Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Warranty and Defect Liability Period For Service ContractDokument2 SeitenWarranty and Defect Liability Period For Service ContractSiju Alex Cherian100% (5)

- 1 Ncnda Imfpa D2 PrinDokument8 Seiten1 Ncnda Imfpa D2 Prinemt6382100% (2)

- LTD Digest 1Dokument4 SeitenLTD Digest 1Soap MacTavishNoch keine Bewertungen

- Constitutional Law I NotesDokument5 SeitenConstitutional Law I NotesShannin MaeNoch keine Bewertungen

- Non-Impairment Clause ReviewerDokument3 SeitenNon-Impairment Clause ReviewerShannin MaeNoch keine Bewertungen

- Labo Jr. vs. ComelecDokument14 SeitenLabo Jr. vs. ComelecShannin MaeNoch keine Bewertungen

- Donation Mortis Causa vs Inter Vivos: Key DifferencesDokument10 SeitenDonation Mortis Causa vs Inter Vivos: Key DifferencesKwesi DelgadoNoch keine Bewertungen

- Philippines Minimum Wage Rates by Sector and Region 2016Dokument7 SeitenPhilippines Minimum Wage Rates by Sector and Region 2016Shannin MaeNoch keine Bewertungen

- Criminal Law II Reviewer PDFDokument33 SeitenCriminal Law II Reviewer PDFShannin MaeNoch keine Bewertungen

- Nature and Creation of Attorney-Client RelationshipDokument6 SeitenNature and Creation of Attorney-Client RelationshipShannin MaeNoch keine Bewertungen

- Constitutional Law I NotesDokument5 SeitenConstitutional Law I NotesShannin MaeNoch keine Bewertungen

- Environmental LawDokument1 SeiteEnvironmental LawShannin MaeNoch keine Bewertungen

- Criminal Law II Reviewer .2Dokument1 SeiteCriminal Law II Reviewer .2Shannin MaeNoch keine Bewertungen

- Title 3 Corpo. Case DigestsDokument16 SeitenTitle 3 Corpo. Case DigestsShannin MaeNoch keine Bewertungen

- Sacraments Show God's Presence Through ActionsDokument1 SeiteSacraments Show God's Presence Through ActionsShannin MaeNoch keine Bewertungen

- Philippines Minimum Wage Rates by Sector and Region 2016Dokument7 SeitenPhilippines Minimum Wage Rates by Sector and Region 2016Shannin MaeNoch keine Bewertungen

- Criminal Law II Reviewer PDFDokument33 SeitenCriminal Law II Reviewer PDFShannin MaeNoch keine Bewertungen

- Title 3 Corpo. Case DigestsDokument16 SeitenTitle 3 Corpo. Case DigestsShannin MaeNoch keine Bewertungen

- Groupings For Code of Judicial Conduct Report Pale 3CDokument1 SeiteGroupings For Code of Judicial Conduct Report Pale 3CShannin MaeNoch keine Bewertungen

- Agenda For SK Federation: Top Activities (Highly Suggested)Dokument2 SeitenAgenda For SK Federation: Top Activities (Highly Suggested)Shannin MaeNoch keine Bewertungen

- Canons 17 To 22 Case DigestDokument2 SeitenCanons 17 To 22 Case DigestShannin MaeNoch keine Bewertungen

- Bathroom and Furniture LayoutDokument2 SeitenBathroom and Furniture LayoutShannin MaeNoch keine Bewertungen

- Budget Hearing Summary: Total Budget For The Youth and Sports Development Program Is P5, 283, 459.16Dokument5 SeitenBudget Hearing Summary: Total Budget For The Youth and Sports Development Program Is P5, 283, 459.16Shannin MaeNoch keine Bewertungen

- 1pale Case DigestsasgDokument20 Seiten1pale Case DigestsasgShannin MaeNoch keine Bewertungen

- RA 9729 Climate Change ActDokument14 SeitenRA 9729 Climate Change ActBabangNoch keine Bewertungen

- Case List Consti2Dokument10 SeitenCase List Consti2Darren SulitNoch keine Bewertungen

- Application For A Search Warrant (PNP)Dokument1 SeiteApplication For A Search Warrant (PNP)Shannin MaeNoch keine Bewertungen

- Paper Chase Reflection PaperDokument1 SeitePaper Chase Reflection PaperShannin MaeNoch keine Bewertungen

- Sample of Application For Search WarrantDokument3 SeitenSample of Application For Search WarrantEmiliana Kampilan40% (5)

- Criminal Law II Reviewer .2Dokument1 SeiteCriminal Law II Reviewer .2Shannin MaeNoch keine Bewertungen

- Executive-Digests (Constitutional Law 1)Dokument1 SeiteExecutive-Digests (Constitutional Law 1)Shannin MaeNoch keine Bewertungen

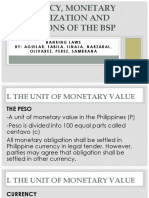

- CURRENCY, MONETARY STABILIZATION AND BANKING LAWSDokument88 SeitenCURRENCY, MONETARY STABILIZATION AND BANKING LAWSShannin MaeNoch keine Bewertungen

- Executive-Digests (Constitutional Law 1)Dokument28 SeitenExecutive-Digests (Constitutional Law 1)Shannin MaeNoch keine Bewertungen

- Continue..: - Appointment of InvigilatorsDokument6 SeitenContinue..: - Appointment of InvigilatorsPawan KumarNoch keine Bewertungen

- Mutual, 2-Way NDADokument7 SeitenMutual, 2-Way NDAponticarlo7658Noch keine Bewertungen

- W 02 (NCC) (W) 561 04 2015Dokument18 SeitenW 02 (NCC) (W) 561 04 2015zamribakar1967_52536Noch keine Bewertungen

- Abrogar v. Cosmos Bottling CoDokument6 SeitenAbrogar v. Cosmos Bottling CoMarian Gae MerinoNoch keine Bewertungen

- History of Egypt, Chaldæa, Syria, Babylonia, and Assyria, Volume 6 (Of 12) by Maspero, Gaston Camille Charles, 1846-1916Dokument12 SeitenHistory of Egypt, Chaldæa, Syria, Babylonia, and Assyria, Volume 6 (Of 12) by Maspero, Gaston Camille Charles, 1846-1916Gutenberg.orgNoch keine Bewertungen

- Solid Homes V Tan G R No 145156Dokument3 SeitenSolid Homes V Tan G R No 145156Anonymous 91f03cwNoch keine Bewertungen

- RA 8424 and RA 10963 tax provisions comparedDokument14 SeitenRA 8424 and RA 10963 tax provisions comparedFatima BrionesNoch keine Bewertungen

- Executive Order No. 292 (BOOK V - Title I - Subtitle A - Chapter 7-Discipline) - Official Gazette of The Republic of The PhilippinesDokument7 SeitenExecutive Order No. 292 (BOOK V - Title I - Subtitle A - Chapter 7-Discipline) - Official Gazette of The Republic of The PhilippinesJasonV.PanayNoch keine Bewertungen

- Georgina Paintball WAIVER FORMDokument1 SeiteGeorgina Paintball WAIVER FORMAndrew HalsteadNoch keine Bewertungen

- IRS Notice Form for Fiduciary RelationshipDokument2 SeitenIRS Notice Form for Fiduciary Relationshipphard2345100% (1)

- Agcaoili Vs GSISDokument5 SeitenAgcaoili Vs GSISGloria Diana DulnuanNoch keine Bewertungen

- Last Will Testament SummaryDokument4 SeitenLast Will Testament SummaryNombs NomNoch keine Bewertungen

- Stages of a Civil SuitDokument3 SeitenStages of a Civil SuitAnkit Sharma50% (2)

- Certainty of Objects and The Beneficiary PrincipleDokument27 SeitenCertainty of Objects and The Beneficiary Principlearian100% (1)

- Union Manufacturing Co Vs Philippine Guaranty CoDokument3 SeitenUnion Manufacturing Co Vs Philippine Guaranty CoChelle BelenzoNoch keine Bewertungen

- G.R. No. 149295 - Philippine National Bank v. de JesusDokument7 SeitenG.R. No. 149295 - Philippine National Bank v. de JesusJaana AlbanoNoch keine Bewertungen

- Mary Ann Vernatter v. Allstate Insurance Company, An Illinois Corporation, 362 F.2d 403, 4th Cir. (1966)Dokument6 SeitenMary Ann Vernatter v. Allstate Insurance Company, An Illinois Corporation, 362 F.2d 403, 4th Cir. (1966)Scribd Government DocsNoch keine Bewertungen

- w9 Request JeffCo District Court 3-22-2022Dokument2 Seitenw9 Request JeffCo District Court 3-22-2022otis tolbertNoch keine Bewertungen

- Landbank of The Philippines Vs Villegas Case DigestDokument2 SeitenLandbank of The Philippines Vs Villegas Case DigestManuelMarasiganMismanosNoch keine Bewertungen

- Supreme Court: Primicias, Abad, Mencies & Castillo For Petitioner. Moises Ma. Buhain For RespondentDokument7 SeitenSupreme Court: Primicias, Abad, Mencies & Castillo For Petitioner. Moises Ma. Buhain For RespondentPaulette AquinoNoch keine Bewertungen

- 1 Interpleader Cases 1 10Dokument11 Seiten1 Interpleader Cases 1 10Anonymous fnlSh4KHIgNoch keine Bewertungen

- REF - 2944126 Jul 23-Respond - Initial-28072023Dokument1 SeiteREF - 2944126 Jul 23-Respond - Initial-28072023Paul Snowdon JeffersonNoch keine Bewertungen

- AFFIDAVIT OF NEIGHBOR's CONSENTDokument1 SeiteAFFIDAVIT OF NEIGHBOR's CONSENTWell LaboratoryNoch keine Bewertungen

- G.R. No. 218901Dokument5 SeitenG.R. No. 218901FbarrsNoch keine Bewertungen

- Supreme Court hears challenge to ED attachment in IBC caseDokument2 SeitenSupreme Court hears challenge to ED attachment in IBC caseAbhinandan SharmaNoch keine Bewertungen

- Cambria Company v. Cosmos Granite & Marble, NC - ComplaintDokument17 SeitenCambria Company v. Cosmos Granite & Marble, NC - ComplaintSarah BursteinNoch keine Bewertungen

- MERCHANT SHIPPING ORDINANCE 1952 MalaysiaDokument4 SeitenMERCHANT SHIPPING ORDINANCE 1952 MalaysiaOrite100% (1)