Das könnte Ihnen auch gefallen

- Manicure Marketing StrategyDokument11 SeitenManicure Marketing StrategyElijah ElijahNoch keine Bewertungen

- Letter of Award....Dokument3 SeitenLetter of Award....lalith ruberu100% (3)

- JASA Mar Apr 2012 IssueDokument104 SeitenJASA Mar Apr 2012 IssueandrewduttaNoch keine Bewertungen

- Costco Marketing PresentationDokument11 SeitenCostco Marketing PresentationRuma BhowmikNoch keine Bewertungen

- Journal For Advancement of Stellar AstrologyDokument95 SeitenJournal For Advancement of Stellar Astrologyandrew_dutta67% (3)

- Summary: The Essential CFODokument9 SeitenSummary: The Essential CFOLeoneSalomNoch keine Bewertungen

- JASA May-Jun 2012 IssueDokument106 SeitenJASA May-Jun 2012 IssueandrewduttaNoch keine Bewertungen

- "Simple Rules of 4 Step Theory": Rule 1Dokument5 Seiten"Simple Rules of 4 Step Theory": Rule 1SaptarishisAstrology100% (2)

- A Study of Stock Index and Factors Affecting Share PricesDokument73 SeitenA Study of Stock Index and Factors Affecting Share PricesPraveen KambleNoch keine Bewertungen

- Nov-Dec 2011 Issue of JASADokument0 SeitenNov-Dec 2011 Issue of JASAProfessorAsim Kumar MishraNoch keine Bewertungen

- Applied Econometrics: A Simple IntroductionVon EverandApplied Econometrics: A Simple IntroductionBewertung: 5 von 5 Sternen5/5 (2)

- Agricultural MarketingDokument65 SeitenAgricultural MarketingOliver TalipNoch keine Bewertungen

- JASA Oct-Dec 2013 IssueDokument116 SeitenJASA Oct-Dec 2013 Issuekumarkumar123Noch keine Bewertungen

- A Study On Analysis of Equity Share Price Behavior ofDokument8 SeitenA Study On Analysis of Equity Share Price Behavior ofSagar Mundada100% (2)

- Profiting From Technical AnalysisDokument20 SeitenProfiting From Technical Analysissuhasking100% (1)

- An Analysis of Market Efficiency in Sectoral Indices: A Study With A Special Reference To Bombay Stock Exchange in IndiaDokument8 SeitenAn Analysis of Market Efficiency in Sectoral Indices: A Study With A Special Reference To Bombay Stock Exchange in IndiaRatish CdnvNoch keine Bewertungen

- AStudyof Efficiencyofthe Indian Stock MarketDokument9 SeitenAStudyof Efficiencyofthe Indian Stock MarketAkanksha GoelNoch keine Bewertungen

- SSRN Id2621942Dokument15 SeitenSSRN Id2621942Arun KCNoch keine Bewertungen

- 20-MF-17 Weak Form Efficiency Study of Indian Stock MarketDokument8 Seiten20-MF-17 Weak Form Efficiency Study of Indian Stock MarketNachiket ParabNoch keine Bewertungen

- 18 BM1407-037Dokument5 Seiten18 BM1407-037Eby Johnson C.Noch keine Bewertungen

- Volatility in The Indian Stock Market: A Case of Individual SecuritiesDokument12 SeitenVolatility in The Indian Stock Market: A Case of Individual SecuritiesKarthik KarthikNoch keine Bewertungen

- Weak Form Efficiency in Indian Stock Markets PDFDokument9 SeitenWeak Form Efficiency in Indian Stock Markets PDFDeepender DeolNoch keine Bewertungen

- Testing Weak Form Efficiency For Indian Derivatives MarketDokument4 SeitenTesting Weak Form Efficiency For Indian Derivatives MarketVasantha NaikNoch keine Bewertungen

- Determinants of Equity Share Prices in IndiaDokument10 SeitenDeterminants of Equity Share Prices in IndiaMuhammad RezaNoch keine Bewertungen

- Importance of Technical and Fundamental Analysis and Other Strategic Factors in The Indian Stock MarketDokument39 SeitenImportance of Technical and Fundamental Analysis and Other Strategic Factors in The Indian Stock MarketArkajeet PaulNoch keine Bewertungen

- 5 Journals in One FileDokument7 Seiten5 Journals in One FileSunita MauryaNoch keine Bewertungen

- Market Timing Performance of The Open enDokument10 SeitenMarket Timing Performance of The Open enAli NadafNoch keine Bewertungen

- Hypothesis Testing ExampleDokument11 SeitenHypothesis Testing ExampleAayush SisodiaNoch keine Bewertungen

- Blackbook ValuationDokument63 SeitenBlackbook Valuationsmit sangoiNoch keine Bewertungen

- Tests of Technical Analysis in India: Sanjay Sehgal and Meenakshi GuptaDokument14 SeitenTests of Technical Analysis in India: Sanjay Sehgal and Meenakshi Guptashailendra_nrNoch keine Bewertungen

- Micro Economic Determinants Changed Final AceptedDokument22 SeitenMicro Economic Determinants Changed Final AceptedujstudyNoch keine Bewertungen

- SSRN Id1803922 Paper DipDokument20 SeitenSSRN Id1803922 Paper DipKamal SinghNoch keine Bewertungen

- A Study of The Weak Form of Market Efficiency in India With Special Reference To Realty SectorDokument7 SeitenA Study of The Weak Form of Market Efficiency in India With Special Reference To Realty SectorsandypkapoorNoch keine Bewertungen

- Technical Analysis of Indian Pharma CompaniesDokument3 SeitenTechnical Analysis of Indian Pharma CompaniesRaj KumarNoch keine Bewertungen

- A Study On Impact of Corporate Action On Stock Price at L&TDokument58 SeitenA Study On Impact of Corporate Action On Stock Price at L&TRajesh BathulaNoch keine Bewertungen

- SDM - Event Study On Corporate ActionsDokument28 SeitenSDM - Event Study On Corporate Actionsvinay MohanNoch keine Bewertungen

- Review of LiteratureDokument20 SeitenReview of LiteratureHarsh BhanushaliNoch keine Bewertungen

- Momentum TradingDokument2 SeitenMomentum TradingAaryan GuptaNoch keine Bewertungen

- A Study On The Performance of Initial Public Sarliya (1) 111Dokument14 SeitenA Study On The Performance of Initial Public Sarliya (1) 111sarliyaNoch keine Bewertungen

- Capital Market Research Is An Essential Activity For Companies Because It Enables Them ToDokument5 SeitenCapital Market Research Is An Essential Activity For Companies Because It Enables Them Tonikita sharmaNoch keine Bewertungen

- Chapter-1: Page - 1Dokument13 SeitenChapter-1: Page - 1Dhaval MajithiaNoch keine Bewertungen

- Manorama, Rajesh Joshi, Amardeep Singh, Jairaghuveer BawaDokument13 SeitenManorama, Rajesh Joshi, Amardeep Singh, Jairaghuveer BawaHimanshu Raj JainNoch keine Bewertungen

- Analysis of Corporate Actions and Market Efficiency in IndiaDokument16 SeitenAnalysis of Corporate Actions and Market Efficiency in IndiaAzim BawaNoch keine Bewertungen

- Gilani Et Al 2014 PDFDokument9 SeitenGilani Et Al 2014 PDFmithaNoch keine Bewertungen

- Seasonality Indian MarketDokument15 SeitenSeasonality Indian MarketRENJiiiNoch keine Bewertungen

- Ijair Volume 6 Issue 2 Xxii Aprilgjune 2019 143 151Dokument10 SeitenIjair Volume 6 Issue 2 Xxii Aprilgjune 2019 143 151Rachmawati -Noch keine Bewertungen

- 09 - Chapter 3 PDFDokument42 Seiten09 - Chapter 3 PDFZahid HussainNoch keine Bewertungen

- p716 FinalDokument5 Seitenp716 FinalTariq AzizNoch keine Bewertungen

- Modelling The Nigerian Stock Market (Shares) Evidence From Time Series AnalysisDokument12 SeitenModelling The Nigerian Stock Market (Shares) Evidence From Time Series AnalysistheijesNoch keine Bewertungen

- 09 - Chapter 2Dokument30 Seiten09 - Chapter 2aswinecebeNoch keine Bewertungen

- A Study of Individual Investors in The Capital Market in Kerala, Chap-2Dokument22 SeitenA Study of Individual Investors in The Capital Market in Kerala, Chap-2jayarawmanrNoch keine Bewertungen

- Tài Liệu Không Có Tiêu ĐềDokument18 SeitenTài Liệu Không Có Tiêu ĐềKhánh LinhNoch keine Bewertungen

- A Comparative Analysis of Mutual Fund Schemes in IndiaDokument13 SeitenA Comparative Analysis of Mutual Fund Schemes in IndiagomsinghNoch keine Bewertungen

- Prosiding David Sukardi-OkDokument17 SeitenProsiding David Sukardi-OkReny Prama LestariNoch keine Bewertungen

- Event Study Pengumuman Laba Terhadap Reaksi Pasar ModalDokument24 SeitenEvent Study Pengumuman Laba Terhadap Reaksi Pasar ModalRatih NatawiraniNoch keine Bewertungen

- Truba College of Engineering 2Dokument44 SeitenTruba College of Engineering 2Prashant GoleNoch keine Bewertungen

- Hiren M Maniar, DR - Rajesh Bhatt, DR - Dharmesh M ManiyarDokument28 SeitenHiren M Maniar, DR - Rajesh Bhatt, DR - Dharmesh M Maniyarguptapunit03Noch keine Bewertungen

- Performance of 9904452455Dokument10 SeitenPerformance of 9904452455Pradip JaniNoch keine Bewertungen

- Delhi Business Review X VolDokument7 SeitenDelhi Business Review X VolMohit VanawatNoch keine Bewertungen

- Pavan Project On Equity Derivatives 2222222222222222222222222222Dokument55 SeitenPavan Project On Equity Derivatives 2222222222222222222222222222ravan vlogsNoch keine Bewertungen

- 10 1 1 16 658 PDFDokument11 Seiten10 1 1 16 658 PDFHM SyedNoch keine Bewertungen

- The Market For Long Term Securities Like Bonds, Equity Stocks andDokument76 SeitenThe Market For Long Term Securities Like Bonds, Equity Stocks andRohit AggarwalNoch keine Bewertungen

- Submitted by Sukla Paul Roll No: 07, 2Nd Year Soms, Iiest, ShibpurDokument26 SeitenSubmitted by Sukla Paul Roll No: 07, 2Nd Year Soms, Iiest, ShibpurDarshiNoch keine Bewertungen

- On Going CP 1Dokument27 SeitenOn Going CP 1Anonymous eveICfNoch keine Bewertungen

- Research MethodologyDokument11 SeitenResearch MethodologyBalram SoniNoch keine Bewertungen

- The Effects of Rupee Dollar Exchange Rate Parity On The Indian Stock MarketDokument11 SeitenThe Effects of Rupee Dollar Exchange Rate Parity On The Indian Stock MarketAssociation for Pure and Applied ResearchesNoch keine Bewertungen

- Predictability of Stock Returns Using Financial Ratios: Empirical Evidence From Colombo Stock ExchangeDokument13 SeitenPredictability of Stock Returns Using Financial Ratios: Empirical Evidence From Colombo Stock ExchangeAngella TiosannaNoch keine Bewertungen

- Complete Final NanduDokument76 SeitenComplete Final Nandupandukrish0143Noch keine Bewertungen

- Emerging Markets Trading StrategiesDokument19 SeitenEmerging Markets Trading StrategiesjaycamerNoch keine Bewertungen

- Group 2 Campbell Corpor DebtDokument9 SeitenGroup 2 Campbell Corpor DebtProfessorAsim Kumar MishraNoch keine Bewertungen

- Post Merger ManagementDokument6 SeitenPost Merger ManagementProfessorAsim Kumar MishraNoch keine Bewertungen

- Destin Brass Case SolDokument2 SeitenDestin Brass Case SolProfessorAsim Kumar MishraNoch keine Bewertungen

- Bill FincgDokument16 SeitenBill FincgProfessorAsim Kumar MishraNoch keine Bewertungen

- KNR Construction - Book BuildingDokument11 SeitenKNR Construction - Book BuildingProfessorAsim Kumar MishraNoch keine Bewertungen

- Divid PolicyDokument15 SeitenDivid PolicyProfessorAsim Kumar Mishra100% (1)

- Bill DiscountingDokument69 SeitenBill DiscountingDhanesh BabarNoch keine Bewertungen

- Stock MKT Pred CHRTDokument2 SeitenStock MKT Pred CHRTProfessorAsim Kumar MishraNoch keine Bewertungen

- IBFS Case - Rights Issue - Godrej Consumers (Group 1 - WMP13) - V3.0Dokument8 SeitenIBFS Case - Rights Issue - Godrej Consumers (Group 1 - WMP13) - V3.0ProfessorAsim Kumar MishraNoch keine Bewertungen

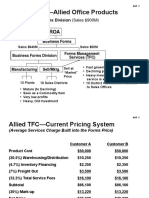

- ABC Costing Allied Office ProductsDokument13 SeitenABC Costing Allied Office ProductsProfessorAsim Kumar Mishra100% (1)

- Analysis of Continuing ValueDokument8 SeitenAnalysis of Continuing ValueProfessorAsim Kumar MishraNoch keine Bewertungen

- DIP GuidelinesDokument11 SeitenDIP GuidelinesProfessorAsim Kumar MishraNoch keine Bewertungen

- Short Term Sources of FinanceDokument18 SeitenShort Term Sources of FinanceJithin Krishnan100% (1)

- KP Reader 3 Pg. 314Dokument5 SeitenKP Reader 3 Pg. 314ProfessorAsim Kumar MishraNoch keine Bewertungen

- Horary and Sublord in RetroDokument1 SeiteHorary and Sublord in RetroProfessorAsim Kumar MishraNoch keine Bewertungen

- ARS AllRapidShare 3.0Dokument1 SeiteARS AllRapidShare 3.0ProfessorAsim Kumar MishraNoch keine Bewertungen

- 12 Houses SignifyDokument7 Seiten12 Houses SignifyProfessorAsim Kumar MishraNoch keine Bewertungen

- 12 Signs of The ZodiacDokument9 Seiten12 Signs of The ZodiacProfessorAsim Kumar MishraNoch keine Bewertungen

- TMP For AstroDokument4 SeitenTMP For AstroProfessorAsim Kumar MishraNoch keine Bewertungen

- KP Reader 3 Pg. 160Dokument5 SeitenKP Reader 3 Pg. 160ProfessorAsim Kumar MishraNoch keine Bewertungen

- 8th House in MarriageDokument3 Seiten8th House in MarriageProfessorAsim Kumar MishraNoch keine Bewertungen

- Nak ChintaDokument5 SeitenNak ChintaProfessorAsim Kumar MishraNoch keine Bewertungen

- Jasa Sep-Oct 2011 - 1Dokument0 SeitenJasa Sep-Oct 2011 - 1ProfessorAsim Kumar MishraNoch keine Bewertungen

- Soudek - Aristotles Theory of Exchange PDFDokument32 SeitenSoudek - Aristotles Theory of Exchange PDFFlorencia Zayas YogaNoch keine Bewertungen

- Brokerage CalculatorDokument5 SeitenBrokerage CalculatorJay KewatNoch keine Bewertungen

- Price List: Cables With HTR (High Temperature Resistance)Dokument2 SeitenPrice List: Cables With HTR (High Temperature Resistance)Amit MandalNoch keine Bewertungen

- CGQS BrochureDokument1 SeiteCGQS BrochureCathal GuineyNoch keine Bewertungen

- Determinants of Demand PDFDokument20 SeitenDeterminants of Demand PDFKhamisi MwanzaraNoch keine Bewertungen

- Fin333 Secondmt04w Sample QuestionsDokument10 SeitenFin333 Secondmt04w Sample QuestionsSara NasNoch keine Bewertungen

- Islamic Economic SystemDokument5 SeitenIslamic Economic Systemhelperforeu100% (1)

- DB - Chemical DatabookDokument51 SeitenDB - Chemical Databooksiput_lembekNoch keine Bewertungen

- Eng 329 Team1Dokument11 SeitenEng 329 Team1b21fa1676Noch keine Bewertungen

- Unravelling The Indian Consumer - Web PDFDokument31 SeitenUnravelling The Indian Consumer - Web PDFMUNning BuddhaNoch keine Bewertungen

- Corporate-Level Strategy:: What Business Are We In?Dokument5 SeitenCorporate-Level Strategy:: What Business Are We In?Chitral PatelNoch keine Bewertungen

- Optus Loop: Standard Pricing TableDokument12 SeitenOptus Loop: Standard Pricing TableDave BennettsNoch keine Bewertungen

- Practice Exam - Part 3: Multiple ChoiceDokument4 SeitenPractice Exam - Part 3: Multiple ChoiceAzeem TalibNoch keine Bewertungen

- Mitesh Patel - The Angry Young Man of Options TradingDokument18 SeitenMitesh Patel - The Angry Young Man of Options Tradingbarkha rani100% (1)

- History of IFRS 7: Reclassification of Financial Assets (Amendments To IAS 39 and IFRS 7) IssuedDokument5 SeitenHistory of IFRS 7: Reclassification of Financial Assets (Amendments To IAS 39 and IFRS 7) IssuedTin BatacNoch keine Bewertungen

- CA Chapter 15-03-05Dokument14 SeitenCA Chapter 15-03-05D DNoch keine Bewertungen

- Impact of Crude Oil Price On Indian EconomyDokument5 SeitenImpact of Crude Oil Price On Indian EconomySri LakshmiNoch keine Bewertungen

- Lucky Cement Report3Dokument21 SeitenLucky Cement Report3sidrah_farooq2878100% (1)

- Toyota CamryDokument1 SeiteToyota CamryJamal100% (1)

- Xplornet Pre-Installation Info For United TVDokument5 SeitenXplornet Pre-Installation Info For United TVPam DavidsonNoch keine Bewertungen

- Rent Income: Dividend Income Other IncomeDokument1 SeiteRent Income: Dividend Income Other IncomeLhorene Hope DueñasNoch keine Bewertungen

- Current Affairs Weekly Content PDF February 2023 3rd Week by AffairsCloudDokument27 SeitenCurrent Affairs Weekly Content PDF February 2023 3rd Week by AffairsClouddatwbfaqsjvmsNoch keine Bewertungen

- NDFDokument7 SeitenNDFbaldfishNoch keine Bewertungen

- Trader's Playbook - HOMEDokument3 SeitenTrader's Playbook - HOMEConstantino L. Ramirez IIINoch keine Bewertungen

- SOLAR PV Panel Contract For Newport Housing Trust: Strictly Private and ConfidentialDokument59 SeitenSOLAR PV Panel Contract For Newport Housing Trust: Strictly Private and ConfidentialjogiyajeeNoch keine Bewertungen