Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Project Proposal TemplateDokument6 SeitenProject Proposal TemplateGomathiNoch keine Bewertungen

- Gusto Business Plan f16Dokument12 SeitenGusto Business Plan f16ChandanNoch keine Bewertungen

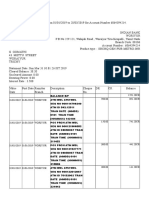

- Bank Reconciliation StatementDokument8 SeitenBank Reconciliation StatementDavidNoch keine Bewertungen

- Analysis AssignmentDokument3 SeitenAnalysis AssignmentmadyanoshieNoch keine Bewertungen

- DC Migration Case StudiesDokument3 SeitenDC Migration Case StudiesSalman SaluNoch keine Bewertungen

- Pure Logic GroupDokument28 SeitenPure Logic GroupPure Logic GroupNoch keine Bewertungen

- Multivariate Data Analysis Chapter 18 MCQDokument7 SeitenMultivariate Data Analysis Chapter 18 MCQThùyy VyNoch keine Bewertungen

- ENTREPRENEURSHIP: Filipino Businessman's SuccessDokument1 SeiteENTREPRENEURSHIP: Filipino Businessman's Successme meNoch keine Bewertungen

- ISO27k ISMS Mandatory Documentation Checklist Release 1v1Dokument29 SeitenISO27k ISMS Mandatory Documentation Checklist Release 1v1Ngo Hong QuangNoch keine Bewertungen

- TechnotronicsDokument1 SeiteTechnotronicsviral patelNoch keine Bewertungen

- Chapter 1Dokument12 SeitenChapter 1Jessica100% (1)

- Chapter 1 Ic 14 Development of Insurance Legislation in India and Insurance Act 1938Dokument30 SeitenChapter 1 Ic 14 Development of Insurance Legislation in India and Insurance Act 1938Jaswanth Singh RajpurohitNoch keine Bewertungen

- Tanishq Brand Research ProjectDokument70 SeitenTanishq Brand Research ProjectYashi Gupta0% (2)

- FAC3702 Question Bank 2015Dokument105 SeitenFAC3702 Question Bank 2015Itumeleng KekanaNoch keine Bewertungen

- Economics Problems PDFDokument31 SeitenEconomics Problems PDFev xvNoch keine Bewertungen

- J17 F6LSO Section B AnsDokument5 SeitenJ17 F6LSO Section B Ansaswathi1Noch keine Bewertungen

- Cir Vs Central Luzon Drug CorporationDokument2 SeitenCir Vs Central Luzon Drug CorporationVincent Quiña Piga71% (7)

- Gloria JeansDokument19 SeitenGloria Jeansfakethedoll50% (4)

- Bretton Woods Conference establishes IMF and World BankDokument3 SeitenBretton Woods Conference establishes IMF and World Banksam_64Noch keine Bewertungen

- Wholesalers N RetailersDokument7 SeitenWholesalers N RetailersDrRajdeep SinghNoch keine Bewertungen

- CSR-HRM Nexus: Defining The Role Engagement of The Human Resources ProfessionalsDokument9 SeitenCSR-HRM Nexus: Defining The Role Engagement of The Human Resources ProfessionalsDrRam Singh KambojNoch keine Bewertungen

- CIA OIG Audit Independent ContractorsDokument39 SeitenCIA OIG Audit Independent ContractorsJason Leopold100% (1)

- Contract ManagementDokument4 SeitenContract ManagementManish GuptaNoch keine Bewertungen

- Access Database Examples Download Able Sample DatabasesDokument5 SeitenAccess Database Examples Download Able Sample DatabasesNasha SaydNoch keine Bewertungen

- Price Promise Claim FormDokument2 SeitenPrice Promise Claim FormmichaelNoch keine Bewertungen

- Credit Monitoring in BankDokument40 SeitenCredit Monitoring in BankAGB AGB100% (1)

- Damas PDFDokument2 SeitenDamas PDFMartyna GiedriauskytėNoch keine Bewertungen

- Top ELSS Funds Annual Returns TrackerDokument31 SeitenTop ELSS Funds Annual Returns TrackerAli NadafNoch keine Bewertungen

- 09304001Dokument6 Seiten09304001AHMAD KAMIL MAKHTARNoch keine Bewertungen

- Salary (Proforma)Dokument15 SeitenSalary (Proforma)Joshua Capa FrondaNoch keine Bewertungen