Das könnte Ihnen auch gefallen

- Car Rental AgreementDokument2 SeitenCar Rental AgreementRon Yhayan72% (32)

- Lease Option Power PlaysDokument68 SeitenLease Option Power PlaysMark I'Anson100% (1)

- Chapter 6 Solutions Horngren Cost AccountingDokument51 SeitenChapter 6 Solutions Horngren Cost AccountingAnik Kumar Mallick100% (3)

- Decision Making With Relevant Costs and A Strategic Emphasis Teaching Notes For CasesDokument13 SeitenDecision Making With Relevant Costs and A Strategic Emphasis Teaching Notes For Casespolerdio100% (1)

- anthonyIM 23Dokument25 SeitenanthonyIM 23ceojiNoch keine Bewertungen

- Solution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 5Dokument36 SeitenSolution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 5jasperkennedy090% (39)

- Residential House Lease AgreementDokument5 SeitenResidential House Lease AgreementOzan Bilen OngunNoch keine Bewertungen

- Riyadh Real Estate Report 2018 19 EngDokument29 SeitenRiyadh Real Estate Report 2018 19 EngTy BorjaNoch keine Bewertungen

- The Craftsman - 1906 - 08 - August PDFDokument162 SeitenThe Craftsman - 1906 - 08 - August PDFmdc2013Noch keine Bewertungen

- Fundamentals of Cost Accounting 5th Edition Lanen Solutions ManualDokument38 SeitenFundamentals of Cost Accounting 5th Edition Lanen Solutions Manualjeanbarnettxv9v100% (20)

- Fundamentals of Cost Accounting 5Th Edition Lanen Solutions Manual Full Chapter PDFDokument54 SeitenFundamentals of Cost Accounting 5Th Edition Lanen Solutions Manual Full Chapter PDFmarrowscandentyzch4c100% (10)

- Fundamentals of Product and Service Costing: Solutions To Review QuestionsDokument27 SeitenFundamentals of Product and Service Costing: Solutions To Review QuestionsLHunt100% (1)

- Case Study 4Dokument8 SeitenCase Study 4priyaa03Noch keine Bewertungen

- Chapter 6 - Fundamentals of Product and Service CostingDokument26 SeitenChapter 6 - Fundamentals of Product and Service Costingalleyezonmii100% (1)

- Chap 005Dokument40 SeitenChap 005Erica JurkowskiNoch keine Bewertungen

- Unit 6-1Dokument14 SeitenUnit 6-1Abel ZegeyeNoch keine Bewertungen

- CH 04 Kinney 9e SM Final PDFDokument41 SeitenCH 04 Kinney 9e SM Final PDFSeanLejeeBajanNoch keine Bewertungen

- Chapter 5 Activity Based Costing and Activity Based ManagementDokument69 SeitenChapter 5 Activity Based Costing and Activity Based Managementkhushboo100% (2)

- Chapter 5Dokument43 SeitenChapter 5Léo Audibert100% (2)

- Using Activity Based Costing in Service Industries.: Cost AllocationsDokument7 SeitenUsing Activity Based Costing in Service Industries.: Cost AllocationsWaqar AkhtarNoch keine Bewertungen

- C.A-I Chapter-6Dokument14 SeitenC.A-I Chapter-6Tariku KolchaNoch keine Bewertungen

- Section A P1 Q& ADokument12 SeitenSection A P1 Q& AAnisah HabibNoch keine Bewertungen

- Chapter 5 - Cost EstimationDokument36 SeitenChapter 5 - Cost Estimationalleyezonmii0% (2)

- Hilton7e SM CH6Dokument51 SeitenHilton7e SM CH6VivekRaptorNoch keine Bewertungen

- Tarek Isteak Tonmoy-2016010000130 PDFDokument7 SeitenTarek Isteak Tonmoy-2016010000130 PDFTarek Isteak TonmoyNoch keine Bewertungen

- Chap 12Dokument89 SeitenChap 12parthNoch keine Bewertungen

- ABC CostingDokument4 SeitenABC CostingKashif GulzarNoch keine Bewertungen

- Questions, Exercises, Problems, and Cases: Answers and SolutionsDokument20 SeitenQuestions, Exercises, Problems, and Cases: Answers and Solutionssanucwa6932Noch keine Bewertungen

- Cost Accounting AssignmentDokument21 SeitenCost Accounting AssignmentAdoonkii Alaha Wayn67% (3)

- Dissertation On ABC CostingDokument7 SeitenDissertation On ABC CostingBuyingPapersSingapore100% (1)

- Cost I Chapter 5Dokument10 SeitenCost I Chapter 5kenaNoch keine Bewertungen

- Cost Allocation: Chapter ThreeDokument48 SeitenCost Allocation: Chapter ThreesolomonaauNoch keine Bewertungen

- Cost Allocation& JBDokument12 SeitenCost Allocation& JBfitsumNoch keine Bewertungen

- Jariatu MGMT AssignDokument10 SeitenJariatu MGMT AssignHenry Bobson SesayNoch keine Bewertungen

- Chapter 14 SolutionsDokument35 SeitenChapter 14 SolutionsAnik Kumar MallickNoch keine Bewertungen

- Word Manaerial EcoDokument12 SeitenWord Manaerial Ecopawanijain96269Noch keine Bewertungen

- Ama-Cw, Man Ming Li ENU Matriculation ID:54088860Dokument12 SeitenAma-Cw, Man Ming Li ENU Matriculation ID:54088860manmingliNoch keine Bewertungen

- Cost Reduction Vs Cost AvoidanceDokument17 SeitenCost Reduction Vs Cost AvoidancenaveenNoch keine Bewertungen

- Cost Accounting Ch. 4Dokument41 SeitenCost Accounting Ch. 4Shady67% (3)

- CH 04 Kinney 9e SM FinalDokument41 SeitenCH 04 Kinney 9e SM FinalAshutoshNoch keine Bewertungen

- Chap 3 CMADokument34 SeitenChap 3 CMAsolomonaauNoch keine Bewertungen

- Universidade Federal de Itajubá de Itabira: CampusDokument6 SeitenUniversidade Federal de Itajubá de Itabira: CampusRepVai da NadaNoch keine Bewertungen

- Cost AccountingDokument38 SeitenCost AccountingLuccha RaiNoch keine Bewertungen

- Managerial Accounting by James JiambalvoDokument52 SeitenManagerial Accounting by James JiambalvoAhmed AliNoch keine Bewertungen

- Fourth Meeting - COST ASSIGNMENT AND ACCOUNTING ENTRIESDokument11 SeitenFourth Meeting - COST ASSIGNMENT AND ACCOUNTING ENTRIESsagung anindyaNoch keine Bewertungen

- System Design: Activity-Based Costing and ManagementDokument27 SeitenSystem Design: Activity-Based Costing and ManagementJason MablesNoch keine Bewertungen

- Chap 006Dokument61 SeitenChap 006palak32Noch keine Bewertungen

- CmaDokument10 SeitenCmabhagathnagarNoch keine Bewertungen

- Fundamentals of Cost Accounting 5th Edition Lanen Solutions Manual 1Dokument36 SeitenFundamentals of Cost Accounting 5th Edition Lanen Solutions Manual 1brittanymartinezdknybgqpes100% (27)

- Cost Model For Data Management Center (DMC) Main MenuDokument65 SeitenCost Model For Data Management Center (DMC) Main MenuCarlos Augusto Ebert GestroNoch keine Bewertungen

- P2 - Performance ManagementDokument9 SeitenP2 - Performance ManagementJosiah MwashitaNoch keine Bewertungen

- F5 - Revision Answers Dec 2010Dokument32 SeitenF5 - Revision Answers Dec 2010Vagabond Princess Rj67% (3)

- Abc Report ScriptDokument2 SeitenAbc Report ScriptKim DedicatoriaNoch keine Bewertungen

- Chap 006Dokument56 SeitenChap 006Garrett HarperNoch keine Bewertungen

- Activity-Based Costing and Activity-Based Management: Tracing, Indirect-Cost Pools, and Cost-Allocation BasesDokument9 SeitenActivity-Based Costing and Activity-Based Management: Tracing, Indirect-Cost Pools, and Cost-Allocation Basesvir1672Noch keine Bewertungen

- Financial Decision Making (FINM036) (University of Northampton-MBA) Lecturer: Arvind Harris Aharris@mauritius - Amity.eduDokument6 SeitenFinancial Decision Making (FINM036) (University of Northampton-MBA) Lecturer: Arvind Harris Aharris@mauritius - Amity.eduMelvinNoch keine Bewertungen

- Phoenix 99Dokument12 SeitenPhoenix 99Bundasak PuangchindaNoch keine Bewertungen

- ABC CostingDokument64 SeitenABC Costingvtnhan@gmail.com100% (1)

- Throughput Accounting: A Guide to Constraint ManagementVon EverandThroughput Accounting: A Guide to Constraint ManagementNoch keine Bewertungen

- Cut Costs, Grow Stronger : A Strategic Approach to What to Cut and What to KeepVon EverandCut Costs, Grow Stronger : A Strategic Approach to What to Cut and What to KeepBewertung: 5 von 5 Sternen5/5 (1)

- Mandatory Benefit Secrets: How to Turn Statutes Into AssetsVon EverandMandatory Benefit Secrets: How to Turn Statutes Into AssetsNoch keine Bewertungen

- Cost Reduction Strategies for the Manufacturing Sector With Application of Microsoft ExcelVon EverandCost Reduction Strategies for the Manufacturing Sector With Application of Microsoft ExcelNoch keine Bewertungen

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesVon EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNoch keine Bewertungen

- 1-8 GST - GST Payable or ITC AvalDokument2 Seiten1-8 GST - GST Payable or ITC Avaloddsey0713Noch keine Bewertungen

- Does FBT Apply?: Div 13 ExclusionsDokument1 SeiteDoes FBT Apply?: Div 13 Exclusionsoddsey0713Noch keine Bewertungen

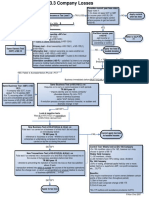

- 3-3 Company LossesDokument1 Seite3-3 Company Lossesoddsey0713Noch keine Bewertungen

- 4-3 Part IVA General AntiAvoidanceDokument1 Seite4-3 Part IVA General AntiAvoidanceoddsey0713Noch keine Bewertungen

- 2-3 Capital AllowancesDokument1 Seite2-3 Capital Allowancesoddsey0713Noch keine Bewertungen

- 3-3 Franking AccountDokument1 Seite3-3 Franking Accountoddsey0713Noch keine Bewertungen

- 2-4,5 Capital WorksDokument1 Seite2-4,5 Capital Worksoddsey0713Noch keine Bewertungen

- Case Summaries 1 193Dokument54 SeitenCase Summaries 1 193oddsey0713100% (1)

- 3-3 Div 7A Deemed Divs - VLDokument1 Seite3-3 Div 7A Deemed Divs - VLoddsey0713Noch keine Bewertungen

- T6 Chapter 5 Solutions To The Essential ActivitiesDokument12 SeitenT6 Chapter 5 Solutions To The Essential Activitiesoddsey0713Noch keine Bewertungen

- 1859 Welcome LetterDokument3 Seiten1859 Welcome LetterYi WangNoch keine Bewertungen

- Case Studies Using Demand and Supply AnalysisDokument12 SeitenCase Studies Using Demand and Supply Analysiskirtiinitya100% (1)

- SIGNED Contract of Lease Parking Slot No. 1 MauiDokument5 SeitenSIGNED Contract of Lease Parking Slot No. 1 Mauielvie epilNoch keine Bewertungen

- Royalty Account: Royalty Meaning in AccountingDokument8 SeitenRoyalty Account: Royalty Meaning in AccountingMahfooz AlamNoch keine Bewertungen

- BlueFrog - Lease AgreementDokument6 SeitenBlueFrog - Lease Agreementrentbluefrog0% (1)

- April 2016Dokument15 SeitenApril 2016Pumper TraderNoch keine Bewertungen

- Maintenance Request - WORK ORDER: Building/Job Details Tenant DetailsDokument2 SeitenMaintenance Request - WORK ORDER: Building/Job Details Tenant DetailsKing_of_SenseNoch keine Bewertungen

- Bangkok Retail 4q13Dokument1 SeiteBangkok Retail 4q13Bea LorinczNoch keine Bewertungen

- Yulo vs. Yang Chiao SengDokument8 SeitenYulo vs. Yang Chiao SengJerome ArañezNoch keine Bewertungen

- Puregold Annual Report CY 2018Dokument152 SeitenPuregold Annual Report CY 2018Jessa Joy Alano Lopez100% (1)

- Investment PropertyDokument1 SeiteInvestment PropertyAmor SaladinoNoch keine Bewertungen

- Commercial AgreementDokument14 SeitenCommercial Agreementratna_p_pNoch keine Bewertungen

- BCom Business Taxation Income Tax and Sales Tax Numerical 2018Dokument5 SeitenBCom Business Taxation Income Tax and Sales Tax Numerical 2018AHSAN LASHARINoch keine Bewertungen

- Bsa2105 FS2021 Vat Da22412Dokument7 SeitenBsa2105 FS2021 Vat Da22412ela kikayNoch keine Bewertungen

- Consideration PropDokument2 SeitenConsideration PropQasim GorayaNoch keine Bewertungen

- Lease Contract ResidentialDokument5 SeitenLease Contract ResidentialMatel LazaroNoch keine Bewertungen

- 071021241446Dokument13 Seiten071021241446Paras NigamNoch keine Bewertungen

- Solved Tovar Applied For The Position of Resident Physician in PaxtonDokument1 SeiteSolved Tovar Applied For The Position of Resident Physician in PaxtonAnbu jaromiaNoch keine Bewertungen

- Taxation Law Review FinalsDokument6 SeitenTaxation Law Review FinalsLean Manuel ParagasNoch keine Bewertungen

- CH 21Dokument48 SeitenCH 21Iris MaNoch keine Bewertungen

- Unit 4 Container Types and BusinessDokument16 SeitenUnit 4 Container Types and BusinessjohnpratheeshNoch keine Bewertungen

- Taylor's Hostel Management ApplicationDokument2 SeitenTaylor's Hostel Management ApplicationFahad FarhanNoch keine Bewertungen

- BCAS v13n04Dokument78 SeitenBCAS v13n04Len HollowayNoch keine Bewertungen

- F-05 814 Pricing StrategyDokument24 SeitenF-05 814 Pricing Strategydinosaur2512Noch keine Bewertungen

- Special Events NotesDokument14 SeitenSpecial Events NotesSangesh Nattamai100% (1)