Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- 8 Trdln0610saudiDokument40 Seiten8 Trdln0610saudiJad SoaiNoch keine Bewertungen

- Assertive Populism Od Dravidian PartiesDokument21 SeitenAssertive Populism Od Dravidian PartiesVeeramani ManiNoch keine Bewertungen

- Chapter 01 - PowerPoint - Introduction To Taxation in Canada - 2013Dokument32 SeitenChapter 01 - PowerPoint - Introduction To Taxation in Canada - 2013melsun007Noch keine Bewertungen

- Global Wealth Databook 2017Dokument165 SeitenGlobal Wealth Databook 2017Derek ZNoch keine Bewertungen

- Guide To Original Issue Discount (OID) Instruments: Publication 1212Dokument17 SeitenGuide To Original Issue Discount (OID) Instruments: Publication 1212Theplaymaker508Noch keine Bewertungen

- Internal Audit Checklist Sample PDFDokument3 SeitenInternal Audit Checklist Sample PDFFernando AguilarNoch keine Bewertungen

- The Political Economy of Communication (Second Edition)Dokument2 SeitenThe Political Economy of Communication (Second Edition)Trop JeengNoch keine Bewertungen

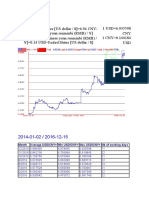

- Month Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysDokument3 SeitenMonth Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysZahid RizvyNoch keine Bewertungen

- Wedding BlissDokument16 SeitenWedding BlissThe Myanmar TimesNoch keine Bewertungen

- Chapter 6 - An Introduction To The Tourism Geography of EuroDokument12 SeitenChapter 6 - An Introduction To The Tourism Geography of EuroAnonymous 1ClGHbiT0JNoch keine Bewertungen

- Advantages and Disadvantages of Shares and DebentureDokument9 SeitenAdvantages and Disadvantages of Shares and Debenturekomal komal100% (1)

- Kotler - MarketingDokument25 SeitenKotler - Marketingermal880% (1)

- Us Cons Job Architecture 041315Dokument11 SeitenUs Cons Job Architecture 041315Karan Pratap Singh100% (1)

- GCCA Newsletter - FEBRUARY 2023Dokument1 SeiteGCCA Newsletter - FEBRUARY 2023ArnaldoFortiBattaginNoch keine Bewertungen

- Udai Pareek Scal For SES RuralDokument3 SeitenUdai Pareek Scal For SES Ruralopyadav544100% (1)

- Sim CBM 122 Lesson 3Dokument9 SeitenSim CBM 122 Lesson 3Andrew Sy ScottNoch keine Bewertungen

- Salary Slip Template V12Dokument5 SeitenSalary Slip Template V12Matthew NiñoNoch keine Bewertungen

- Anser Key For Class 8 Social Science SA 2 PDFDokument5 SeitenAnser Key For Class 8 Social Science SA 2 PDFSoumitraBagNoch keine Bewertungen

- Position PaperDokument2 SeitenPosition PaperMaria Marielle BucksNoch keine Bewertungen

- DPWH Natl Sewerage Septage MGMT ProgramDokument15 SeitenDPWH Natl Sewerage Septage MGMT Programclint castilloNoch keine Bewertungen

- MBBS MO OptionsDokument46 SeitenMBBS MO Optionskrishna madkeNoch keine Bewertungen

- TOEFLDokument15 SeitenTOEFLMega Suci LestariNoch keine Bewertungen

- Veit Tunel 1Dokument7 SeitenVeit Tunel 1Bladimir SolizNoch keine Bewertungen

- Statistical Appendix Economic Survey 2022-23Dokument217 SeitenStatistical Appendix Economic Survey 2022-23vijay krishnaNoch keine Bewertungen

- Ra 11057Dokument16 SeitenRa 11057Rio Sanchez100% (9)

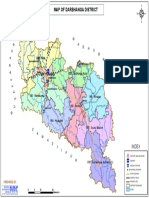

- DARBHANGA MapDokument1 SeiteDARBHANGA MapRISHIKESH ANANDNoch keine Bewertungen

- Module 1 GE 4 (Contemporary World)Dokument84 SeitenModule 1 GE 4 (Contemporary World)MARY MAXENE CAMELON BITARANoch keine Bewertungen

- Political Economy of Media - A Short IntroductionDokument5 SeitenPolitical Economy of Media - A Short Introductionmatthewhandy100% (1)

- Dennis Redmond Adorno MicrologiesDokument14 SeitenDennis Redmond Adorno MicrologiespatriceframbosaNoch keine Bewertungen

- Full Download Business in Action 6th Edition Bovee Solutions ManualDokument35 SeitenFull Download Business in Action 6th Edition Bovee Solutions Manuallincolnpatuc8100% (32)