Das könnte Ihnen auch gefallen

- COVENANTS WorksheetDokument3 SeitenCOVENANTS Worksheetsubhojit dasNoch keine Bewertungen

- Muster Roll - (They Were Employees Who Were Engaged by The MunicipalDokument3 SeitenMuster Roll - (They Were Employees Who Were Engaged by The Municipalsubhojit dasNoch keine Bewertungen

- TBT and SPSDokument2 SeitenTBT and SPSsubhojit dasNoch keine Bewertungen

- Car Purchase Agreement TemplateDokument2 SeitenCar Purchase Agreement Templatesubhojit dasNoch keine Bewertungen

- Car Purchase Agreement TemplateDokument2 SeitenCar Purchase Agreement Templatesubhojit dasNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Account StatementDokument6 SeitenAccount Statementunkosii siyeeNoch keine Bewertungen

- Account Summary Payment Information: New Balance: $261.55Dokument6 SeitenAccount Summary Payment Information: New Balance: $261.55AriadnaUrsachi100% (2)

- Statement 1700313960560Dokument28 SeitenStatement 1700313960560Arun MuniNoch keine Bewertungen

- User Id 012439461813 - DSL Telephonenumber 01244823150Dokument6 SeitenUser Id 012439461813 - DSL Telephonenumber 01244823150NAVEEN SLNoch keine Bewertungen

- Sales Quotation: Jl. Nias 3 No. 33 Lingk. Tegalboto Kidul, Kel. Sumbersari, Kec. Sumbersari Kab. Jember, Jawa TimurDokument1 SeiteSales Quotation: Jl. Nias 3 No. 33 Lingk. Tegalboto Kidul, Kel. Sumbersari, Kec. Sumbersari Kab. Jember, Jawa TimurAde HerdiansyahNoch keine Bewertungen

- Tax Reforms in Pakistan Historic and Critical ViewDokument299 SeitenTax Reforms in Pakistan Historic and Critical ViewJąhąnząib Khąn KąkąrNoch keine Bewertungen

- Neft and RtgsDokument4 SeitenNeft and RtgsmukeshkpatidarNoch keine Bewertungen

- Prelim TaxDokument5 SeitenPrelim TaxDonna Zandueta-TumalaNoch keine Bewertungen

- Invoice - 1Dokument1 SeiteInvoice - 1Toney KurianNoch keine Bewertungen

- 2166 COC BookletDokument34 Seiten2166 COC BookletSamay MaraviNoch keine Bewertungen

- Interim Statement 10-Mar-2023 12-25-49Dokument2 SeitenInterim Statement 10-Mar-2023 12-25-49zani arslanNoch keine Bewertungen

- NDokument2 SeitenNYna YnaNoch keine Bewertungen

- Form16 W0000000 GS186523X 2021 20211Dokument1 SeiteForm16 W0000000 GS186523X 2021 20211Raman OjhaNoch keine Bewertungen

- Your Child's Account by The End of The School YearDokument3 SeitenYour Child's Account by The End of The School YeariNeko FriesNoch keine Bewertungen

- Income and Business TaxationDokument1 SeiteIncome and Business TaxationTomo Euryl San JuanNoch keine Bewertungen

- May 30 Provider Relief Fund FAQ RedlineDokument23 SeitenMay 30 Provider Relief Fund FAQ RedlineRachel Cohrs100% (1)

- BIR Ruling No. 051 2000 PDFDokument3 SeitenBIR Ruling No. 051 2000 PDFVina CeeNoch keine Bewertungen

- AttachmentDokument31 SeitenAttachmentHambaNoch keine Bewertungen

- CH - 10 Tax Invoice, Credit and Debit Notes Que by ICAIDokument3 SeitenCH - 10 Tax Invoice, Credit and Debit Notes Que by ICAIk kakkarNoch keine Bewertungen

- Tax Card TY 2022Dokument8 SeitenTax Card TY 2022princecharming14Noch keine Bewertungen

- Tax Invoice: Smartschool Education PVT LTDDokument1 SeiteTax Invoice: Smartschool Education PVT LTDHarshit SuriNoch keine Bewertungen

- Final ReitDokument5 SeitenFinal Reitchris_yvonneNoch keine Bewertungen

- Swiggy Order 58514422563Dokument2 SeitenSwiggy Order 58514422563SakshamNoch keine Bewertungen

- Fiscal Policy of Pakistan: Presented By: RDokument30 SeitenFiscal Policy of Pakistan: Presented By: Rfujimukazu93% (42)

- MasterCard Prepaid TandCDokument9 SeitenMasterCard Prepaid TandCmikeNoch keine Bewertungen

- Vamsi Krishna Velaga - ITDokument1 SeiteVamsi Krishna Velaga - ITvamsiNoch keine Bewertungen

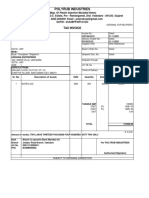

- Polyrub Industries Invoice 56Dokument1 SeitePolyrub Industries Invoice 56jemish limbaniNoch keine Bewertungen

- Copy DETENTION INVOICE Number: 5260418140: Total Amount Due Condition Rate Base Value Total (USD)Dokument2 SeitenCopy DETENTION INVOICE Number: 5260418140: Total Amount Due Condition Rate Base Value Total (USD)dinesh pillaiNoch keine Bewertungen

- Questions On Imprest SysyemDokument3 SeitenQuestions On Imprest Sysyemyuvita prasadNoch keine Bewertungen

- Income Tax Refund ChartDokument2 SeitenIncome Tax Refund ChartKelly Phillips ErbNoch keine Bewertungen