Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- 10 Rules of CommerceDokument2 Seiten10 Rules of Commercesabiont92% (24)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- RCBC VS BdoDokument3 SeitenRCBC VS BdoPao InfanteNoch keine Bewertungen

- TutorialDokument9 SeitenTutorialNaailah نائلة MaudarunNoch keine Bewertungen

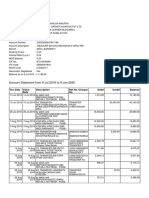

- Account Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument4 SeitenAccount Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancemauryapiaeNoch keine Bewertungen

- Economic Highlights - Foreign Exchange Reserves Rose To US$104.6bn As at 15 October - 25/10/2010Dokument2 SeitenEconomic Highlights - Foreign Exchange Reserves Rose To US$104.6bn As at 15 October - 25/10/2010Rhb InvestNoch keine Bewertungen

- Commodities & Currencies - Yet Another Sign of A Rebound On The Greenback - 25/10/2010Dokument3 SeitenCommodities & Currencies - Yet Another Sign of A Rebound On The Greenback - 25/10/2010Rhb InvestNoch keine Bewertungen

- RHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Dokument4 SeitenRHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Rhb InvestNoch keine Bewertungen

- RHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Dokument4 SeitenRHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Rhb InvestNoch keine Bewertungen

- Economic Highlights - Inflation Unexpectedly Eased in September - 25/10/2010Dokument3 SeitenEconomic Highlights - Inflation Unexpectedly Eased in September - 25/10/2010Rhb InvestNoch keine Bewertungen

- Corporate Highlights - 22/10/2010Dokument2 SeitenCorporate Highlights - 22/10/2010Rhb InvestNoch keine Bewertungen

- Rubber Glove Sector Update: Still Cautious On Near-Term Outlook - 21/10/2010Dokument2 SeitenRubber Glove Sector Update: Still Cautious On Near-Term Outlook - 21/10/2010Rhb InvestNoch keine Bewertungen

- British American Tobacco: Corporate HighlightsDokument4 SeitenBritish American Tobacco: Corporate HighlightsRhb InvestNoch keine Bewertungen

- Corporate Highlights - 21/10/2010Dokument2 SeitenCorporate Highlights - 21/10/2010Rhb InvestNoch keine Bewertungen

- RHB Equity 360° - 21 October 2010 (Media, Rubber Gloves, Puncak Niaga, WCT, Axis REIT, BAT Technical: AFG)Dokument4 SeitenRHB Equity 360° - 21 October 2010 (Media, Rubber Gloves, Puncak Niaga, WCT, Axis REIT, BAT Technical: AFG)Rhb InvestNoch keine Bewertungen

- Tracking The World Economy... - 19/10/2010Dokument3 SeitenTracking The World Economy... - 19/10/2010Rhb InvestNoch keine Bewertungen

- WCT Berhad: Secures RM1.36bn Building Job in Qatar and RM128m Hospital Project in Sabah - 21/10/2010Dokument3 SeitenWCT Berhad: Secures RM1.36bn Building Job in Qatar and RM128m Hospital Project in Sabah - 21/10/2010Rhb InvestNoch keine Bewertungen

- Puncak Niaga Berhad: Eyeing Hogenakkal Water Project in India - 21/10/2010Dokument2 SeitenPuncak Niaga Berhad: Eyeing Hogenakkal Water Project in India - 21/10/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights - Decline in Manufacturing Investment Approvals Narrowed in The 2Q - 20/10/2010Dokument3 SeitenEconomic Highlights - Decline in Manufacturing Investment Approvals Narrowed in The 2Q - 20/10/2010Rhb InvestNoch keine Bewertungen

- Axis REIT: Quattro West Started To Contribute - 21/10/2010Dokument3 SeitenAxis REIT: Quattro West Started To Contribute - 21/10/2010Rhb InvestNoch keine Bewertungen

- Motor Sector Update - Lower TIV On Shorter Working Month - 20/10/2010Dokument6 SeitenMotor Sector Update - Lower TIV On Shorter Working Month - 20/10/2010Rhb InvestNoch keine Bewertungen

- Quill Capita Trust: Flattish 3Q10 Numbers - 20/10/2010Dokument3 SeitenQuill Capita Trust: Flattish 3Q10 Numbers - 20/10/2010Rhb InvestNoch keine Bewertungen

- Economic Highlights - Leading Index Bounced Back in August, Pointing To A Resilient Economic Activities Ahead - 20/10/2010Dokument2 SeitenEconomic Highlights - Leading Index Bounced Back in August, Pointing To A Resilient Economic Activities Ahead - 20/10/2010Rhb InvestNoch keine Bewertungen

- RHB Equity 360° - 20 October 2010 (Property, Motor, Quill Capita Technical: Kump. Hartanah Selangor)Dokument3 SeitenRHB Equity 360° - 20 October 2010 (Property, Motor, Quill Capita Technical: Kump. Hartanah Selangor)Rhb InvestNoch keine Bewertungen

- RHB Equity 360° - 19 October 2010 (ILB, Public Bank Technical: Ann Joo)Dokument3 SeitenRHB Equity 360° - 19 October 2010 (ILB, Public Bank Technical: Ann Joo)Rhb InvestNoch keine Bewertungen

- Corporate Highlights - 19/10/2010Dokument2 SeitenCorporate Highlights - 19/10/2010Rhb InvestNoch keine Bewertungen

- Corporate Highlights - 20/10/2010Dokument2 SeitenCorporate Highlights - 20/10/2010Rhb InvestNoch keine Bewertungen

- RHB Equity 360° - 18 October 2010 (Budget, PLUS Technical: Axiata, CMS)Dokument3 SeitenRHB Equity 360° - 18 October 2010 (Budget, PLUS Technical: Axiata, CMS)Rhb InvestNoch keine Bewertungen

- Tracking The World Economy... - 18/10/2010Dokument2 SeitenTracking The World Economy... - 18/10/2010Rhb InvestNoch keine Bewertungen

- LONG QUIZ - Civil Law Review 2Dokument3 SeitenLONG QUIZ - Civil Law Review 2Vin DualbzNoch keine Bewertungen

- International Monetary FundDokument3 SeitenInternational Monetary FundanjaliNoch keine Bewertungen

- Assignment 1 IISDokument4 SeitenAssignment 1 IISZulqarnain KambohNoch keine Bewertungen

- Week 05 - Compendium V - Factoring & Forfaiting v3Dokument16 SeitenWeek 05 - Compendium V - Factoring & Forfaiting v3ximenaNoch keine Bewertungen

- Chief Executive Officer CEO Turnaround in San Diego CA Resume Robert CampbellDokument2 SeitenChief Executive Officer CEO Turnaround in San Diego CA Resume Robert CampbellRobertCampbell1Noch keine Bewertungen

- Corporate Presentation: L&T Finance Limited L&T Infrastructure Finance Company Limited L&T Investment Management LimitedDokument27 SeitenCorporate Presentation: L&T Finance Limited L&T Infrastructure Finance Company Limited L&T Investment Management LimitedBijendra SinghNoch keine Bewertungen

- Metropolitan Bank & Trust Co. Vs Junnel's Marketing CorporationDokument15 SeitenMetropolitan Bank & Trust Co. Vs Junnel's Marketing CorporationJulius ReyesNoch keine Bewertungen

- Account Closure RequestDokument2 SeitenAccount Closure Requestsankar22Noch keine Bewertungen

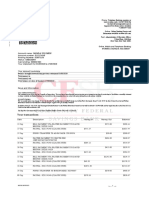

- Histori TransaksiDokument3 SeitenHistori TransaksiHari SusantoNoch keine Bewertungen

- Aarpa5489j 2019Dokument5 SeitenAarpa5489j 2019drali508482Noch keine Bewertungen

- A Critical Review of NPA in Indian Banking IndustryDokument12 SeitenA Critical Review of NPA in Indian Banking IndustryNavneet NandaNoch keine Bewertungen

- Negotiable Instruments Act 1881Dokument101 SeitenNegotiable Instruments Act 1881Bidyut Biplab DasNoch keine Bewertungen

- Mrs Janada Solomon 500 Laurel Lane, Midland, Texas 79701Dokument2 SeitenMrs Janada Solomon 500 Laurel Lane, Midland, Texas 79701SolomonNoch keine Bewertungen

- Final Thesis Report-Yilebes A Submitted To AAUDokument122 SeitenFinal Thesis Report-Yilebes A Submitted To AAUAhmed MohamedNoch keine Bewertungen

- Presented By:-Sumit Singal MBA-I (3129)Dokument34 SeitenPresented By:-Sumit Singal MBA-I (3129)Inderpreet SinghNoch keine Bewertungen

- 10 Myths About Financial DerivativesDokument6 Seiten10 Myths About Financial DerivativesArshad FahoumNoch keine Bewertungen

- A Case Study of Acquisition of Spice Communications by Isaasdaddea Cellular LimitedDokument13 SeitenA Case Study of Acquisition of Spice Communications by Isaasdaddea Cellular Limitedsarge1986Noch keine Bewertungen

- Ticketing Manual New 2011Dokument125 SeitenTicketing Manual New 2011Jonathan LiewNoch keine Bewertungen

- Industrial Finance ProjectDokument62 SeitenIndustrial Finance ProjectSantosh PawarNoch keine Bewertungen

- Conversor de Monedas en ExcelDokument5 SeitenConversor de Monedas en ExcelRaúl RivasNoch keine Bewertungen

- Associated Bank v. TanDokument1 SeiteAssociated Bank v. TanAngie JapitanNoch keine Bewertungen

- List of Consumer Reporting CompaniesDokument33 SeitenList of Consumer Reporting CompaniesAnaoj28Noch keine Bewertungen

- A Dollarization Blueprint For Argentina, Cato Foreign Policy Briefing No. 52Dokument25 SeitenA Dollarization Blueprint For Argentina, Cato Foreign Policy Briefing No. 52Cato InstituteNoch keine Bewertungen

- FTP MultiPeriod Pricing 2016 FinalProof DermineDokument12 SeitenFTP MultiPeriod Pricing 2016 FinalProof DermineSumair ChughtaiNoch keine Bewertungen

- Indian Stock Broking IndustryDokument49 SeitenIndian Stock Broking Industrysatya_choubisa89% (9)

- Balance of Payment MCQS: Economic & Social Issues - Multiple Choice QuestionsDokument12 SeitenBalance of Payment MCQS: Economic & Social Issues - Multiple Choice QuestionsIsmat100% (1)