Das könnte Ihnen auch gefallen

- Operating Leases-Incentives: SIC Interpretation 15Dokument4 SeitenOperating Leases-Incentives: SIC Interpretation 15Asis KoiralaNoch keine Bewertungen

- GCA Consultants: Introduction of The EuroDokument34 SeitenGCA Consultants: Introduction of The EuroNaeem MalikNoch keine Bewertungen

- 48 - Ifrs 03 bv2008Dokument203 Seiten48 - Ifrs 03 bv2008MK RKNoch keine Bewertungen

- IFRS03 BV2009 - Business CombinationsDokument144 SeitenIFRS03 BV2009 - Business CombinationsShaik Abdul Cader DawoodNoch keine Bewertungen

- Ias 17Dokument22 SeitenIas 17saad munirNoch keine Bewertungen

- ACS ProjectDokument31 SeitenACS Projectshanker_kNoch keine Bewertungen

- Sap 2 FinalDokument19 SeitenSap 2 FinalAndreiNoch keine Bewertungen

- Operating Leases-Incentives: SIC Interpretation 15Dokument1 SeiteOperating Leases-Incentives: SIC Interpretation 15Alexandra OanceNoch keine Bewertungen

- Sop 98-5Dokument14 SeitenSop 98-5chanti0999Noch keine Bewertungen

- IFRS 3 Business Combinations 2015Dokument208 SeitenIFRS 3 Business Combinations 2015Faye Dela TorreNoch keine Bewertungen

- Disclosure of Accounting PoliciesDokument7 SeitenDisclosure of Accounting PoliciesSatesh Kumar KonduruNoch keine Bewertungen

- Ias17 Bv2009 - LeasesDokument23 SeitenIas17 Bv2009 - Leasesdhani26Noch keine Bewertungen

- B8 Ipsas - 32 PDFDokument60 SeitenB8 Ipsas - 32 PDFEZEKIELNoch keine Bewertungen

- Disclosure of Accounting PoliciesDokument8 SeitenDisclosure of Accounting Policiesabdullah0331Noch keine Bewertungen

- Applying Rev RHC Mar 2015Dokument33 SeitenApplying Rev RHC Mar 2015Danik AstutikNoch keine Bewertungen

- Accounting Standard (AS) 1 (Issued 1979) : Disclosure of Accounting PoliciesDokument5 SeitenAccounting Standard (AS) 1 (Issued 1979) : Disclosure of Accounting PoliciesSuhasini GummeNoch keine Bewertungen

- 1 As Disclouser of Accounting PoliciesDokument6 Seiten1 As Disclouser of Accounting Policiesanisahemad1178Noch keine Bewertungen

- Module 5Dokument4 SeitenModule 5Karen GarciaNoch keine Bewertungen

- IFRS 3 - Business Combinations: History of The ProjectDokument13 SeitenIFRS 3 - Business Combinations: History of The ProjectGeoreyGNoch keine Bewertungen

- Leases: International Accounting Standard 17Dokument28 SeitenLeases: International Accounting Standard 17Dushyant ChouhanNoch keine Bewertungen

- Consolidated and Separate Financial Statements: International Accounting Standard 27Dokument41 SeitenConsolidated and Separate Financial Statements: International Accounting Standard 27davidwijaya1986Noch keine Bewertungen

- Depreciation & Inventory ValuationDokument9 SeitenDepreciation & Inventory ValuationDeepak KohliNoch keine Bewertungen

- Accounting Standard (AS) 1: (Issued 1979)Dokument7 SeitenAccounting Standard (AS) 1: (Issued 1979)anoop_mishra1986Noch keine Bewertungen

- IFRS 16 Leases (Repaired)Dokument19 SeitenIFRS 16 Leases (Repaired)Gana M. AyyashNoch keine Bewertungen

- Insurance Contracts: IFRS Standard 4Dokument30 SeitenInsurance Contracts: IFRS Standard 4Teja JurakNoch keine Bewertungen

- Deloitte Model Half Year Report 31dec2013Dokument75 SeitenDeloitte Model Half Year Report 31dec2013PhillipGaoNoch keine Bewertungen

- EY Applying Leases Apr2015Dokument53 SeitenEY Applying Leases Apr2015polkeastNoch keine Bewertungen

- Proposedamendtoifrs 3Dokument216 SeitenProposedamendtoifrs 3Avis Koh Wai LoonNoch keine Bewertungen

- As1 171222Dokument6 SeitenAs1 171222spikysanchitNoch keine Bewertungen

- As1-Diclosure of Accounting PoliciesDokument6 SeitenAs1-Diclosure of Accounting PoliciesDharmesh MistryNoch keine Bewertungen

- Isa 800Dokument11 SeitenIsa 800baabasaamNoch keine Bewertungen

- Chapter 3 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Dokument24 SeitenChapter 3 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din SheryarNoch keine Bewertungen

- IAS 8 - Accounting Policies, Changes in Accounting Estimates and ErrorsDokument7 SeitenIAS 8 - Accounting Policies, Changes in Accounting Estimates and ErrorsLeen LurNoch keine Bewertungen

- Disclosure of Accounting PoliciesDokument7 SeitenDisclosure of Accounting PoliciesgimmyjoyNoch keine Bewertungen

- CombinepdfDokument14 SeitenCombinepdfKen ZafraNoch keine Bewertungen

- CombinepdfDokument20 SeitenCombinepdfKen ZafraNoch keine Bewertungen

- Accounting Standard (AS) 1 (Issued 1979) : Disclosure of Accounting PoliciesDokument4 SeitenAccounting Standard (AS) 1 (Issued 1979) : Disclosure of Accounting Policiessaradindu123Noch keine Bewertungen

- NZ IAS 18 - RevenueDokument18 SeitenNZ IAS 18 - RevenueLutfia Nur AfifahNoch keine Bewertungen

- EY Applying Ifrs Presentation and Disclosure Requirements of Ifrs 15 October 2017Dokument51 SeitenEY Applying Ifrs Presentation and Disclosure Requirements of Ifrs 15 October 2017Jb AugustNoch keine Bewertungen

- Accounting Standards Board (ASB) in 1977Dokument15 SeitenAccounting Standards Board (ASB) in 1977Viswanathan SrkNoch keine Bewertungen

- Summary of Main Changes C. Act2014Dokument3 SeitenSummary of Main Changes C. Act2014mentinfusionNoch keine Bewertungen

- Ifrs Updates August 2019Dokument9 SeitenIfrs Updates August 2019obedNoch keine Bewertungen

- Reduction in Time Period of Financial StatementsDokument2 SeitenReduction in Time Period of Financial StatementsanjithNoch keine Bewertungen

- Wa0033.Dokument38 SeitenWa0033.Baqar BaigNoch keine Bewertungen

- B8 Ipsas - 32 - 0Dokument60 SeitenB8 Ipsas - 32 - 0Marius SteffyNoch keine Bewertungen

- Ifrs 4Dokument30 SeitenIfrs 4Cryptic LollNoch keine Bewertungen

- Date Development Comments: Reporting PublishedDokument4 SeitenDate Development Comments: Reporting PublishedJuan TañamorNoch keine Bewertungen

- Accounting StandardDokument13 SeitenAccounting StandardJohanna Pauline SequeiraNoch keine Bewertungen

- Accounting Standard 1Dokument7 SeitenAccounting Standard 1api-3828505Noch keine Bewertungen

- Interim Financial Reporting and Impairment: IFRIC Interpretation 10Dokument6 SeitenInterim Financial Reporting and Impairment: IFRIC Interpretation 10Matt PuaNoch keine Bewertungen

- ICAP TRsDokument45 SeitenICAP TRsSyed Azhar Abbas0% (1)

- Codification of Statements on Standards for Accounting and Review Services: Numbers 21-24Von EverandCodification of Statements on Standards for Accounting and Review Services: Numbers 21-24Noch keine Bewertungen

- Codification of Statements on Standards for Accounting and Review Services: Numbers 1 - 23Von EverandCodification of Statements on Standards for Accounting and Review Services: Numbers 1 - 23Noch keine Bewertungen

- Audit and Accounting Guide: Entities With Oil and Gas Producing Activities, 2018Von EverandAudit and Accounting Guide: Entities With Oil and Gas Producing Activities, 2018Noch keine Bewertungen

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsVon EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNoch keine Bewertungen

- Wiley GAAP for Governments 2016: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsVon EverandWiley GAAP for Governments 2016: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsNoch keine Bewertungen

- Partnership Act 1932Dokument20 SeitenPartnership Act 1932Cryptic Loll100% (1)

- Bangladesh Labour Laws 2006Dokument82 SeitenBangladesh Labour Laws 2006Cryptic LollNoch keine Bewertungen

- Company Act 1994Dokument31 SeitenCompany Act 1994Cryptic Loll100% (1)

- Trademarks Act 2009Dokument7 SeitenTrademarks Act 2009Mohammad Lutfor Rahaman KhanNoch keine Bewertungen

- N.I. Act 1881Dokument10 SeitenN.I. Act 1881Cryptic LollNoch keine Bewertungen

- Insurance Act 2010 (Theory) PDFDokument6 SeitenInsurance Act 2010 (Theory) PDFCryptic LollNoch keine Bewertungen

- Sale of Goods Act 1930Dokument24 SeitenSale of Goods Act 1930Cryptic LollNoch keine Bewertungen

- Bank Companies Act 1991 PDFDokument3 SeitenBank Companies Act 1991 PDFCryptic Loll0% (1)

- Worldcom: A Focus On Fraud and Inherent Risk AssessmentDokument4 SeitenWorldcom: A Focus On Fraud and Inherent Risk AssessmentCryptic LollNoch keine Bewertungen

- Arbitration Act 2001 PDFDokument11 SeitenArbitration Act 2001 PDFCryptic LollNoch keine Bewertungen

- Banking Companies Act 1991 Final PDFDokument5 SeitenBanking Companies Act 1991 Final PDFCryptic LollNoch keine Bewertungen

- Bangladesh Labour Laws 2006 (Definitions) PDFDokument7 SeitenBangladesh Labour Laws 2006 (Definitions) PDFCryptic LollNoch keine Bewertungen

- Insurance Act 2010 PDFDokument7 SeitenInsurance Act 2010 PDFCryptic Loll100% (1)

- Companies Act 1994 Final PDFDokument7 SeitenCompanies Act 1994 Final PDFCryptic LollNoch keine Bewertungen

- Bangladesh Labour Laws 2006 (Important) PDFDokument10 SeitenBangladesh Labour Laws 2006 (Important) PDFCryptic LollNoch keine Bewertungen

- 2 06 PDFDokument4 Seiten2 06 PDFCryptic LollNoch keine Bewertungen

- The Fund of Funds: A Focus On Fraud and Inherent Risk AssessmentDokument5 SeitenThe Fund of Funds: A Focus On Fraud and Inherent Risk AssessmentCryptic LollNoch keine Bewertungen

- 2 06 PDFDokument4 Seiten2 06 PDFCryptic LollNoch keine Bewertungen

- 2-05 2 PDFDokument4 Seiten2-05 2 PDFCryptic LollNoch keine Bewertungen

- Understanding The Client's Business and Industry: SectionDokument5 SeitenUnderstanding The Client's Business and Industry: SectionCryptic LollNoch keine Bewertungen

- Sunbeam: A Focus On Fraud and Inherent Risk Assessment: SynopsisDokument5 SeitenSunbeam: A Focus On Fraud and Inherent Risk Assessment: SynopsisCryptic LollNoch keine Bewertungen

- 2-05 2 PDFDokument4 Seiten2-05 2 PDFCryptic LollNoch keine Bewertungen

- Waste Management: A Focus On Fraud and Inherent Risk AssessmentDokument7 SeitenWaste Management: A Focus On Fraud and Inherent Risk AssessmentCryptic LollNoch keine Bewertungen

- Worldcom: A Focus On Professional Responsibility: SynopsisDokument4 SeitenWorldcom: A Focus On Professional Responsibility: SynopsisCryptic LollNoch keine Bewertungen

- 1 05Dokument5 Seiten1 05Tesfaye BelayeNoch keine Bewertungen

- The Fund of Funds: A Focus On Independence: SynopsisDokument4 SeitenThe Fund of Funds: A Focus On Independence: SynopsisCryptic LollNoch keine Bewertungen

- Waste Management: A Focus On Fraud and Inherent Risk AssessmentDokument7 SeitenWaste Management: A Focus On Fraud and Inherent Risk AssessmentCryptic LollNoch keine Bewertungen

- Enron: A Focus On Quality Assurance: SynopsisDokument5 SeitenEnron: A Focus On Quality Assurance: SynopsisCryptic LollNoch keine Bewertungen

- Waste Management: A Focus On Ethics and Due Professional CareDokument4 SeitenWaste Management: A Focus On Ethics and Due Professional CareCryptic LollNoch keine Bewertungen

- Index 2 PDFDokument30 SeitenIndex 2 PDFCryptic LollNoch keine Bewertungen

- Guidance - Note On Division III of Co's Act, 2013Dokument186 SeitenGuidance - Note On Division III of Co's Act, 2013rakhi100% (1)

- FZ5000 Solución Tarea 2 AJ2020Dokument2 SeitenFZ5000 Solución Tarea 2 AJ2020gerardoNoch keine Bewertungen

- Prosedur Dan Akibat Hukum Penundaan Kewajiban Pembayaran Utang Perseroan Terbatas (Studi Kasus Putusan Nomor 03/PKPU/2010/PN - Niaga.Sby)Dokument5 SeitenProsedur Dan Akibat Hukum Penundaan Kewajiban Pembayaran Utang Perseroan Terbatas (Studi Kasus Putusan Nomor 03/PKPU/2010/PN - Niaga.Sby)anindita putriNoch keine Bewertungen

- Negotiations, Deal StructuringDokument30 SeitenNegotiations, Deal StructuringVishakha PawarNoch keine Bewertungen

- Ifrs Example Interim Consolidated Financial Statements 2021Dokument46 SeitenIfrs Example Interim Consolidated Financial Statements 2021Kurt Leonard AlbaoNoch keine Bewertungen

- Project On Working Capital (OPTCL)Dokument66 SeitenProject On Working Capital (OPTCL)Prateek Anand33% (3)

- Chapter 4 - Forms of Business OrganizationDokument24 SeitenChapter 4 - Forms of Business Organizationairam cabadduNoch keine Bewertungen

- MercedesDokument138 SeitenMercedesMihaela DavidoaiaNoch keine Bewertungen

- GF Difference Between Private and Public Company Structure Under The Corporations ActDokument3 SeitenGF Difference Between Private and Public Company Structure Under The Corporations ActUbai M-pireNoch keine Bewertungen

- Business Valuations Business ValuationsDokument12 SeitenBusiness Valuations Business ValuationsAliNoch keine Bewertungen

- Asquith and Mullins 1983Dokument21 SeitenAsquith and Mullins 1983Angelie AngelNoch keine Bewertungen

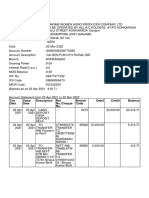

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDokument16 SeitenTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceTanu ParidaNoch keine Bewertungen

- CheatsheetDokument2 SeitenCheatsheetravapu345100% (1)

- The Following Information For CLH Company Is Available On June 30, 2018, The End of A MonthlyDokument5 SeitenThe Following Information For CLH Company Is Available On June 30, 2018, The End of A MonthlyJel SanNoch keine Bewertungen

- ACCTG 101 Final Quiz: Requirement: Provide The Necessary Journal EntriesDokument5 SeitenACCTG 101 Final Quiz: Requirement: Provide The Necessary Journal EntriesCalyx ImperialNoch keine Bewertungen

- Untitled DocumentDokument2 SeitenUntitled DocumentPeter Jun ParkNoch keine Bewertungen

- Mohammad Ali Jinnah University: Financial Accounting WorksheetDokument9 SeitenMohammad Ali Jinnah University: Financial Accounting WorksheetAsh LayNoch keine Bewertungen

- Not-for-Profit Organizations - Answers: Advanced Level Examination - Unit 08Dokument12 SeitenNot-for-Profit Organizations - Answers: Advanced Level Examination - Unit 08Dimuthu JayasuriyaNoch keine Bewertungen

- LongDokument3 SeitenLongKath ChuNoch keine Bewertungen

- LDD PT OlamDokument65 SeitenLDD PT OlamHubertus SetiawanNoch keine Bewertungen

- Soal Dan Jawaban Latihan Lab 1 - Home Office and Branch Office PDFDokument7 SeitenSoal Dan Jawaban Latihan Lab 1 - Home Office and Branch Office PDFPUTRI YANINoch keine Bewertungen

- Practice Material 1Dokument8 SeitenPractice Material 1Tine100% (1)

- Research Project (Finance) - Merger and AcquisitionDokument56 SeitenResearch Project (Finance) - Merger and AcquisitionKumar Harshit100% (1)

- Transmittal PhilhealthDokument7 SeitenTransmittal PhilhealthAnnette Aquino GuevarraNoch keine Bewertungen

- Incorporation Questionnaire For Startups From Orrick, Herrington & Sutcliffe LLPDokument9 SeitenIncorporation Questionnaire For Startups From Orrick, Herrington & Sutcliffe LLPthedundiesNoch keine Bewertungen

- Assignment CH-1 & 2Dokument11 SeitenAssignment CH-1 & 2Aarush GuptaNoch keine Bewertungen

- ASE20093 Resource BookDokument8 SeitenASE20093 Resource BookAung Zaw Htwe0% (1)

- Fundamentals of Accounting-I WorksheetDokument7 SeitenFundamentals of Accounting-I WorksheetLee HailuNoch keine Bewertungen

- The Rise of The Deferred Tax Assets in JapanDokument57 SeitenThe Rise of The Deferred Tax Assets in Japanpaliacho77Noch keine Bewertungen

- Business PlanDokument35 SeitenBusiness Planjohn mwambu100% (1)