Das könnte Ihnen auch gefallen

- Loan SyndicationDokument4 SeitenLoan Syndicationsantu15038847420Noch keine Bewertungen

- Lecture 4 - Syndicated LoansDokument13 SeitenLecture 4 - Syndicated LoansEmmanuel MwapeNoch keine Bewertungen

- Loan SyndicationDokument35 SeitenLoan Syndicationdivyapillai0201_Noch keine Bewertungen

- Loan SyndicationDokument14 SeitenLoan SyndicationGaurav Shah100% (3)

- Syndicate LaonDokument6 SeitenSyndicate Laonarpitm61Noch keine Bewertungen

- Syndication LoanDokument21 SeitenSyndication LoanneemNoch keine Bewertungen

- Laws Related To Banking in IndiaDokument48 SeitenLaws Related To Banking in IndiaRohit Sharma75% (8)

- Syndicated LoanDokument33 SeitenSyndicated LoanAarti YadavNoch keine Bewertungen

- Case Study Loan Syndication Fort IsDokument13 SeitenCase Study Loan Syndication Fort Ishesham88Noch keine Bewertungen

- Loan SyndicationDokument6 SeitenLoan SyndicationNaymur RahmanNoch keine Bewertungen

- Loan Syndication State Bank of IndiaDokument52 SeitenLoan Syndication State Bank of Indiakavita75% (4)

- Loan SyndicationDokument12 SeitenLoan SyndicationArpit Jain100% (1)

- Rohan Proj - Report Loan SyndicationDokument75 SeitenRohan Proj - Report Loan Syndicationriranna100% (5)

- Syndicated Loan MarketDokument56 SeitenSyndicated Loan MarketYolanda Glover100% (1)

- Bank Loan Covenants PrimerDokument5 SeitenBank Loan Covenants PrimerPropertywizzNoch keine Bewertungen

- Syndicated Loan AgreementDokument49 SeitenSyndicated Loan Agreementcasey9759949Noch keine Bewertungen

- Final Project Loan SyndicationDokument48 SeitenFinal Project Loan Syndicationmaulik1391Noch keine Bewertungen

- Sample Joint-Mandate-LetterDokument15 SeitenSample Joint-Mandate-LetterAmit Verma100% (1)

- Loan SyndicationDokument4 SeitenLoan SyndicationRalsha DinoopNoch keine Bewertungen

- Banking CH 4 Relationship Between Banker and Customer-1Dokument9 SeitenBanking CH 4 Relationship Between Banker and Customer-1AbiyNoch keine Bewertungen

- LoansDokument17 SeitenLoansPia Samantha DasecoNoch keine Bewertungen

- Loan SyndicationDokument49 SeitenLoan SyndicationShruthi ShettyNoch keine Bewertungen

- Loan SyndicationDokument11 SeitenLoan SyndicationArun DasNoch keine Bewertungen

- Why Do The Banks Syndicate LoansDokument8 SeitenWhy Do The Banks Syndicate LoansIvan SemedoNoch keine Bewertungen

- Debt SecuritizationDokument20 SeitenDebt SecuritizationSandeep KulshresthaNoch keine Bewertungen

- 869 Mutual FundDokument13 Seiten869 Mutual FundRutik PanchalNoch keine Bewertungen

- Coral - Commitment LetterDokument283 SeitenCoral - Commitment LetterMarius AngaraNoch keine Bewertungen

- Decoding Term Sheets & iSAFE NotesDokument17 SeitenDecoding Term Sheets & iSAFE NotesMehta SubscriptionsNoch keine Bewertungen

- DebentureDokument34 SeitenDebentureSOHEL BANGINoch keine Bewertungen

- Ipo ProcessDokument9 SeitenIpo Processrahulkoli25Noch keine Bewertungen

- Name-Rohit Kiran Keluskar. Class - Tybcbi ROLL NO - 1510726. Subject - Central Banking Topic - Loan SyndicationDokument8 SeitenName-Rohit Kiran Keluskar. Class - Tybcbi ROLL NO - 1510726. Subject - Central Banking Topic - Loan Syndicationrohit keluskarNoch keine Bewertungen

- Report On Loan Syndication & Financial Services For Fund Based Credit Facility in The Form of Cash CreditDokument76 SeitenReport On Loan Syndication & Financial Services For Fund Based Credit Facility in The Form of Cash Creditravishivhare89% (9)

- Loan SyndicationDokument53 SeitenLoan Syndicationcybertron cafeNoch keine Bewertungen

- Patnership Act Companies Act Co-Operative Societies Act Limited Liability PatnershipDokument14 SeitenPatnership Act Companies Act Co-Operative Societies Act Limited Liability Patnershipneenu georgeNoch keine Bewertungen

- Lending Policies of Indian BanksDokument47 SeitenLending Policies of Indian BanksProf Dr Chowdari Prasad80% (5)

- Loan Syndication-Structure, Pricing and Deal MakingDokument30 SeitenLoan Syndication-Structure, Pricing and Deal Makingjaya100% (7)

- Credit Rating ProcessDokument36 SeitenCredit Rating ProcessBhuvi SharmaNoch keine Bewertungen

- AifDokument39 SeitenAifRaviYamijalaNoch keine Bewertungen

- Financing Small and Medium-Sized Enterprises in Asia and the Pacific: Credit Guarantee SchemesVon EverandFinancing Small and Medium-Sized Enterprises in Asia and the Pacific: Credit Guarantee SchemesNoch keine Bewertungen

- Loan SyndicationDokument30 SeitenLoan SyndicationMegha BhatnagarNoch keine Bewertungen

- Non Convertible DebenturesDokument3 SeitenNon Convertible DebenturesAbhinav AroraNoch keine Bewertungen

- Institute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingDokument3 SeitenInstitute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingS100% (2)

- ABL Asset-Based Lending Guide April 2015Dokument20 SeitenABL Asset-Based Lending Guide April 2015Venp PeNoch keine Bewertungen

- 2 Principles+of+LendingDokument25 Seiten2 Principles+of+LendingBratati SahooNoch keine Bewertungen

- Bank of Uganda Releases Agent Banking RegulationsDokument2 SeitenBank of Uganda Releases Agent Banking RegulationspokechoNoch keine Bewertungen

- Transfer and Transmission of SharesDokument6 SeitenTransfer and Transmission of SharesshanumanuranuNoch keine Bewertungen

- Bank GuaranteesDokument16 SeitenBank GuaranteesViji RangaNoch keine Bewertungen

- Banker-Customer RelationshipDokument17 SeitenBanker-Customer RelationshipAdharsh VenkatesanNoch keine Bewertungen

- Sources of FinanceDokument25 SeitenSources of FinanceNehaNoch keine Bewertungen

- BVCA Model Term Sheet For A Series A Round - Sept 2015Dokument15 SeitenBVCA Model Term Sheet For A Series A Round - Sept 2015GabrielaNoch keine Bewertungen

- Understanding Term SheetDokument5 SeitenUnderstanding Term Sheetgvs_2000Noch keine Bewertungen

- Loan SyndicationDokument36 SeitenLoan SyndicationSatish Tiwari100% (1)

- Unit 05 - Principles of Bank LendingDokument18 SeitenUnit 05 - Principles of Bank LendingSayak GhoshNoch keine Bewertungen

- Draft Share Pledge AgreementDokument10 SeitenDraft Share Pledge AgreementMuneeb Ahmed ShiekhNoch keine Bewertungen

- Role of Merchant Banker in IPODokument27 SeitenRole of Merchant Banker in IPOAmbily S Kumar67% (3)

- Group 3Dokument9 SeitenGroup 3eranyigiNoch keine Bewertungen

- Loan Syndication Ti OnDokument11 SeitenLoan Syndication Ti Onhayden28Noch keine Bewertungen

- Chapter 2Dokument21 SeitenChapter 2fentawmelaku1993Noch keine Bewertungen

- Report On Funds RaisingDokument28 SeitenReport On Funds RaisingNikita MajiNoch keine Bewertungen

- Credit Card FraudsDokument63 SeitenCredit Card FraudsAnaghaPuranikNoch keine Bewertungen

- Badla MechanismDokument27 SeitenBadla Mechanismdivyapillai0201_Noch keine Bewertungen

- Different Post-Office For Small Savings Schemes Are As Follows: 1. Post-Office Saving AccountDokument6 SeitenDifferent Post-Office For Small Savings Schemes Are As Follows: 1. Post-Office Saving Accountdivyapillai0201_Noch keine Bewertungen

- Chapter No: 1Dokument29 SeitenChapter No: 1divyapillai0201_Noch keine Bewertungen

- BCG Matrix of BritanniaDokument37 SeitenBCG Matrix of Britanniadivyapillai0201_100% (1)

- Chapter No: 1: Bank of Bengal H.O. EstablishmentDokument33 SeitenChapter No: 1: Bank of Bengal H.O. Establishmentdivyapillai0201_Noch keine Bewertungen

- B) Quote For TrademarkDokument1 SeiteB) Quote For TrademarkKawrw DgedeaNoch keine Bewertungen

- D Tomlinson Retail Seeks Your Assistance in Developing Cash andDokument1 SeiteD Tomlinson Retail Seeks Your Assistance in Developing Cash andAmit PandeyNoch keine Bewertungen

- LSNZ Combo Brochure 2007Dokument4 SeitenLSNZ Combo Brochure 2007Joins 세계유학Noch keine Bewertungen

- FinalONLINE TRANSACTION INDEXDokument2 SeitenFinalONLINE TRANSACTION INDEXLaraya, Roy MatthewNoch keine Bewertungen

- Golden Book of Accounting Finance Interviews Part I Site Version V 1.0 PDFDokument62 SeitenGolden Book of Accounting Finance Interviews Part I Site Version V 1.0 PDFRAJESH M S100% (2)

- Midterm Exam in Traffic Management and Accident Investigation Multiple ChoiceDokument5 SeitenMidterm Exam in Traffic Management and Accident Investigation Multiple ChoiceRemo Octaviano63% (8)

- Bhagwat Group CorporationDokument10 SeitenBhagwat Group CorporationPrabin KumarNoch keine Bewertungen

- HARP 2.0 Freddie Open Access Relief UnlimitedDokument4 SeitenHARP 2.0 Freddie Open Access Relief UnlimitedAccessLendingNoch keine Bewertungen

- Screenshot 2022-02-24 at 10.08.07Dokument4 SeitenScreenshot 2022-02-24 at 10.08.07Katia allen0% (1)

- China Bank Credit Card Application Form PDFDokument2 SeitenChina Bank Credit Card Application Form PDFJon SantiagoNoch keine Bewertungen

- 1) Permanent Audit File IndexDokument6 Seiten1) Permanent Audit File IndexPurnamaAjiNoch keine Bewertungen

- HELB Loan DisbursementDokument3 SeitenHELB Loan DisbursementIbrahim jewaNoch keine Bewertungen

- MULTIPLE CHOICE. Choose The One Alternative That Best Completes The Statement or Answers The QuestionDokument3 SeitenMULTIPLE CHOICE. Choose The One Alternative That Best Completes The Statement or Answers The QuestionMohammad Abu LailNoch keine Bewertungen

- New Brochure Tpc2Dokument2 SeitenNew Brochure Tpc2Hone DarkroseNoch keine Bewertungen

- Transaction HistoryDokument3 SeitenTransaction HistorysomeshleocolaNoch keine Bewertungen

- M73 Osbo1023 01 Se CH73Dokument10 SeitenM73 Osbo1023 01 Se CH73prexiebubblesNoch keine Bewertungen

- Rammandir Sedam Road Corridor: Last Mile Connectivity in Kalaburagi City On The TODokument25 SeitenRammandir Sedam Road Corridor: Last Mile Connectivity in Kalaburagi City On The TOSachin GopagoniwarNoch keine Bewertungen

- Posting Areas Brim - AccountsDokument14 SeitenPosting Areas Brim - AccountsSourav Kumar JenaNoch keine Bewertungen

- 03 Senior Civil Judge OcrDokument23 Seiten03 Senior Civil Judge OcrHemendra KapadiaNoch keine Bewertungen

- Sudu20297alus0pk PDFDokument4 SeitenSudu20297alus0pk PDFEli Cuero MadridNoch keine Bewertungen

- Verified by Visa Acquirer Merchant Implementation GuideDokument114 SeitenVerified by Visa Acquirer Merchant Implementation GuideyadbhavishyaNoch keine Bewertungen

- Unit 3 CDokument14 SeitenUnit 3 Cmusic niNoch keine Bewertungen

- Indeminity BondDokument3 SeitenIndeminity BondAli KhanNoch keine Bewertungen

- Antena 4g CajxbalatiDokument9 SeitenAntena 4g Cajxbalatiest.mbsandroNoch keine Bewertungen

- Unit 4, Pharmaceutical Engineering, B Pharmacy 3rd Sem, Carewell PharmaDokument20 SeitenUnit 4, Pharmaceutical Engineering, B Pharmacy 3rd Sem, Carewell Pharmaohayo3590Noch keine Bewertungen

- 0731 I K JG 000169791Dokument1 Seite0731 I K JG 000169791Fikri FarhanNoch keine Bewertungen

- Cash and CE Problems ExercisesDokument3 SeitenCash and CE Problems ExercisesMa. Erika Charisse DacerNoch keine Bewertungen

- Attach SignalingDokument44 SeitenAttach Signalingbrr.rezvaniNoch keine Bewertungen

- SW and ASSIGNMENT - TUGOTDokument9 SeitenSW and ASSIGNMENT - TUGOTAndrea TugotNoch keine Bewertungen

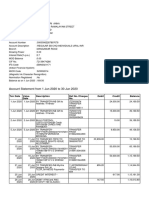

- Account Statement From 1 Jun 2020 To 30 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument2 SeitenAccount Statement From 1 Jun 2020 To 30 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAnil KumarNoch keine Bewertungen