Das könnte Ihnen auch gefallen

- 1-8 GST - GST Payable or ITC AvalDokument2 Seiten1-8 GST - GST Payable or ITC Avaloddsey0713Noch keine Bewertungen

- Does FBT Apply?: Div 13 ExclusionsDokument1 SeiteDoes FBT Apply?: Div 13 Exclusionsoddsey0713Noch keine Bewertungen

- 3-3 Company LossesDokument1 Seite3-3 Company Lossesoddsey0713Noch keine Bewertungen

- 4-3 Part IVA General AntiAvoidanceDokument1 Seite4-3 Part IVA General AntiAvoidanceoddsey0713Noch keine Bewertungen

- 2-3 Capital AllowancesDokument1 Seite2-3 Capital Allowancesoddsey0713Noch keine Bewertungen

- 3-3 Franking AccountDokument1 Seite3-3 Franking Accountoddsey0713Noch keine Bewertungen

- 2-4,5 Capital WorksDokument1 Seite2-4,5 Capital Worksoddsey0713Noch keine Bewertungen

- T6 Chapter 5 Solutions To The Essential ActivitiesDokument12 SeitenT6 Chapter 5 Solutions To The Essential Activitiesoddsey0713Noch keine Bewertungen

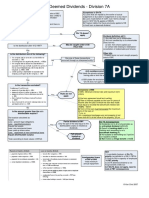

- 3-3 Div 7A Deemed Divs - VLDokument1 Seite3-3 Div 7A Deemed Divs - VLoddsey0713Noch keine Bewertungen

- Case Summaries 1 193Dokument54 SeitenCase Summaries 1 193oddsey0713100% (1)

- T7 Chapter 6 Solutions To The Essential ActivitiesDokument26 SeitenT7 Chapter 6 Solutions To The Essential Activitiesoddsey0713Noch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- STP Analysis: Complete MBA CourseDokument6 SeitenSTP Analysis: Complete MBA CourseBilly ButcherNoch keine Bewertungen

- EW Ch3 Case Audit Planning MemoDokument7 SeitenEW Ch3 Case Audit Planning MemoNursalihah Binti Md NorNoch keine Bewertungen

- Shivika SIP InterimDokument19 SeitenShivika SIP InterimShivika AroraNoch keine Bewertungen

- Principles of Management Assignment MBA Annamalai University First Year AssignmentDokument22 SeitenPrinciples of Management Assignment MBA Annamalai University First Year Assignmentamitinasia25% (4)

- Nurul Izmah BT Ab Rahim: Rawang, SelangorDokument3 SeitenNurul Izmah BT Ab Rahim: Rawang, SelangorNurul RahimNoch keine Bewertungen

- Lecture 2 - Development of ESG Strategies-2Dokument48 SeitenLecture 2 - Development of ESG Strategies-2PGNoch keine Bewertungen

- LaporanmagangDokument46 SeitenLaporanmagangNadya RizkitaNoch keine Bewertungen

- Syllabus Semester 4 HRMDokument5 SeitenSyllabus Semester 4 HRMJeyNoch keine Bewertungen

- Ecommerce NotesDokument8 SeitenEcommerce NotesmzumziNoch keine Bewertungen

- R M D C: ISK Anagement Epartment HarterDokument15 SeitenR M D C: ISK Anagement Epartment HarterPATRICK MUTINDANoch keine Bewertungen

- FOSTIIMA Prospectus 2012Dokument22 SeitenFOSTIIMA Prospectus 2012Sangita SrivastavaNoch keine Bewertungen

- ACCT3109 Assignment Discussion Q Ch6Dokument2 SeitenACCT3109 Assignment Discussion Q Ch6Ailsa MayNoch keine Bewertungen

- Chapter 5Dokument31 SeitenChapter 5cherryyllNoch keine Bewertungen

- BRC Global Standard For Packaging and Packaging MaterialsDokument5 SeitenBRC Global Standard For Packaging and Packaging MaterialsCassilda CarvalhoNoch keine Bewertungen

- Gamp5 For Basic Training PDFDokument47 SeitenGamp5 For Basic Training PDFVimlesh Kumar PandeyNoch keine Bewertungen

- Change Management 2010Dokument5 SeitenChange Management 2010Mrinal MehtaNoch keine Bewertungen

- ABC Company Sample Data ReportDokument11 SeitenABC Company Sample Data Reportjessa salamanqueNoch keine Bewertungen

- MBAAR AssignmentDokument43 SeitenMBAAR Assignmentkidszalor1412100% (3)

- StraMa Worksheet 12 Internal Factor Evaluation MatrixDokument6 SeitenStraMa Worksheet 12 Internal Factor Evaluation MatrixDiazmean SoteloNoch keine Bewertungen

- Leadership Final Material.Dokument26 SeitenLeadership Final Material.Peña TahirisNoch keine Bewertungen

- BEC Mnemonics, Formulas, and Condensed ITDokument5 SeitenBEC Mnemonics, Formulas, and Condensed ITtavinash80Noch keine Bewertungen

- Job Analysis in CokeDokument26 SeitenJob Analysis in CokeHijab50% (4)

- Title of Summer Internship Report@RomarioDokument5 SeitenTitle of Summer Internship Report@RomarioRomario MaibamNoch keine Bewertungen

- Shopee CompetitorsDokument4 SeitenShopee CompetitorsCuong VUongNoch keine Bewertungen

- Roll No. - Total Printed Pages:: Unit 1Dokument2 SeitenRoll No. - Total Printed Pages:: Unit 1Head SAMENoch keine Bewertungen

- LEC 5 Standard Costing and Variance AnalysisDokument33 SeitenLEC 5 Standard Costing and Variance AnalysisKelvin CulajaráNoch keine Bewertungen

- Ais Development Strategies Suggested Answers To Discussion QuestionsDokument33 SeitenAis Development Strategies Suggested Answers To Discussion QuestionsDon RajuNoch keine Bewertungen

- An Overview of The SAP R/3 Production Planning (PP) ModuleDokument130 SeitenAn Overview of The SAP R/3 Production Planning (PP) ModuleGeeta Koyalamoody100% (1)

- FSD OP1909 LatestDokument652 SeitenFSD OP1909 Latestmeening003Noch keine Bewertungen

- EADR SyllabusDokument2 SeitenEADR SyllabussanzitNoch keine Bewertungen