Das könnte Ihnen auch gefallen

- Module in Introduction To The World ReligionDokument70 SeitenModule in Introduction To The World ReligionAlex Antenero93% (44)

- PORTER'S FIVE FORCES ANALYSIS ON TELECOM INDUSTRYDokument11 SeitenPORTER'S FIVE FORCES ANALYSIS ON TELECOM INDUSTRYradhukanuNoch keine Bewertungen

- Discounted Cash Flow (DCF) Definition - InvestopediaDokument2 SeitenDiscounted Cash Flow (DCF) Definition - Investopedianaviprasadthebond9532Noch keine Bewertungen

- USOnline PayslipDokument2 SeitenUSOnline PayslipTami SariNoch keine Bewertungen

- School Form 10 SF10 Learners Permanent Academic Record For Elementary SchoolDokument10 SeitenSchool Form 10 SF10 Learners Permanent Academic Record For Elementary SchoolRene ManansalaNoch keine Bewertungen

- Al Fara'aDokument56 SeitenAl Fara'azoinasNoch keine Bewertungen

- PORTER 5 ForcesDokument4 SeitenPORTER 5 ForcesMiley MartinNoch keine Bewertungen

- Porter Five Forces WordDokument11 SeitenPorter Five Forces WordvinodvahoraNoch keine Bewertungen

- The Telecom Industry HandbookDokument3 SeitenThe Telecom Industry HandbookAman DeepNoch keine Bewertungen

- Porter's Five Forces On Us Telecom IndustryDokument5 SeitenPorter's Five Forces On Us Telecom IndustrySagar MallikNoch keine Bewertungen

- The Industry HandbookDokument13 SeitenThe Industry HandbookRenu NerlekarNoch keine Bewertungen

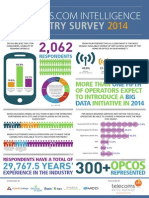

- Industry Survey: More Than of Operators Expect To Introduce A Initiative inDokument40 SeitenIndustry Survey: More Than of Operators Expect To Introduce A Initiative intanveerameenNoch keine Bewertungen

- The Industry HandbookDokument7 SeitenThe Industry HandbookknnoknnoNoch keine Bewertungen

- Trends, Opportunities and Use Cases For Mobile Data Monetization in Mature MarketsDokument12 SeitenTrends, Opportunities and Use Cases For Mobile Data Monetization in Mature MarketspragsyNoch keine Bewertungen

- Advantages and Disadvantages of The Voice Over Internet Protocol BusinessDokument3 SeitenAdvantages and Disadvantages of The Voice Over Internet Protocol BusinessNithin JoyNoch keine Bewertungen

- Telecom Industry Value Chain Turning On Its HeadDokument2 SeitenTelecom Industry Value Chain Turning On Its HeadPeter OkohNoch keine Bewertungen

- Mobil Europe 1.8Dokument53 SeitenMobil Europe 1.8Sajeel RehmanNoch keine Bewertungen

- Porter'S Five Forces Analysis of Indian Telecom Industry: I. Buyer PowerDokument6 SeitenPorter'S Five Forces Analysis of Indian Telecom Industry: I. Buyer PowerRahul SinghNoch keine Bewertungen

- Five Force Analysis of Japan's Telecom Industry at i-mode LaunchDokument4 SeitenFive Force Analysis of Japan's Telecom Industry at i-mode Launchnitishhere100% (2)

- Business Strategy Assignment - Final TelecomDokument10 SeitenBusiness Strategy Assignment - Final TelecomAishwarya SankhlaNoch keine Bewertungen

- Telecommunications Final PaperDokument41 SeitenTelecommunications Final PaperJessieHaNoch keine Bewertungen

- Analysys Mason - TRANSFORMING NETWORK INTELLIGENCE INTO A POSITIVE CUSTOMER EXPERIENCE AND REVENUE-GENERATING OPPORTUNITIESDokument16 SeitenAnalysys Mason - TRANSFORMING NETWORK INTELLIGENCE INTO A POSITIVE CUSTOMER EXPERIENCE AND REVENUE-GENERATING OPPORTUNITIESCommProveNoch keine Bewertungen

- Handset Leasing - Unlock Opportunities To Regain Financial Position in Telecom IndustryDokument7 SeitenHandset Leasing - Unlock Opportunities To Regain Financial Position in Telecom IndustryHoàng NguyễnNoch keine Bewertungen

- VoIP in Developing Countries - The Next Disruptive TechnologyDokument16 SeitenVoIP in Developing Countries - The Next Disruptive TechnologyHavanyaniNoch keine Bewertungen

- IRG 63 Business SvcsDokument2 SeitenIRG 63 Business SvcsiwanrNoch keine Bewertungen

- Pre-Paid Customer Churn Prediction Using SPSSDokument18 SeitenPre-Paid Customer Churn Prediction Using SPSSabhi1098Noch keine Bewertungen

- Policy Identity Sec WPDokument18 SeitenPolicy Identity Sec WPabohemadeNoch keine Bewertungen

- Telecom Sector Porter's 5 Force AnalysisDokument3 SeitenTelecom Sector Porter's 5 Force AnalysisKARTIK ANAND100% (1)

- IST 755 Telecom Industry AnalysisDokument29 SeitenIST 755 Telecom Industry AnalysisAditya GuptaNoch keine Bewertungen

- How To Choose Voip 91213Dokument8 SeitenHow To Choose Voip 91213johodadaNoch keine Bewertungen

- By Rafael Junquera,: Smartphones: Are They The Real Deal?Dokument5 SeitenBy Rafael Junquera,: Smartphones: Are They The Real Deal?kallolshyam.roy2811Noch keine Bewertungen

- STRATEGIC MANAGEMENT-assignemtDokument4 SeitenSTRATEGIC MANAGEMENT-assignemtUmaimatu Paredavoa FuseiniNoch keine Bewertungen

- The Evolution of Voip: A Look Into How Voip Has Proliferated Into The Global Dominant Platform It Is TodayDokument48 SeitenThe Evolution of Voip: A Look Into How Voip Has Proliferated Into The Global Dominant Platform It Is TodayBradley SusserNoch keine Bewertungen

- IMS Next Gen Comm Networks 080905Dokument16 SeitenIMS Next Gen Comm Networks 080905api-3807600Noch keine Bewertungen

- Risk Management Notes (Revised)Dokument13 SeitenRisk Management Notes (Revised)Imtiaz KaziNoch keine Bewertungen

- Five inspiring telecom business model innovationsDokument32 SeitenFive inspiring telecom business model innovationsAveek DaschoudhuryNoch keine Bewertungen

- The Industry Handbook - The Telecommunications Industry: Back To Industry ListDokument5 SeitenThe Industry Handbook - The Telecommunications Industry: Back To Industry ListAnkush ThoratNoch keine Bewertungen

- Presentation On Airtel and Cell Phone Service IndustryDokument37 SeitenPresentation On Airtel and Cell Phone Service Industrygagan15095895Noch keine Bewertungen

- Magova TCRADokument5 SeitenMagova TCRADenis Ruvilo0% (1)

- 612858Dokument42 Seiten612858Araceli MartínezNoch keine Bewertungen

- Telecom Industry Value Chain - enDokument2 SeitenTelecom Industry Value Chain - ennarayan_umallaNoch keine Bewertungen

- Top 3 Ownership Models for Neutral Host DASDokument7 SeitenTop 3 Ownership Models for Neutral Host DASfarrukhmohammedNoch keine Bewertungen

- 4D Tip ReportDokument16 Seiten4D Tip ReportGeorge GuNoch keine Bewertungen

- SBL BPP Kit-2019 Copy 449Dokument1 SeiteSBL BPP Kit-2019 Copy 449Reever RiverNoch keine Bewertungen

- Selecting Voip For Your Enterprise: Expert Reference Series of White PapersDokument13 SeitenSelecting Voip For Your Enterprise: Expert Reference Series of White PapersToàn ĐẶng KhắcNoch keine Bewertungen

- Assignment: Case Studies For Telecom Business FinanceDokument11 SeitenAssignment: Case Studies For Telecom Business FinancesinghrachanabaghelNoch keine Bewertungen

- IMS-IP Multimedia Subsystem: IMS Overview and The Unified Carrier NetworkDokument11 SeitenIMS-IP Multimedia Subsystem: IMS Overview and The Unified Carrier NetworkManas RanjanNoch keine Bewertungen

- Your Money's Worth The Business Value of VoIP RecordingDokument6 SeitenYour Money's Worth The Business Value of VoIP Recordingamhosny64Noch keine Bewertungen

- Innovativepricing PDFDokument6 SeitenInnovativepricing PDFQristin ViolindaNoch keine Bewertungen

- Volte Strategy From MavenirDokument20 SeitenVolte Strategy From MavenirRajib BashirNoch keine Bewertungen

- Toyota's Strategic Analysis and Customer Value Development in the UKDokument7 SeitenToyota's Strategic Analysis and Customer Value Development in the UKAliNoch keine Bewertungen

- Internet Service Provider Business PlanDokument20 SeitenInternet Service Provider Business Planmanzaranis22Noch keine Bewertungen

- Empirical Evaluation of Fair Use Flat Rate Strategies For Mobile InternetDokument22 SeitenEmpirical Evaluation of Fair Use Flat Rate Strategies For Mobile InternetalifatehitqmNoch keine Bewertungen

- ZZZDokument47 SeitenZZZaaron827077Noch keine Bewertungen

- In 1034Dokument3 SeitenIn 1034SteveGreavesNoch keine Bewertungen

- SaaS Manager Case StudyDokument11 SeitenSaaS Manager Case StudyMuhammad HaseebNoch keine Bewertungen

- McKinsey Telecoms. RECALL No. 17, 2011 - Transition To Digital in High-Growth MarketsDokument76 SeitenMcKinsey Telecoms. RECALL No. 17, 2011 - Transition To Digital in High-Growth MarketskentselveNoch keine Bewertungen

- Literature Review On Voip SecurityDokument8 SeitenLiterature Review On Voip Securitytug0l0byh1g2100% (2)

- Openet Subscriber Optimized Charging 4G Services WPDokument19 SeitenOpenet Subscriber Optimized Charging 4G Services WPaimoneyNoch keine Bewertungen

- Technical, Commercial and Regulatory Challenges of QoS: An Internet Service Model PerspectiveVon EverandTechnical, Commercial and Regulatory Challenges of QoS: An Internet Service Model PerspectiveNoch keine Bewertungen

- Summary of Heather Brilliant & Elizabeth Collins's Why Moats MatterVon EverandSummary of Heather Brilliant & Elizabeth Collins's Why Moats MatterNoch keine Bewertungen

- VoIP Telephony and You: A Guide to Design and Build a Resilient Infrastructure for Enterprise Communications Using the VoIP Technology (English Edition)Von EverandVoIP Telephony and You: A Guide to Design and Build a Resilient Infrastructure for Enterprise Communications Using the VoIP Technology (English Edition)Noch keine Bewertungen

- BBD Electronics Day3 Online at Best Price - Flipkart - pdf2Dokument4 SeitenBBD Electronics Day3 Online at Best Price - Flipkart - pdf2naviprasadthebond9532Noch keine Bewertungen

- The Bivariate Normal DistributionDokument11 SeitenThe Bivariate Normal DistributionaharisjoNoch keine Bewertungen

- A Bright Future For Indias Defense IndustryDokument12 SeitenA Bright Future For Indias Defense IndustryKiran ChokshiNoch keine Bewertungen

- 26 Car One Liners - Funniest Car Jokes - OneLineFun1Dokument2 Seiten26 Car One Liners - Funniest Car Jokes - OneLineFun1naviprasadthebond9532Noch keine Bewertungen

- Aristotle's View of Courage as a Disposition Formed Through PracticeDokument2 SeitenAristotle's View of Courage as a Disposition Formed Through Practicenaviprasadthebond9532Noch keine Bewertungen

- 26 Car One Liners - Funniest Car Jokes - 2 - OneLineFun2Dokument2 Seiten26 Car One Liners - Funniest Car Jokes - 2 - OneLineFun2naviprasadthebond9532Noch keine Bewertungen

- Five Things We Learned On Day Three of Roland Garros 2016 - Sports - RFIDokument2 SeitenFive Things We Learned On Day Three of Roland Garros 2016 - Sports - RFInaviprasadthebond9532Noch keine Bewertungen

- 33 Beautiful Indian Baby Names You Wish Your Parents Had Chosen For You PDFDokument20 Seiten33 Beautiful Indian Baby Names You Wish Your Parents Had Chosen For You PDFnaviprasadthebond9532Noch keine Bewertungen

- Kathasaritsagara (English) by Charles H. TawneyDokument364 SeitenKathasaritsagara (English) by Charles H. Tawneynaviprasadthebond9532100% (1)

- The Black-Scholes ModelDokument42 SeitenThe Black-Scholes Modelnaviprasadthebond9532Noch keine Bewertungen

- Panchtantra, Moti Chand, Kahani SangrahDokument306 SeitenPanchtantra, Moti Chand, Kahani Sangrahnaviprasadthebond9532Noch keine Bewertungen

- NASSCOM Strategic Review 2015 Executive SummaryDokument14 SeitenNASSCOM Strategic Review 2015 Executive SummaryRatnadeep JoshiNoch keine Bewertungen

- Panch TantraDokument313 SeitenPanch Tantranaviprasadthebond9532Noch keine Bewertungen

- Interview with John G. Thompson and Jacques Tits on Early Mathematical ExperiencesDokument8 SeitenInterview with John G. Thompson and Jacques Tits on Early Mathematical Experiencesnaviprasadthebond9532Noch keine Bewertungen

- 33 Beautiful Indian Baby Names You Wish Your Parents Had Chosen For You PDFDokument20 Seiten33 Beautiful Indian Baby Names You Wish Your Parents Had Chosen For You PDFnaviprasadthebond9532Noch keine Bewertungen

- Documents StackDokument1 SeiteDocuments StackDan MNoch keine Bewertungen

- GRE 1500 WordDokument75 SeitenGRE 1500 WordAkshay GuptaNoch keine Bewertungen

- Medford Airport History (TX)Dokument33 SeitenMedford Airport History (TX)CAP History LibraryNoch keine Bewertungen

- Unique and Interactive EffectsDokument14 SeitenUnique and Interactive EffectsbinepaNoch keine Bewertungen

- RPPSN Arbour StatementDokument2 SeitenRPPSN Arbour StatementJohnPhilpotNoch keine Bewertungen

- SECTION 26. Registration of Threatened and Exotic Wildlife in The Possession of Private Persons. - NoDokument5 SeitenSECTION 26. Registration of Threatened and Exotic Wildlife in The Possession of Private Persons. - NoAron PanturillaNoch keine Bewertungen

- CallClerk User GuideDokument94 SeitenCallClerk User GuiderrjlNoch keine Bewertungen

- Time Value of Money - TheoryDokument7 SeitenTime Value of Money - TheoryNahidul Islam IUNoch keine Bewertungen

- Entrance English Test for Graduate Management StudiesDokument6 SeitenEntrance English Test for Graduate Management StudiesPhương Linh TrươngNoch keine Bewertungen

- Cruise LetterDokument23 SeitenCruise LetterSimon AlvarezNoch keine Bewertungen

- Reading Comprehension and Vocabulary PracticeDokument10 SeitenReading Comprehension and Vocabulary Practice徐明羽Noch keine Bewertungen

- A Research Agenda For Creative Tourism: OnlineDokument1 SeiteA Research Agenda For Creative Tourism: OnlineFelipe Luis GarciaNoch keine Bewertungen

- Coiculescu PDFDokument2 SeitenCoiculescu PDFprateek_301466650Noch keine Bewertungen

- Legal Notice: Submitted By: Amit Grover Bba L.LB (H) Section B A3221515130Dokument9 SeitenLegal Notice: Submitted By: Amit Grover Bba L.LB (H) Section B A3221515130Amit GroverNoch keine Bewertungen

- Vista Print TaxInvoiceDokument2 SeitenVista Print TaxInvoicebhageshlNoch keine Bewertungen

- URP - Questionnaire SampleDokument8 SeitenURP - Questionnaire SampleFardinNoch keine Bewertungen

- 1 292583745 Bill For Current Month 1Dokument2 Seiten1 292583745 Bill For Current Month 1Shrotriya AnamikaNoch keine Bewertungen

- CV Experienced Marketing ProfessionalDokument2 SeitenCV Experienced Marketing ProfessionalPankaj JaiswalNoch keine Bewertungen

- Sunway Berhad (F) Part 2 (Page 97-189)Dokument93 SeitenSunway Berhad (F) Part 2 (Page 97-189)qeylazatiey93_598514100% (1)

- The Meaning of Life Without Parole - Rough Draft 1Dokument4 SeitenThe Meaning of Life Without Parole - Rough Draft 1api-504422093Noch keine Bewertungen

- Baccmass - ChordsDokument7 SeitenBaccmass - ChordsYuan MasudaNoch keine Bewertungen

- CIR vs. CA YMCA G.R. No. 124043 October 14 1998Dokument1 SeiteCIR vs. CA YMCA G.R. No. 124043 October 14 1998Anonymous MikI28PkJc100% (1)

- How To Get The Poor Off Our ConscienceDokument4 SeitenHow To Get The Poor Off Our Conscience钟丽虹Noch keine Bewertungen

- Engineering Economy 2ed Edition: January 2018Dokument12 SeitenEngineering Economy 2ed Edition: January 2018anup chauhanNoch keine Bewertungen

- Investment Decision RulesDokument113 SeitenInvestment Decision RulesHuy PanhaNoch keine Bewertungen

- Human Resource Management in HealthDokument7 SeitenHuman Resource Management in HealthMark MadridanoNoch keine Bewertungen

- RVU Distribution - New ChangesDokument5 SeitenRVU Distribution - New Changesmy indiaNoch keine Bewertungen

- 20% DEVELOPMENT UTILIZATION FOR FY 2021Dokument2 Seiten20% DEVELOPMENT UTILIZATION FOR FY 2021edvince mickael bagunas sinonNoch keine Bewertungen