Das könnte Ihnen auch gefallen

- Anything Goes: An Advanced Reader of Modern Chinese - Revised EditionVon EverandAnything Goes: An Advanced Reader of Modern Chinese - Revised EditionBewertung: 5 von 5 Sternen5/5 (1)

- Standalone Financial Results, Auditors Report For March 31, 2016 (Result)Dokument14 SeitenStandalone Financial Results, Auditors Report For March 31, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Metal Valves & Pipe Fittings World Summary: Market Values & Financials by CountryVon EverandMetal Valves & Pipe Fittings World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- Standalone Financial Results, Form A, Auditors Report For March 31, 2016 (Result)Dokument8 SeitenStandalone Financial Results, Form A, Auditors Report For March 31, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Machine Tools, Metal Cutting Types World Summary: Market Values & Financials by CountryVon EverandMachine Tools, Metal Cutting Types World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- Financial Results, Limited Review Report, Results Press Release For December 31, 2015 (Result)Dokument6 SeitenFinancial Results, Limited Review Report, Results Press Release For December 31, 2015 (Result)Shyam SunderNoch keine Bewertungen

- Standalone Financial Results, Auditors Report For March 31, 2016 (Result)Dokument10 SeitenStandalone Financial Results, Auditors Report For March 31, 2016 (Result)Shyam SunderNoch keine Bewertungen

- A Trip to China: An Intermediate Reader of Modern Chinese - Revised EditionVon EverandA Trip to China: An Intermediate Reader of Modern Chinese - Revised EditionBewertung: 3.5 von 5 Sternen3.5/5 (8)

- Marcom Dlms SolutionsDokument18 SeitenMarcom Dlms SolutionsMARCOM SRLNoch keine Bewertungen

- General Radio 650-ADokument16 SeitenGeneral Radio 650-ApohopetchNoch keine Bewertungen

- Manual IpsDokument329 SeitenManual IpsDavid Naranjo Amores80% (5)

- Costume Jewelry & Novelties World Summary: Market Values & Financials by CountryVon EverandCostume Jewelry & Novelties World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- Financial Results & Limited Review Report For Dec 31, 2015 (Standalone) (Result)Dokument3 SeitenFinancial Results & Limited Review Report For Dec 31, 2015 (Standalone) (Result)Shyam SunderNoch keine Bewertungen

- Bhabha - The Commitment To TheoryDokument13 SeitenBhabha - The Commitment To TheorysafeplasticNoch keine Bewertungen

- Intermediate Reader of Modern Chinese: Volume I: TextVon EverandIntermediate Reader of Modern Chinese: Volume I: TextNoch keine Bewertungen

- (1893) Boxing A Manual Devoted To The Art of Self Defense - James SullivanDokument22 Seiten(1893) Boxing A Manual Devoted To The Art of Self Defense - James SullivanSamurai_Chef100% (1)

- 110 Semiconductor Projects for the Home ConstructorVon Everand110 Semiconductor Projects for the Home ConstructorBewertung: 4 von 5 Sternen4/5 (1)

- Alinco DJ-580T Instruction Manual Part 1Dokument11 SeitenAlinco DJ-580T Instruction Manual Part 1Yayok S. AnggoroNoch keine Bewertungen

- Clamptek Toggle CatalogueDokument109 SeitenClamptek Toggle CatalogueAlimco TirupatiNoch keine Bewertungen

- XR7040 SMDokument57 SeitenXR7040 SMJeff BrintonNoch keine Bewertungen

- Evanghelia Eseniana Partea 2Dokument72 SeitenEvanghelia Eseniana Partea 2Gugescu Gianina100% (2)

- Casio Fx6200g User ManualDokument60 SeitenCasio Fx6200g User Manualnoogy2noogyNoch keine Bewertungen

- Ref Binder1 Home LoanDokument31 SeitenRef Binder1 Home Loankyawmoehein65Noch keine Bewertungen

- Tuning Old Skool FordsDokument54 SeitenTuning Old Skool FordsTRIZtease100% (4)

- Bank StatementDokument6 SeitenBank StatementFirstpostNoch keine Bewertungen

- Ma Tae Khin Ba Loke Kya Ma LeDokument58 SeitenMa Tae Khin Ba Loke Kya Ma LeyeufamilyNoch keine Bewertungen

- Ingersoll (1987) - The Theory of Financial Decision MakingDokument16 SeitenIngersoll (1987) - The Theory of Financial Decision MakingsafiebuttNoch keine Bewertungen

- Standalone Financial Results For September 30, 2016 (Result)Dokument4 SeitenStandalone Financial Results For September 30, 2016 (Result)Shyam SunderNoch keine Bewertungen

- TCVN 1916-1995Dokument44 SeitenTCVN 1916-1995Vu Anh TuanNoch keine Bewertungen

- Nostalgia 4Dokument28 SeitenNostalgia 4Sreekanth SreeNoch keine Bewertungen

- Myanmar Ebooks Myanmar TaYarTawMyar Sate Shaw Phoot Te A LoteDokument30 SeitenMyanmar Ebooks Myanmar TaYarTawMyar Sate Shaw Phoot Te A Lotezar_chi_3Noch keine Bewertungen

- Briefings On Existence - BadiouDokument32 SeitenBriefings On Existence - BadioumadspeterNoch keine Bewertungen

- New Flag JournalDokument68 SeitenNew Flag JournalMoe Ma KaNoch keine Bewertungen

- Yco 5.5Dokument16 SeitenYco 5.5ycowanewsNoch keine Bewertungen

- Wayy Lay Kaung LayDokument100 SeitenWayy Lay Kaung LayMyomyat ThuNoch keine Bewertungen

- Movement For The Advancement of Filipino Nationalism (MAN) - 1969 - R. ConstantinoDokument47 SeitenMovement For The Advancement of Filipino Nationalism (MAN) - 1969 - R. ConstantinoBert M DronaNoch keine Bewertungen

- VODOGRADNJEDokument100 SeitenVODOGRADNJEIVANNoch keine Bewertungen

- MS Word NerchukondiDokument43 SeitenMS Word Nerchukondipvaraogitam100% (1)

- Altenmuller Apotropaia IDokument98 SeitenAltenmuller Apotropaia IMizraim2010Noch keine Bewertungen

- Sony P3B KV2127R 2137RSDokument36 SeitenSony P3B KV2127R 2137RSJoaquín Roberto Sánchez Ortiz100% (1)

- Fadli's Intro To HadithDokument94 SeitenFadli's Intro To HadithImammiyah HallNoch keine Bewertungen

- Surya Namaskar InstructionsDokument12 SeitenSurya Namaskar InstructionsDeepa MadhavanNoch keine Bewertungen

- Siddha Sadhana - Bimba Roopa Kaambudake - Ananda Rao, Maadhu RaoDokument40 SeitenSiddha Sadhana - Bimba Roopa Kaambudake - Ananda Rao, Maadhu Raoಮಂಜುನಾಥ್ ಮಾದಯ್ಯNoch keine Bewertungen

- Anwar Shaikh - Valor Acumulacion Y Crisis (Book)Dokument203 SeitenAnwar Shaikh - Valor Acumulacion Y Crisis (Book)Ismael ValverdeNoch keine Bewertungen

- Standalone & Consolidated Financial Results, Limited Review Report For September 30, 2016 (Result)Dokument10 SeitenStandalone & Consolidated Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Navico RT6500 User ManualDokument8 SeitenNavico RT6500 User ManualmarinamarigotNoch keine Bewertungen

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Dokument4 SeitenStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Leader TR Dip Meter LDM-815 Instruction ManualDokument8 SeitenLeader TR Dip Meter LDM-815 Instruction Manualvlad_alucardNoch keine Bewertungen

- Bs-3692 Iso Metric Precision Hexagon Bolts, Screws, and NutsDokument34 SeitenBs-3692 Iso Metric Precision Hexagon Bolts, Screws, and NutsUmesh ChamaraNoch keine Bewertungen

- Philips 4cm2799 TV DDokument10 SeitenPhilips 4cm2799 TV DroscovanulNoch keine Bewertungen

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Dokument4 SeitenStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNoch keine Bewertungen

- The Victoria Mills: /lclflclljiDokument2 SeitenThe Victoria Mills: /lclflclljinaresh kayadNoch keine Bewertungen

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Dokument3 SeitenStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Dictionar Englez RomanDokument252 SeitenDictionar Englez Romanaliaj2Noch keine Bewertungen

- 2cm German AmmunitionDokument57 Seiten2cm German AmmunitionJános MolnárNoch keine Bewertungen

- Settlement Order in Respect of Bikaner Wooltex Pvt. Limited in The Matter of Sangam Advisors LimitedDokument2 SeitenSettlement Order in Respect of Bikaner Wooltex Pvt. Limited in The Matter of Sangam Advisors LimitedShyam SunderNoch keine Bewertungen

- Mutual Fund Holdings in DHFLDokument7 SeitenMutual Fund Holdings in DHFLShyam SunderNoch keine Bewertungen

- Order of Hon'ble Supreme Court in The Matter of The SaharasDokument6 SeitenOrder of Hon'ble Supreme Court in The Matter of The SaharasShyam SunderNoch keine Bewertungen

- HINDUNILVR: Hindustan Unilever LimitedDokument1 SeiteHINDUNILVR: Hindustan Unilever LimitedShyam SunderNoch keine Bewertungen

- PR - Exit Order in Respect of Spice & Oilseeds Exchange Limited (Soel)Dokument1 SeitePR - Exit Order in Respect of Spice & Oilseeds Exchange Limited (Soel)Shyam SunderNoch keine Bewertungen

- JUSTDIAL Mutual Fund HoldingsDokument2 SeitenJUSTDIAL Mutual Fund HoldingsShyam SunderNoch keine Bewertungen

- Financial Results For June 30, 2014 (Audited) (Result)Dokument3 SeitenFinancial Results For June 30, 2014 (Audited) (Result)Shyam SunderNoch keine Bewertungen

- Standalone Financial Results, Auditors Report For March 31, 2016 (Result)Dokument5 SeitenStandalone Financial Results, Auditors Report For March 31, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Exit Order in Respect of The Spice and Oilseeds Exchange Limited, SangliDokument5 SeitenExit Order in Respect of The Spice and Oilseeds Exchange Limited, SangliShyam SunderNoch keine Bewertungen

- Financial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Dokument4 SeitenFinancial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Shyam SunderNoch keine Bewertungen

- Financial Results, Limited Review Report For December 31, 2015 (Result)Dokument4 SeitenFinancial Results, Limited Review Report For December 31, 2015 (Result)Shyam SunderNoch keine Bewertungen

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Dokument3 SeitenStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Settlement Order in Respect of R.R. Corporate Securities LimitedDokument2 SeitenSettlement Order in Respect of R.R. Corporate Securities LimitedShyam SunderNoch keine Bewertungen

- Financial Results & Limited Review Report For June 30, 2015 (Standalone) (Result)Dokument3 SeitenFinancial Results & Limited Review Report For June 30, 2015 (Standalone) (Result)Shyam SunderNoch keine Bewertungen

- Standalone Financial Results For March 31, 2016 (Result)Dokument11 SeitenStandalone Financial Results For March 31, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Financial Results For Dec 31, 2013 (Result)Dokument4 SeitenFinancial Results For Dec 31, 2013 (Result)Shyam Sunder0% (1)

- Financial Results For Mar 31, 2014 (Result)Dokument2 SeitenFinancial Results For Mar 31, 2014 (Result)Shyam SunderNoch keine Bewertungen

- Standalone Financial Results For September 30, 2016 (Result)Dokument3 SeitenStandalone Financial Results For September 30, 2016 (Result)Shyam SunderNoch keine Bewertungen

- PDF Processed With Cutepdf Evaluation EditionDokument3 SeitenPDF Processed With Cutepdf Evaluation EditionShyam SunderNoch keine Bewertungen

- Financial Results For June 30, 2013 (Audited) (Result)Dokument2 SeitenFinancial Results For June 30, 2013 (Audited) (Result)Shyam SunderNoch keine Bewertungen

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Dokument5 SeitenStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Dokument4 SeitenStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Dokument3 SeitenStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Financial Results For September 30, 2013 (Result)Dokument2 SeitenFinancial Results For September 30, 2013 (Result)Shyam SunderNoch keine Bewertungen

- Standalone Financial Results For June 30, 2016 (Result)Dokument2 SeitenStandalone Financial Results For June 30, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Dokument4 SeitenStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Dokument4 SeitenStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Dokument4 SeitenStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNoch keine Bewertungen

- Transcript of The Investors / Analysts Con Call (Company Update)Dokument15 SeitenTranscript of The Investors / Analysts Con Call (Company Update)Shyam SunderNoch keine Bewertungen

- Investor Presentation For December 31, 2016 (Company Update)Dokument27 SeitenInvestor Presentation For December 31, 2016 (Company Update)Shyam SunderNoch keine Bewertungen

- Latihan Soal Cash FlowDokument2 SeitenLatihan Soal Cash FlowRuth AngeliaNoch keine Bewertungen

- Chapter 18 Answer KeyDokument9 SeitenChapter 18 Answer KeyNCT100% (1)

- Genmo CorporationDokument12 SeitenGenmo CorporationAarushi Pawar100% (1)

- WIPRO Wealth Creation StoryDokument3 SeitenWIPRO Wealth Creation StoryvikramNoch keine Bewertungen

- Keloggs DragonDokument8 SeitenKeloggs DragonLakshmi ThiagarajanNoch keine Bewertungen

- CAPE Accounting 2010 U1 P2Dokument8 SeitenCAPE Accounting 2010 U1 P2leah hostenNoch keine Bewertungen

- 2010 SampleEntranceExamDokument76 Seiten2010 SampleEntranceExamPavan KumarNoch keine Bewertungen

- Cost Accounting: Quiz 1Dokument11 SeitenCost Accounting: Quiz 1ASILINA BUULOLONoch keine Bewertungen

- Ch09 - Cost of Capital 12112020 125813pmDokument13 SeitenCh09 - Cost of Capital 12112020 125813pmMuhammad Umar BashirNoch keine Bewertungen

- V F Corporation NYSE VFC FinancialsDokument9 SeitenV F Corporation NYSE VFC FinancialsAmalia MegaNoch keine Bewertungen

- CH 15 Anchoring On The Financial Statements Simple Forecasting and Simple ValuationDokument25 SeitenCH 15 Anchoring On The Financial Statements Simple Forecasting and Simple ValuationRocky HunilaNoch keine Bewertungen

- Share CertificateDokument4 SeitenShare CertificateSohail Shaikh'sNoch keine Bewertungen

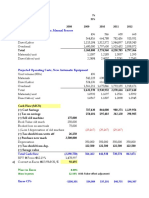

- Projected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Dokument4 SeitenProjected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Cesar CameyNoch keine Bewertungen

- Tutorial 9 PM AnswersDokument6 SeitenTutorial 9 PM AnswersKhanh Linh LeNoch keine Bewertungen

- Laporan Tahunan - Annual Report AMFG 2021Dokument178 SeitenLaporan Tahunan - Annual Report AMFG 2021Sella YunitaNoch keine Bewertungen

- Topic: Explain CAPM With Assumptions. IntroductionDokument3 SeitenTopic: Explain CAPM With Assumptions. Introductiondeepti sharmaNoch keine Bewertungen

- Foa Ii Individual AssignmentDokument3 SeitenFoa Ii Individual Assignmentyosef mechalNoch keine Bewertungen

- Nism and Crisil Certified Wealth ManagerDokument14 SeitenNism and Crisil Certified Wealth ManagerChaitanya FulariNoch keine Bewertungen

- Fsa Assignment 1 PDFDokument19 SeitenFsa Assignment 1 PDFMUHAMMAD UMARNoch keine Bewertungen

- Quiz - Single Entry (Answer Key)Dokument2 SeitenQuiz - Single Entry (Answer Key)Gloria BeltranNoch keine Bewertungen

- Bank Statment Wells FargoDokument7 SeitenBank Statment Wells FargoYu ShilohNoch keine Bewertungen

- ACCT1101 - Questions - Chapter 06Dokument5 SeitenACCT1101 - Questions - Chapter 06Zong Zheng SunNoch keine Bewertungen

- Adh Newipo IpoDokument759 SeitenAdh Newipo IpoSathishKumarNoch keine Bewertungen

- Olam Brokers' ReportDokument9 SeitenOlam Brokers' Reportsananth60100% (1)

- Capital Budgeting - Baldwin Inc (Solved)Dokument27 SeitenCapital Budgeting - Baldwin Inc (Solved)Contact InfoNoch keine Bewertungen

- Bamuya Fabm Act-3Dokument2 SeitenBamuya Fabm Act-3Irish C. BamuyaNoch keine Bewertungen

- Annual Report - 2020 - Linde Bangladesh BOCDokument90 SeitenAnnual Report - 2020 - Linde Bangladesh BOCAtiqul islamNoch keine Bewertungen

- Case 2 AT&TDokument13 SeitenCase 2 AT&TSean Moore100% (1)

- FIN 460-END OF Chap 2 - AmendedDokument5 SeitenFIN 460-END OF Chap 2 - AmendedBombitaNoch keine Bewertungen

- Chapter 2 (Prob.1-10) - Partnership and Corp.Dokument10 SeitenChapter 2 (Prob.1-10) - Partnership and Corp.Andrea Joy ReyNoch keine Bewertungen