Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- RURAL Banking in India ProjectDokument107 SeitenRURAL Banking in India Projectdevendra68% (28)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- 1994 - Coates - A Review of CaneDokument3 Seiten1994 - Coates - A Review of CaneAnonymous smFxIR07Noch keine Bewertungen

- Horn Expose Is Reputation Quotient A Valid and Reliable MeasureDokument31 SeitenHorn Expose Is Reputation Quotient A Valid and Reliable MeasureAnonymous smFxIR07Noch keine Bewertungen

- 1994 - Coates - A Review of CaneDokument3 Seiten1994 - Coates - A Review of CaneAnonymous smFxIR07Noch keine Bewertungen

- Revenue Direct Expenses: Budgeted Income Statement For The Six Months To 31/8/10Dokument2 SeitenRevenue Direct Expenses: Budgeted Income Statement For The Six Months To 31/8/10Anonymous smFxIR07Noch keine Bewertungen

- Six Sigma and TQM in Taiwan An Empirical Study of Discriminate AnalysisDokument17 SeitenSix Sigma and TQM in Taiwan An Empirical Study of Discriminate AnalysisAnonymous smFxIR07Noch keine Bewertungen

- Sasa PDFDokument9 SeitenSasa PDFAnonymous smFxIR07Noch keine Bewertungen

- Notes For Part 6Dokument5 SeitenNotes For Part 6Anonymous smFxIR07Noch keine Bewertungen

- Flammability: A Safety Guide For Users: Best Practice Guidelines N°Dokument48 SeitenFlammability: A Safety Guide For Users: Best Practice Guidelines N°Anonymous smFxIR07Noch keine Bewertungen

- Bolts TechnicalData PDFDokument48 SeitenBolts TechnicalData PDFAnonymous smFxIR07Noch keine Bewertungen

- Duck Industry Performance Report 2013Dokument14 SeitenDuck Industry Performance Report 2013Donald RemulaNoch keine Bewertungen

- MCL Act 93 of 1981Dokument4 SeitenMCL Act 93 of 1981Dennis JudsonNoch keine Bewertungen

- Thesis1 PDFDokument329 SeitenThesis1 PDFUma deviNoch keine Bewertungen

- Soil SSCDokument11 SeitenSoil SSCvkjha623477Noch keine Bewertungen

- Australasia X IDokument1 SeiteAustralasia X Ijose del carmen naranjo jimenezNoch keine Bewertungen

- Genetics and Biotechnology Reaction PaperDokument2 SeitenGenetics and Biotechnology Reaction PaperARLENE POMBONoch keine Bewertungen

- 5 Digest - SALAS VS CABUNGCAL GR 191545Dokument3 Seiten5 Digest - SALAS VS CABUNGCAL GR 191545Paul Joshua Suba50% (2)

- Capacity Building For AfricaDokument8 SeitenCapacity Building For AfricaTaofeeq YekinniNoch keine Bewertungen

- 2015 Agstar Vendor Directory July 2015 508 072715Dokument64 Seiten2015 Agstar Vendor Directory July 2015 508 072715Mbamali ChukwunenyeNoch keine Bewertungen

- Lesson 12.1 - StudentDokument13 SeitenLesson 12.1 - StudentChrise RajNoch keine Bewertungen

- Influence of Lime ...Dokument7 SeitenInfluence of Lime ...Luna EléctricaNoch keine Bewertungen

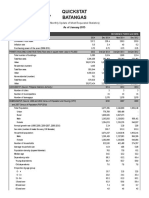

- Quickstat Batangas: (Monthly Update of Most Requested Statistics)Dokument5 SeitenQuickstat Batangas: (Monthly Update of Most Requested Statistics)Martin Owen CallejaNoch keine Bewertungen

- Response of Intercropping and Different Row Ratios On Growth and Yield of Wheat (Triticum Aestivum) Under Rainfed Condition of Kaymore PlateauDokument5 SeitenResponse of Intercropping and Different Row Ratios On Growth and Yield of Wheat (Triticum Aestivum) Under Rainfed Condition of Kaymore PlateautheijesNoch keine Bewertungen

- Complete Report - Docx KSCST 41S - B - BE - 026 PDFDokument96 SeitenComplete Report - Docx KSCST 41S - B - BE - 026 PDFShiva PrasadNoch keine Bewertungen

- The Coastal Zone of BangladeshDokument2 SeitenThe Coastal Zone of BangladeshZulfiquar AhmedNoch keine Bewertungen

- Agriculture Current AffairsDokument6 SeitenAgriculture Current Affairshiteshrao810Noch keine Bewertungen

- Grade 6 End of Year Exam CoverageDokument27 SeitenGrade 6 End of Year Exam CoverageMouza Al ArimiNoch keine Bewertungen

- Case Study 8Dokument2 SeitenCase Study 8AwesomeNoch keine Bewertungen

- Draft Kawainui-Hamakua Master PlanDokument153 SeitenDraft Kawainui-Hamakua Master PlanHPR NewsNoch keine Bewertungen

- Advt No.33-2020 05-11-2020 X7 VersionDokument1 SeiteAdvt No.33-2020 05-11-2020 X7 VersionumairNoch keine Bewertungen

- Sugar Beet Pulp PLDokument3 SeitenSugar Beet Pulp PLyousria.ahmed46Noch keine Bewertungen

- Role of ICT in AgribusinessDokument26 SeitenRole of ICT in AgribusinessEsther Dominguez100% (1)

- Pala Yamanan PlusDokument44 SeitenPala Yamanan PlusRayge HarbskyNoch keine Bewertungen

- Vegetative PropagationDokument20 SeitenVegetative PropagationMarcus RashfordNoch keine Bewertungen

- Nikhil Pratap Singh, Et AlDokument10 SeitenNikhil Pratap Singh, Et Aljyoti singhNoch keine Bewertungen

- The Waterman of Alwarpalli - Ambica VinodDokument9 SeitenThe Waterman of Alwarpalli - Ambica VinodPratham BooksNoch keine Bewertungen

- Sapkale J.B. Geography-Impact of Urmodi Dam On Rehabilitated People of Satara District, MaharashtraDokument3 SeitenSapkale J.B. Geography-Impact of Urmodi Dam On Rehabilitated People of Satara District, MaharashtraJagdish SapkaleNoch keine Bewertungen

- TT21 28112019BNN (E)Dokument40 SeitenTT21 28112019BNN (E)Thanh Tâm TrầnNoch keine Bewertungen

- On GMO: A Research PaperDokument11 SeitenOn GMO: A Research PaperTao DoNoch keine Bewertungen