Das könnte Ihnen auch gefallen

- Poseidon Perspective No. 24 September 2010Dokument20 SeitenPoseidon Perspective No. 24 September 2010Brian SheanNoch keine Bewertungen

- 7.0 Poseidon Perspective July 2010Dokument21 Seiten7.0 Poseidon Perspective July 2010Brian SheanNoch keine Bewertungen

- 5.0 Pose Id On Perspective May 2010Dokument20 Seiten5.0 Pose Id On Perspective May 2010Brian SheanNoch keine Bewertungen

- 6.0 Poseidon Perspective June 2010Dokument17 Seiten6.0 Poseidon Perspective June 2010Brian SheanNoch keine Bewertungen

- 4.0 Poseidon Perspective April 2010Dokument15 Seiten4.0 Poseidon Perspective April 2010Brian SheanNoch keine Bewertungen

- 1.0 Poseidon Perspective January 2010Dokument17 Seiten1.0 Poseidon Perspective January 2010Brian SheanNoch keine Bewertungen

- 3.0 Poseidon Perspective March 2010Dokument18 Seiten3.0 Poseidon Perspective March 2010Brian SheanNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Audit and Internal ReviewDokument7 SeitenAudit and Internal ReviewkhengmaiNoch keine Bewertungen

- TGMCDokument90 SeitenTGMCRavi KumarNoch keine Bewertungen

- Teacher's Handout MoneyDokument5 SeitenTeacher's Handout MoneyannNoch keine Bewertungen

- Prob. 1 Audit 4Dokument2 SeitenProb. 1 Audit 4Annalyn AlmarioNoch keine Bewertungen

- Financial Regulators Who They Are and What They DoDokument1 SeiteFinancial Regulators Who They Are and What They Doomidreza tabrizianNoch keine Bewertungen

- Interview questions and answers on e-banking servicesDokument6 SeitenInterview questions and answers on e-banking servicesMega Pop LockerNoch keine Bewertungen

- Synopsis On Comparative Study On ICICI and SBIDokument9 SeitenSynopsis On Comparative Study On ICICI and SBIitsruchika18100% (7)

- CAPITAL-MARKET-BBA-3RD-SEM - FinalDokument84 SeitenCAPITAL-MARKET-BBA-3RD-SEM - FinalSunny MittalNoch keine Bewertungen

- Factoring As A Financial AlternativeDokument10 SeitenFactoring As A Financial AlternativeJovica RacicNoch keine Bewertungen

- Risk Management - Sample QuestionsDokument11 SeitenRisk Management - Sample QuestionsSandeep Spartacus100% (1)

- 17 Soriano v. BSPDokument6 Seiten17 Soriano v. BSPChester BryanNoch keine Bewertungen

- Deed of UndertakingDokument5 SeitenDeed of UndertakingPeter Roderick M. OlpocNoch keine Bewertungen

- Premium Credit Card UsersDokument54 SeitenPremium Credit Card UserscityNoch keine Bewertungen

- Sources of Business Finance ExplainedDokument39 SeitenSources of Business Finance ExplainedCarry MinatiNoch keine Bewertungen

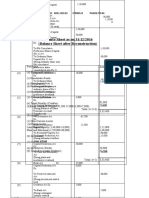

- Balance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)Dokument8 SeitenBalance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)GauravNoch keine Bewertungen

- LITERATURE REVIEW ON ASSET-LIABILITY MANAGEMENTDokument9 SeitenLITERATURE REVIEW ON ASSET-LIABILITY MANAGEMENTAnkur Upadhyay0% (1)

- Debt Elimination Is Based On Understanding How YouDokument20 SeitenDebt Elimination Is Based On Understanding How YouHorton Glenn100% (13)

- KRISHNA POWER CENTRE statementDokument17 SeitenKRISHNA POWER CENTRE statementsukhdev bhattarNoch keine Bewertungen

- UK Banking StructureDokument35 SeitenUK Banking StructureSabiha Farzana MoonmoonNoch keine Bewertungen

- Role of Commercial Banks in The Economic Development of A Country:-An Indian PerspectiveDokument10 SeitenRole of Commercial Banks in The Economic Development of A Country:-An Indian Perspectivepinky kumariNoch keine Bewertungen

- First Consolidated BankDokument3 SeitenFirst Consolidated BankMichael John LunaNoch keine Bewertungen

- 2341 SafestBanksPR 9 09Dokument2 Seiten2341 SafestBanksPR 9 09Danny J. BrouillardNoch keine Bewertungen

- Financial Services ProjectDokument32 SeitenFinancial Services Projecthimita desaiNoch keine Bewertungen

- Debt InstrumentsDokument5 SeitenDebt InstrumentsŚáńtőśh MőkáśhíNoch keine Bewertungen

- Analysis of Frauds in Indian Banking SectorDokument4 SeitenAnalysis of Frauds in Indian Banking SectorEditor IJTSRD100% (1)

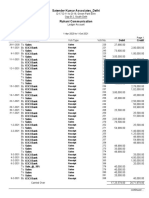

- Satender Kumar Associates - DelhiDokument7 SeitenSatender Kumar Associates - DelhiAVS & AssociatesNoch keine Bewertungen

- Trade Finance KYC ChecklistDokument3 SeitenTrade Finance KYC ChecklistHarpreet SinghNoch keine Bewertungen

- DRDADokument8 SeitenDRDAworld_best284562100% (1)

- Financial Performance Analysis of Nepalese Commercial BanksDokument83 SeitenFinancial Performance Analysis of Nepalese Commercial Bankssps fetrNoch keine Bewertungen

- Banking NotesDokument104 SeitenBanking NotesprasanthNoch keine Bewertungen