna DangetiNoch keine Bewertungen