Das könnte Ihnen auch gefallen

- Introduction to Negotiable Instruments: As per Indian LawsVon EverandIntroduction to Negotiable Instruments: As per Indian LawsBewertung: 5 von 5 Sternen5/5 (1)

- Types of stamps and concepts of stamp dutyDokument5 SeitenTypes of stamps and concepts of stamp dutyNikhil Kasat100% (2)

- Stamp DutiesDokument14 SeitenStamp Dutiessparsh9634100% (4)

- Stamp Duty CalculatorDokument2 SeitenStamp Duty Calculatorjmathew_984887Noch keine Bewertungen

- Stamp Duties Act 15 of 1993Dokument40 SeitenStamp Duties Act 15 of 1993André Le Roux100% (4)

- RemittanceDokument3 SeitenRemittanceSalman Abrar100% (2)

- The Stamp Act of 1899Dokument91 SeitenThe Stamp Act of 1899Muhammad Irfan RiazNoch keine Bewertungen

- United States Stam 00 Unit RichDokument40 SeitenUnited States Stam 00 Unit RichAnonymous 5dtQnfKeTq88% (8)

- Postal Power - The UPU (Universal Postal Union) in Berne, SwitzerlandDokument11 SeitenPostal Power - The UPU (Universal Postal Union) in Berne, SwitzerlandLisa Montgomery100% (9)

- Negotiable Instruments LawDokument33 SeitenNegotiable Instruments LawEj Clemena100% (1)

- Definition of 'Endorsement' and Types of EndorsementsDokument5 SeitenDefinition of 'Endorsement' and Types of EndorsementsMohib Ali100% (1)

- Negotiable Instruments 1229854285942730 1Dokument59 SeitenNegotiable Instruments 1229854285942730 1Sameer Gopal100% (1)

- Stamps Duties ActDokument62 SeitenStamps Duties Actreine_jongNoch keine Bewertungen

- Stamp Act RulesDokument61 SeitenStamp Act RulesKaran AggarwalNoch keine Bewertungen

- United States Stamp DutiesDokument18 SeitenUnited States Stamp DutiesMichael Focia86% (29)

- How to correctly complete a bill of exchangeDokument2 SeitenHow to correctly complete a bill of exchangeVũ Nguyễn100% (1)

- Negotiable Instruments ActDokument34 SeitenNegotiable Instruments Actx2Noch keine Bewertungen

- Law of Negotiable Instruments ExplainedDokument24 SeitenLaw of Negotiable Instruments Explainedshiftn7100% (3)

- Universal Postal UnionDokument13 SeitenUniversal Postal Uniontylerdurdendutch100% (6)

- Bill of Exchange (Credit Instruments)Dokument12 SeitenBill of Exchange (Credit Instruments)Aziz ShaikhNoch keine Bewertungen

- Securities Exchange Act of 1934 - SEC - Gov PDFDokument371 SeitenSecurities Exchange Act of 1934 - SEC - Gov PDFKevin Liu100% (2)

- Stamp Duty RatesDokument2 SeitenStamp Duty RatessankettaranNoch keine Bewertungen

- Medallion ProceduresDokument8 SeitenMedallion Procedureswest_keys100% (2)

- 8 RemittanceDokument4 Seiten8 RemittanceSaif AzmanNoch keine Bewertungen

- How You Funded Your Own Loan With a Promissory NoteDokument4 SeitenHow You Funded Your Own Loan With a Promissory Notesogunmola100% (7)

- Bill of Exchange Act 34 of 1964Dokument31 SeitenBill of Exchange Act 34 of 1964lifeisgrand100% (7)

- Acceptance Endorsement and Surrender Bill of LadingDokument28 SeitenAcceptance Endorsement and Surrender Bill of Ladingv100% (3)

- Instruments of PaymentDokument13 SeitenInstruments of Paymentnovelonash100% (4)

- Bills of ExchangeDokument5 SeitenBills of Exchangesara24391100% (3)

- Indian Stamp Act GuideDokument50 SeitenIndian Stamp Act GuidePraveen Jain100% (3)

- 31 USC 3123 Payment of Obligations and Interest On The Public DebtDokument1 Seite31 USC 3123 Payment of Obligations and Interest On The Public DebtBob JohnsonNoch keine Bewertungen

- Negotiable Instruments Act, 1881Dokument23 SeitenNegotiable Instruments Act, 1881Kansal Abhishek100% (1)

- How Does A Bill of Exchange Work?: Signed by The Person Giving It (Drawer)Dokument3 SeitenHow Does A Bill of Exchange Work?: Signed by The Person Giving It (Drawer)asif abdullah78% (9)

- CCCCC CCC: Negotiation AND EndorsementDokument22 SeitenCCCCC CCC: Negotiation AND EndorsementAnkita Maity100% (5)

- Bill of ExchangeDokument4 SeitenBill of ExchangeChetan SapraNoch keine Bewertungen

- Business Law 8th Edition Cheeseman Test BankDokument15 SeitenBusiness Law 8th Edition Cheeseman Test Banknuxurec83% (6)

- Financing Foreign Trade and International Trade DocumentsDokument9 SeitenFinancing Foreign Trade and International Trade DocumentsStaidCasper100% (1)

- Understanding Bills of ExchangeDokument52 SeitenUnderstanding Bills of ExchangeParesh Vaviya91% (11)

- Negotiable Instruments GuideDokument12 SeitenNegotiable Instruments GuideNithyananda PatelNoch keine Bewertungen

- Accepted 4 Value ExplainedDokument59 SeitenAccepted 4 Value ExplainedKelly EllisNoch keine Bewertungen

- Holder in Due Course and Negotiable Instruments ArticleDokument55 SeitenHolder in Due Course and Negotiable Instruments ArticleCarrieonic0% (1)

- Outward Remittance GuideDokument205 SeitenOutward Remittance GuideGopi Chand100% (1)

- International Bill of Exchange and Promissory NotesDokument41 SeitenInternational Bill of Exchange and Promissory NotesW897% (36)

- Universal Postal UnionDokument13 SeitenUniversal Postal Uniongregaj7100% (13)

- Lawfully Yours: The Realm of Business, Government and LawVon EverandLawfully Yours: The Realm of Business, Government and LawNoch keine Bewertungen

- How to Make Your Credit Card Rights Work for You: Save MoneyVon EverandHow to Make Your Credit Card Rights Work for You: Save MoneyNoch keine Bewertungen

- Bank Instruments & Accounts Management: Detecting & Preventing Fraud: With Case Law, Tutorial Notes, Questions & AnswersVon EverandBank Instruments & Accounts Management: Detecting & Preventing Fraud: With Case Law, Tutorial Notes, Questions & AnswersNoch keine Bewertungen

- Stop! Illegal Predatory Lending: A Self-Help GuideVon EverandStop! Illegal Predatory Lending: A Self-Help GuideNoch keine Bewertungen

- The Artificial Person and the Color of Law: How to Take Back the "Consent"! Social Geometry of LifeVon EverandThe Artificial Person and the Color of Law: How to Take Back the "Consent"! Social Geometry of LifeBewertung: 4.5 von 5 Sternen4.5/5 (9)

- Land LawDokument17 SeitenLand LawDhruv MishraNoch keine Bewertungen

- Stamping of e ContractsDokument5 SeitenStamping of e ContractsRamya ThotiNoch keine Bewertungen

- Stamp DutyDokument6 SeitenStamp DutyBhavya SharmaNoch keine Bewertungen

- LAW 101-Introduction To Legal Reasoning-Marva KhanDokument8 SeitenLAW 101-Introduction To Legal Reasoning-Marva KhanMuhammad Irfan RiazNoch keine Bewertungen

- MIT14 01SCF11 Graph07 PDFDokument10 SeitenMIT14 01SCF11 Graph07 PDFMuhammad Irfan RiazNoch keine Bewertungen

- Rector's and Dean's Merit List - Fall 2015Dokument1 SeiteRector's and Dean's Merit List - Fall 2015Muhammad Irfan RiazNoch keine Bewertungen

- LAW 327-Strategic International Commercial Transactions-Khyzar HussainDokument12 SeitenLAW 327-Strategic International Commercial Transactions-Khyzar HussainMuhammad Irfan RiazNoch keine Bewertungen

- ACF 261 - Principle of FinanceDokument8 SeitenACF 261 - Principle of FinanceMuhammad Irfan RiazNoch keine Bewertungen

- Course Code Course Title Sec Resource Person Mon Tue WedDokument2 SeitenCourse Code Course Title Sec Resource Person Mon Tue WedMuhammad Irfan RiazNoch keine Bewertungen

- SSSHF2017 Datesheet NBDokument1 SeiteSSSHF2017 Datesheet NBMuhammad Irfan RiazNoch keine Bewertungen

- HIST210 ReadingList PDFDokument9 SeitenHIST210 ReadingList PDFpamin_sinNoch keine Bewertungen

- ANTH 100-Introduction To Cultural Anthropology-Sadaf AhmadDokument9 SeitenANTH 100-Introduction To Cultural Anthropology-Sadaf AhmadMuhammad Irfan RiazNoch keine Bewertungen

- SSSHF2017 Datesheet NBDokument1 SeiteSSSHF2017 Datesheet NBMuhammad Irfan RiazNoch keine Bewertungen

- FINAL MERIT LISTSDokument38 SeitenFINAL MERIT LISTSMuhammad Irfan RiazNoch keine Bewertungen

- FINAL MERIT LISTSDokument38 SeitenFINAL MERIT LISTSMuhammad Irfan RiazNoch keine Bewertungen

- Golove (1) InternationalLaw Spring2006 4Dokument37 SeitenGolove (1) InternationalLaw Spring2006 4Sapna KawatNoch keine Bewertungen

- LAW 210-Concept of Law-Angbeen Atif MirzaDokument8 SeitenLAW 210-Concept of Law-Angbeen Atif MirzaMuhammad Irfan RiazNoch keine Bewertungen

- SSC F 2017 Date Sheet NBDokument6 SeitenSSC F 2017 Date Sheet NBMuhammad Irfan RiazNoch keine Bewertungen

- Umt School of Law and Policy: Date Sheet For End Term ExaminationDokument6 SeitenUmt School of Law and Policy: Date Sheet For End Term ExaminationMuhammad Irfan RiazNoch keine Bewertungen

- SSSHF2017 Datesheet NBDokument1 SeiteSSSHF2017 Datesheet NBMuhammad Irfan RiazNoch keine Bewertungen

- International Law - de Burca (Spring 2013)Dokument16 SeitenInternational Law - de Burca (Spring 2013)Muhammad Irfan RiazNoch keine Bewertungen

- COL Outline Silberman 2010Dokument47 SeitenCOL Outline Silberman 2010Muhammad Irfan RiazNoch keine Bewertungen

- Lab1Start v5Dokument1 SeiteLab1Start v5Muhammad Irfan RiazNoch keine Bewertungen

- Program Date Course Code Course Title Section Resource Person Time SlotDokument1 SeiteProgram Date Course Code Course Title Section Resource Person Time SlotMuhammad Irfan RiazNoch keine Bewertungen

- BS Mathematics Spring 2017 (Nov 25)Dokument5 SeitenBS Mathematics Spring 2017 (Nov 25)Muhammad Irfan RiazNoch keine Bewertungen

- Law 220-Contract Law-Khyzar HussainDokument21 SeitenLaw 220-Contract Law-Khyzar HussainMuhammad Irfan RiazNoch keine Bewertungen

- Rector's and Dean's Merit List - Fall 2015Dokument1 SeiteRector's and Dean's Merit List - Fall 2015Muhammad Irfan RiazNoch keine Bewertungen

- Program Date Course Code Course Title Section Resource Person Time SlotDokument1 SeiteProgram Date Course Code Course Title Section Resource Person Time SlotMuhammad Irfan RiazNoch keine Bewertungen

- Course Outline - TCLDokument4 SeitenCourse Outline - TCLMuhammad Irfan RiazNoch keine Bewertungen

- Immigration Outline Rodriguez 2010Dokument48 SeitenImmigration Outline Rodriguez 2010Muhammad Irfan RiazNoch keine Bewertungen

- Summary For Affiliated Colleges and Private Candidates - 13!03!2017Dokument1 SeiteSummary For Affiliated Colleges and Private Candidates - 13!03!2017Muhammad Irfan RiazNoch keine Bewertungen

- LAW 470-Evidence-Justice Fazal KarimDokument16 SeitenLAW 470-Evidence-Justice Fazal Karimalihassangzr100% (1)

- MIT4 241JS13 Handout2Dokument3 SeitenMIT4 241JS13 Handout2Muhammad Irfan RiazNoch keine Bewertungen

- F 1099 ADokument6 SeitenF 1099 AIRS100% (1)

- Financial PlanningDokument18 SeitenFinancial PlanningckzeoNoch keine Bewertungen

- Unit 4 Payment Systems PDFDokument48 SeitenUnit 4 Payment Systems PDFmuskanNoch keine Bewertungen

- Accounting 2 - 4rd ModuleDokument4 SeitenAccounting 2 - 4rd ModuleJessalyn Sarmiento TancioNoch keine Bewertungen

- Finance Current Affairs January Week IiDokument24 SeitenFinance Current Affairs January Week IiBhav MathurNoch keine Bewertungen

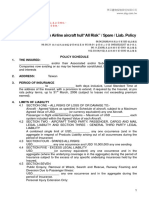

- Airline Aircraft Hull All Risk Spare Liab Policy BrochureDokument27 SeitenAirline Aircraft Hull All Risk Spare Liab Policy BrochureZoran DimitrijevicNoch keine Bewertungen

- Customer Satisfaction IndexDokument25 SeitenCustomer Satisfaction IndexPrateek DeepNoch keine Bewertungen

- Bank RakyatDokument18 SeitenBank RakyatnurulkhalidaNoch keine Bewertungen

- Executive Summary of Internet Banking Risks and OpportunitiesDokument13 SeitenExecutive Summary of Internet Banking Risks and OpportunitiesJaydeep DhandhaliyaNoch keine Bewertungen

- w01 Examination Guide For Exams Up To 30 April 2015Dokument23 Seitenw01 Examination Guide For Exams Up To 30 April 2015Arun MohanNoch keine Bewertungen

- Complaint With Exhibit FinalDokument97 SeitenComplaint With Exhibit FinalDeadspinNoch keine Bewertungen

- Implied Authority of A Partner: A Comparative Study: Assistant Professor of LawDokument20 SeitenImplied Authority of A Partner: A Comparative Study: Assistant Professor of LawHimanshuNoch keine Bewertungen

- Draft Policy On Special Freight Train Operator (SFTO) 1.0 GeneralDokument9 SeitenDraft Policy On Special Freight Train Operator (SFTO) 1.0 GeneralcpadhiNoch keine Bewertungen

- Study On Credit PolicyDokument12 SeitenStudy On Credit PolicyVaibhav GawandeNoch keine Bewertungen

- Fi Annual 16Dokument198 SeitenFi Annual 16sanchita sharmaNoch keine Bewertungen

- FHA Loans GuideDokument5 SeitenFHA Loans GuideHollanderFinancialNoch keine Bewertungen

- 14 People Vs Puig and PorrasDokument2 Seiten14 People Vs Puig and PorrasPring SumNoch keine Bewertungen

- Symbol Company Name AGM Book Closure Date AGM Date AgendaDokument1 SeiteSymbol Company Name AGM Book Closure Date AGM Date AgendaKrishna SapkotaNoch keine Bewertungen

- Contractor GCC 2013Dokument142 SeitenContractor GCC 2013SCReddy0% (1)

- SCO-06 FeeSched Rev18Dokument1 SeiteSCO-06 FeeSched Rev18Marcelo VeronezNoch keine Bewertungen

- Edi - 20689603 - 20689603-Broker-Mrs Febylyn Rodrigue-07 - 04 - 2018-pdx35439512 PDFDokument6 SeitenEdi - 20689603 - 20689603-Broker-Mrs Febylyn Rodrigue-07 - 04 - 2018-pdx35439512 PDFVenis ManahanNoch keine Bewertungen

- Oil & Gas Mini MBA 19-30 March 2012 - Registration Form MacameDokument1 SeiteOil & Gas Mini MBA 19-30 March 2012 - Registration Form Macamethemak76Noch keine Bewertungen

- Fraud Through DefalcationDokument28 SeitenFraud Through DefalcationRaj IslamNoch keine Bewertungen

- 1558035837508gtwf3RUDP4SoBRDQ PDFDokument1 Seite1558035837508gtwf3RUDP4SoBRDQ PDFEmba MadrasNoch keine Bewertungen

- Application Forms, Financial Results, EMI Calculator and MoreDokument21 SeitenApplication Forms, Financial Results, EMI Calculator and MoreRohanTheGreatNoch keine Bewertungen

- Forensic Investigation - ReportDokument6 SeitenForensic Investigation - Reportjhon DavidNoch keine Bewertungen

- Rajghat Besant School Fees For New Students: 2018-19Dokument2 SeitenRajghat Besant School Fees For New Students: 2018-19Nikita AnandNoch keine Bewertungen

- Certificate PDFDokument28 SeitenCertificate PDFRecordTrac - City of OaklandNoch keine Bewertungen

- Asher Rapp BioDokument1 SeiteAsher Rapp BioarappmemNoch keine Bewertungen

- Sip Report - Bajaj MBADokument49 SeitenSip Report - Bajaj MBAGaurav MantalaNoch keine Bewertungen