Das könnte Ihnen auch gefallen

- Nightclub PDFDokument32 SeitenNightclub PDFFrank GallardoNoch keine Bewertungen

- Reservoir Engineers Competency Matrix - Society of Petroleum EngineersDokument5 SeitenReservoir Engineers Competency Matrix - Society of Petroleum Engineersbillal_m_aslamNoch keine Bewertungen

- Environment VocabDokument2 SeitenEnvironment VocabIrene Teach50% (2)

- 3ADI+ Report Tanzania Palm Oil VC Diagnostics and Action PlanDokument121 Seiten3ADI+ Report Tanzania Palm Oil VC Diagnostics and Action PlanAsaph DanielNoch keine Bewertungen

- Broker Business Plan TemplateDokument23 SeitenBroker Business Plan TemplateLestijono Last100% (1)

- Agricultural Lending-A How To GuideDokument136 SeitenAgricultural Lending-A How To GuideQuantmetrixNoch keine Bewertungen

- Poultry Farm Project: Feasibility StudyDokument30 SeitenPoultry Farm Project: Feasibility StudySelam93% (27)

- Guidelines On Farm Value Chain Development Through Promotion of Producers Enterprise Under NRETPDokument14 SeitenGuidelines On Farm Value Chain Development Through Promotion of Producers Enterprise Under NRETPSreekanth reddyNoch keine Bewertungen

- Oil and Gas Training Courses Catalog 2016Dokument358 SeitenOil and Gas Training Courses Catalog 2016Amit Prajapati100% (1)

- CDU Training PowerpointDokument144 SeitenCDU Training Powerpointviettanct92% (13)

- Differential Liberation PVT Fluid TestDokument11 SeitenDifferential Liberation PVT Fluid TestAhmed M. Saad0% (1)

- BiodieselDokument42 SeitenBiodieselFachrurrozi IyunkNoch keine Bewertungen

- China Pastry Bread Market ReportDokument10 SeitenChina Pastry Bread Market ReportAllChinaReports.comNoch keine Bewertungen

- Crude Palm OilDokument19 SeitenCrude Palm OilmarpadanNoch keine Bewertungen

- Edible Oil SourcesDokument22 SeitenEdible Oil Sourcesshym hjrNoch keine Bewertungen

- Castor Oil Report Preview EbookDokument30 SeitenCastor Oil Report Preview EbookBolly Dou100% (1)

- Bakes and Confectinoeries Internship Project ReportDokument29 SeitenBakes and Confectinoeries Internship Project ReportRadhika RuhyNoch keine Bewertungen

- Twinkle Palm Oil Ventures Set to Redefine Standard Palm Oil ProcessingDokument35 SeitenTwinkle Palm Oil Ventures Set to Redefine Standard Palm Oil ProcessingMumtahinaNoch keine Bewertungen

- Indian Edible Oil Industry: Types of Oils Commonly in Use in IndiaDokument11 SeitenIndian Edible Oil Industry: Types of Oils Commonly in Use in IndiaMani BmvNoch keine Bewertungen

- Mother Dairy Fruit and Vegetable PVTDokument49 SeitenMother Dairy Fruit and Vegetable PVTAadietya SinhaNoch keine Bewertungen

- Edible Oil Sector (Industry Analysis)Dokument8 SeitenEdible Oil Sector (Industry Analysis)Umair AyazNoch keine Bewertungen

- Sunflower SectorDokument30 SeitenSunflower SectorMedard SottaNoch keine Bewertungen

- Final Niger Seed Edible Oil Semi Refinery Plant B.P.WDokument60 SeitenFinal Niger Seed Edible Oil Semi Refinery Plant B.P.WIjaaraa SabaaNoch keine Bewertungen

- MARKETING Strategy and Campaign PLANDokument38 SeitenMARKETING Strategy and Campaign PLANRediet Tsigeberhan100% (1)

- Proposal On FarDokument21 SeitenProposal On FarRas Abel BekeleNoch keine Bewertungen

- Erikum Multipurpose Farmer's Cooperatives Union: June, 2012Dokument27 SeitenErikum Multipurpose Farmer's Cooperatives Union: June, 2012Helen Shumay100% (1)

- Alb Ani A LeatherDokument40 SeitenAlb Ani A LeatherkoyluNoch keine Bewertungen

- BS A1.1-FinalDokument44 SeitenBS A1.1-FinalNaNóngNảyNoch keine Bewertungen

- Project Finance Assignment Group 2Dokument11 SeitenProject Finance Assignment Group 2Firaol TufaaNoch keine Bewertungen

- Annual Report 2006-07 HPCLDokument164 SeitenAnnual Report 2006-07 HPCLnishantNoch keine Bewertungen

- Appendix 1-MFV Economic Analysis Peer ReviewDokument56 SeitenAppendix 1-MFV Economic Analysis Peer ReviewAlícia AlmeidaNoch keine Bewertungen

- Atanasov GjorgjiDokument49 SeitenAtanasov GjorgjiSoorsri T SNoch keine Bewertungen

- 3 Marketing StrategyDokument83 Seiten3 Marketing StrategyMengsteNoch keine Bewertungen

- NALF Labor Union 2Dokument20 SeitenNALF Labor Union 2Tesfaye ejetaNoch keine Bewertungen

- 2020 Guidelines For The Administration and Utilization of The Mic Taf - FinalDokument29 Seiten2020 Guidelines For The Administration and Utilization of The Mic Taf - FinalInonge Mary SimakumbaNoch keine Bewertungen

- John Erick G. Dineros Final Project (1st Quarter)Dokument11 SeitenJohn Erick G. Dineros Final Project (1st Quarter)John Erick DinerosNoch keine Bewertungen

- Business Plan Green Light LEDDokument58 SeitenBusiness Plan Green Light LEDGanesh Srinivasan100% (1)

- Haryana's New Industrial Investment Policy 2015Dokument72 SeitenHaryana's New Industrial Investment Policy 2015Miniswar KosanaNoch keine Bewertungen

- Marketing Plan LG in Egypt Ahmed Draft0Dokument74 SeitenMarketing Plan LG in Egypt Ahmed Draft0ahmedmae100% (1)

- Marketing PlanDokument148 SeitenMarketing PlanalinnaeNoch keine Bewertungen

- Business Planning GuideDokument86 SeitenBusiness Planning GuideMohamed Ahmed ElgazzarNoch keine Bewertungen

- Organic Farm Business PlanDokument30 SeitenOrganic Farm Business PlanJosh tubeNoch keine Bewertungen

- International Innovators Business PlanDokument35 SeitenInternational Innovators Business PlansatyamehtaNoch keine Bewertungen

- Kedir Tume Feasibility Study FinalDokument47 SeitenKedir Tume Feasibility Study FinalNuredin GebeyehuNoch keine Bewertungen

- Guidance-COSP ENDokument28 SeitenGuidance-COSP ENJeny EcheverriaNoch keine Bewertungen

- Bajaj Auto Salesforce StrategyDokument18 SeitenBajaj Auto Salesforce Strategym omprakashNoch keine Bewertungen

- Competition Authority of Kenya Strategic Plan 201718 - 202021-MinDokument62 SeitenCompetition Authority of Kenya Strategic Plan 201718 - 202021-MinMark NjoguNoch keine Bewertungen

- M004lon - End of Module AssessmentDokument17 SeitenM004lon - End of Module AssessmentRobert Z. SonkarlayNoch keine Bewertungen

- Karnataka Industrial Policy 2014-19 Final Draft SummaryDokument72 SeitenKarnataka Industrial Policy 2014-19 Final Draft SummarysidrubNoch keine Bewertungen

- Managingbenefits GuidanceDokument52 SeitenManagingbenefits Guidancetitli123Noch keine Bewertungen

- Greenhouse Business Plan - LmagnetDokument10 SeitenGreenhouse Business Plan - LmagnetShurinzNoch keine Bewertungen

- Soap and Detergent ProductionDokument33 SeitenSoap and Detergent ProductionSabrina Abdurahman100% (4)

- Impact of Merger On Financial ProfitabilityDokument25 SeitenImpact of Merger On Financial ProfitabilityganeshadhikariNoch keine Bewertungen

- Guidelines For The Value Chain Fund: AgrobigDokument42 SeitenGuidelines For The Value Chain Fund: Agrobigabel_kayelNoch keine Bewertungen

- Adventure TravelDokument35 SeitenAdventure TravelArsimNoch keine Bewertungen

- Hico Ice Cream Full Master File Swot, Pestel, ETCDokument23 SeitenHico Ice Cream Full Master File Swot, Pestel, ETCPlus Plus100% (2)

- Project: 13040029 Emba 2013Dokument10 SeitenProject: 13040029 Emba 2013Fazal4822Noch keine Bewertungen

- Cross-Partner+Seed+Sector+Study PublicDokument27 SeitenCross-Partner+Seed+Sector+Study PublicEzra EazyNoch keine Bewertungen

- B2B Assignment by Mustafa JamaliDokument12 SeitenB2B Assignment by Mustafa JamalimustafaNoch keine Bewertungen

- RFQ 2021-03-MS Annex A Terms of Reference - Ver2021.02.22Dokument9 SeitenRFQ 2021-03-MS Annex A Terms of Reference - Ver2021.02.22HiraNoch keine Bewertungen

- Alim Proposed A Strategic Plan For EasyJet According To Its Strengths, Weaknesses and The Opportunities and Threats in The Airline MarketDokument51 SeitenAlim Proposed A Strategic Plan For EasyJet According To Its Strengths, Weaknesses and The Opportunities and Threats in The Airline MarketMary Konaté93% (15)

- Important Notice:: DisclaimerDokument45 SeitenImportant Notice:: DisclaimerJummy BMSNoch keine Bewertungen

- Logistics - BP SampleDokument23 SeitenLogistics - BP SamplePro Business Plans100% (1)

- Curve Plus Format 2Dokument34 SeitenCurve Plus Format 2JUN RODOLF JAMORANoch keine Bewertungen

- Report On Market Ting Management Final MbaDokument26 SeitenReport On Market Ting Management Final MbawaqaskhNoch keine Bewertungen

- Ranchi Building Permit MemoDokument2 SeitenRanchi Building Permit MemoMohit JalanNoch keine Bewertungen

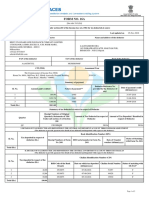

- Form No. 16A: From ToDokument2 SeitenForm No. 16A: From ToAkriti JhaNoch keine Bewertungen

- Indian Institute of Management AhmedabadDokument4 SeitenIndian Institute of Management AhmedabadMohit JalanNoch keine Bewertungen

- Neft Rtgs FormDokument1 SeiteNeft Rtgs FormMohit Jalan100% (1)

- Indian Institute of Management AhmedabadDokument4 SeitenIndian Institute of Management AhmedabadMohit JalanNoch keine Bewertungen

- TDS Deduction GuideDokument35 SeitenTDS Deduction GuideBj Thivagar0% (2)

- BBG RetailDokument16 SeitenBBG RetailRamesh GoudNoch keine Bewertungen

- Product Data Sheet - BIRKOSIT Dichtungskitt ®Dokument2 SeitenProduct Data Sheet - BIRKOSIT Dichtungskitt ®Le Thanh HaiNoch keine Bewertungen

- A Study On Reasons and Effects of Hike in Petrol PricesDokument2 SeitenA Study On Reasons and Effects of Hike in Petrol PricesInternational Journal of Innovative Science and Research TechnologyNoch keine Bewertungen

- Viscosity Index - : Page 1 of 4 Attachment To Report 51479Dokument4 SeitenViscosity Index - : Page 1 of 4 Attachment To Report 51479dassi990% (1)

- Circular Economy 01Dokument16 SeitenCircular Economy 01doxa mariaNoch keine Bewertungen

- GhanaDokument44 SeitenGhanaJohnnie HarrisonNoch keine Bewertungen

- Hydraulic Cat 117Dokument160 SeitenHydraulic Cat 117Renee MabbottNoch keine Bewertungen

- AILE Catalog of Gas Station Fitting Parts PDFDokument72 SeitenAILE Catalog of Gas Station Fitting Parts PDFvikrantathavaleNoch keine Bewertungen

- Opportunities For Egyptian Investors and Industries in Uganda's Oil and Gas Industry - Concept NoteDokument6 SeitenOpportunities For Egyptian Investors and Industries in Uganda's Oil and Gas Industry - Concept NoteberyaugNoch keine Bewertungen

- Modular ConstructionDokument3 SeitenModular ConstructionsandeepNoch keine Bewertungen

- The Mystery of the Disappearing OilDokument10 SeitenThe Mystery of the Disappearing OilangelNoch keine Bewertungen

- Animal Fat Processing and Its Quality Control 2157 7110.1000252Dokument5 SeitenAnimal Fat Processing and Its Quality Control 2157 7110.1000252sarita choudharyNoch keine Bewertungen

- BP Stats Review 2021 All DataDokument624 SeitenBP Stats Review 2021 All Dataivan sudibyoNoch keine Bewertungen

- Drilling Cost Extracted From ODP Final VersionDokument3 SeitenDrilling Cost Extracted From ODP Final VersionAnh Tuan NguyenNoch keine Bewertungen

- D5236 Destilacion PostilDokument18 SeitenD5236 Destilacion PostilLuis Ernesto Marin JaimesNoch keine Bewertungen

- PC-1 Mock TestDokument5 SeitenPC-1 Mock TestkunalNoch keine Bewertungen

- RE1 Dr. Ayoub Assignment 2 John Kevin de CastroDokument2 SeitenRE1 Dr. Ayoub Assignment 2 John Kevin de CastroJohn Kevin de CastroNoch keine Bewertungen

- Orbis Export DATADokument22 SeitenOrbis Export DATAAnthony Arcilla PulhinNoch keine Bewertungen

- My Siwes ReportDokument71 SeitenMy Siwes ReportOrji Christian100% (2)

- Relative ValuationDokument3 SeitenRelative ValuationKhushbooNoch keine Bewertungen

- Astm D 91 - 02Dokument3 SeitenAstm D 91 - 02Edwin RamirezNoch keine Bewertungen

- International General Certificate Syllabus of Secondary Education Chemistry 0620 For Examination in June and November 2010Dokument37 SeitenInternational General Certificate Syllabus of Secondary Education Chemistry 0620 For Examination in June and November 2010Farouk O LionNoch keine Bewertungen

- Book 1Dokument61 SeitenBook 1suriyachackNoch keine Bewertungen

- Hysys 8.8 - ManualDokument606 SeitenHysys 8.8 - ManualCarlos Vaz88% (8)

- 2015 Gea Insight ZmagsDokument104 Seiten2015 Gea Insight ZmagsArvind ShuklaNoch keine Bewertungen

- Petrol Price HikeDokument30 SeitenPetrol Price HikeHimanshu Jatana100% (1)