Das könnte Ihnen auch gefallen

- Chapter 1: Cash and Cash Equivalents Expected Question(s) :: Cash On Hand Cash Fund Cash in BankDokument8 SeitenChapter 1: Cash and Cash Equivalents Expected Question(s) :: Cash On Hand Cash Fund Cash in BankJulie Mae Caling MalitNoch keine Bewertungen

- FARP Quick NotesDokument5 SeitenFARP Quick NotesNicky ChrisNoch keine Bewertungen

- ACCTGBKSDokument4 SeitenACCTGBKSRejed VillanuevaNoch keine Bewertungen

- Unit 5. Audit of Investments, Hedging Instruments, and Related Revenues - Handout - T21920 (Final)Dokument9 SeitenUnit 5. Audit of Investments, Hedging Instruments, and Related Revenues - Handout - T21920 (Final)Alyna JNoch keine Bewertungen

- Intermediate Accounting, Part 1Dokument7 SeitenIntermediate Accounting, Part 1dfsdfdsfNoch keine Bewertungen

- WMDokument31 SeitenWMNiña Rhocel YangcoNoch keine Bewertungen

- Financial Asset MILLANDokument6 SeitenFinancial Asset MILLANAlelie Joy dela CruzNoch keine Bewertungen

- ACCTBA1 - Exercises On Adjusting EntriesDokument5 SeitenACCTBA1 - Exercises On Adjusting EntriesRichard Leighton100% (1)

- Int. Acctg. 3 - Valix2019 - Chapter 3Dokument12 SeitenInt. Acctg. 3 - Valix2019 - Chapter 3Toni Rose Hernandez Lualhati100% (1)

- Mas 09 - Working CapitalDokument7 SeitenMas 09 - Working CapitalCarl Angelo LopezNoch keine Bewertungen

- #16 Investment PropertyDokument4 Seiten#16 Investment PropertyClaudine DuhapaNoch keine Bewertungen

- Lecture Notes Advanced AccountingDokument18 SeitenLecture Notes Advanced AccountingGilbert Tiong100% (1)

- FinACt 5 Foreign Currency TransactionsDokument2 SeitenFinACt 5 Foreign Currency TransactionsBedynz Mark Pimentel100% (2)

- Albert I. Rivera, CPA, MBA, CRA 1Dokument6 SeitenAlbert I. Rivera, CPA, MBA, CRA 1Reina EvangelistaNoch keine Bewertungen

- Lecture Notes On Inventory Estimation - 000Dokument4 SeitenLecture Notes On Inventory Estimation - 000judel ArielNoch keine Bewertungen

- Auditing ProblemsDokument2 SeitenAuditing ProblemsYenelyn Apistar CambarijanNoch keine Bewertungen

- PRTC Manufacturing Co.Dokument2 SeitenPRTC Manufacturing Co.hersheyNoch keine Bewertungen

- I. 1. Acquisition Method: Non-Controlling Interest Consolidated StatementDokument14 SeitenI. 1. Acquisition Method: Non-Controlling Interest Consolidated StatementCookies And CreamNoch keine Bewertungen

- Chapter 5 Accounting For Disbursements and Related TransactionsDokument2 SeitenChapter 5 Accounting For Disbursements and Related TransactionsJaps100% (1)

- Ais MidtermDokument5 SeitenAis MidtermMosabAbuKhaterNoch keine Bewertungen

- Accounts Receivable (Chapter 4)Dokument31 SeitenAccounts Receivable (Chapter 4)chingNoch keine Bewertungen

- Acco 30053 - Audit of Cash and Cash EquivalentsDokument19 SeitenAcco 30053 - Audit of Cash and Cash EquivalentsmarkNoch keine Bewertungen

- Answer Key For Cpa Board Exam ReviewerDokument4 SeitenAnswer Key For Cpa Board Exam ReviewerMaria LopezNoch keine Bewertungen

- Auditing Theory - Risk AssessmentDokument10 SeitenAuditing Theory - Risk AssessmentYenelyn Apistar CambarijanNoch keine Bewertungen

- 1.0 Notes Cash and Cash Equivalents 1.0 Notes Cash and Cash EquivalentsDokument181 Seiten1.0 Notes Cash and Cash Equivalents 1.0 Notes Cash and Cash EquivalentsLawrence YusiNoch keine Bewertungen

- Practical Accounting by Valix Practical Accounting by ValixDokument24 SeitenPractical Accounting by Valix Practical Accounting by ValixMartha Nicole MaristelaNoch keine Bewertungen

- Audit of ReceivablesDokument48 SeitenAudit of Receivablescarl fuerzasNoch keine Bewertungen

- Module 2 Cash, Accrual and Single EntryDokument10 SeitenModule 2 Cash, Accrual and Single EntryFernando III PerezNoch keine Bewertungen

- 01 - Audit of Cash & Cash EquivalentsDokument4 Seiten01 - Audit of Cash & Cash EquivalentsEARL JOHN RosalesNoch keine Bewertungen

- Afar Quicknotes: GATO, Abdul Barri Indol MSU - Main Campus 09452146094Dokument19 SeitenAfar Quicknotes: GATO, Abdul Barri Indol MSU - Main Campus 09452146094Zech PackNoch keine Bewertungen

- Standard Costing and Variances (OK Na!)Dokument6 SeitenStandard Costing and Variances (OK Na!)Jane Michelle EmanNoch keine Bewertungen

- Far 102 - Cash and Cash EquivalentsDokument4 SeitenFar 102 - Cash and Cash EquivalentsKeanna Denise GonzalesNoch keine Bewertungen

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Dokument15 SeitenReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNoch keine Bewertungen

- Cash & Cash Equivalents, Lecture &exercisesDokument16 SeitenCash & Cash Equivalents, Lecture &exercisesDessa GarongNoch keine Bewertungen

- Module I. Business Combination Date of Acquisition NADokument13 SeitenModule I. Business Combination Date of Acquisition NAmax pNoch keine Bewertungen

- List of Pfrs 2018Dokument5 SeitenList of Pfrs 2018Myda Rafael100% (1)

- PUP Review Handout 1 OfficialDokument3 SeitenPUP Review Handout 1 OfficialDonalyn CalipusNoch keine Bewertungen

- This Study Resource Was: Current Asset - Cash & Cash Equivalents CompositionsDokument2 SeitenThis Study Resource Was: Current Asset - Cash & Cash Equivalents CompositionsKim TanNoch keine Bewertungen

- Financialaccounting 3 Theories Summary ValixDokument10 SeitenFinancialaccounting 3 Theories Summary ValixDarwin Competente LagranNoch keine Bewertungen

- Pfrs Update 2022Dokument21 SeitenPfrs Update 2022Robert CastilloNoch keine Bewertungen

- Template - Assignment - Audit of ReceivablesDokument6 SeitenTemplate - Assignment - Audit of ReceivablesEdemson NavalesNoch keine Bewertungen

- Sale Price of Replaced Equipment P 40,000Dokument15 SeitenSale Price of Replaced Equipment P 40,000Jay GamboaNoch keine Bewertungen

- Chapter 31 - Substantive Test of Income Statement AccountsDokument8 SeitenChapter 31 - Substantive Test of Income Statement AccountsDeeNoch keine Bewertungen

- Solution Manual - Chapter 1Dokument5 SeitenSolution Manual - Chapter 1psrikanthmbaNoch keine Bewertungen

- Theory of Accounts - Valix - CinEquityDokument10 SeitenTheory of Accounts - Valix - CinEquityMaryrose Gestoso0% (1)

- Business LawDokument45 SeitenBusiness LawCherwin bentulan100% (2)

- Reo Notes - Audit ProbDokument13 SeitenReo Notes - Audit ProbgeexellNoch keine Bewertungen

- MSC-Audited FS With Notes - 2014 - CaseDokument12 SeitenMSC-Audited FS With Notes - 2014 - CaseMikaela SalvadorNoch keine Bewertungen

- Audit of Cash and Cash EquivalentsDokument108 SeitenAudit of Cash and Cash Equivalentscarl fuerzasNoch keine Bewertungen

- Cash and Cash EquivalentsDokument3 SeitenCash and Cash EquivalentsnikkitaaaNoch keine Bewertungen

- Conceptual Framework and Accounting StandardsDokument4 SeitenConceptual Framework and Accounting StandardsKrestyl Ann GabaldaNoch keine Bewertungen

- Aud Prob Part 1Dokument106 SeitenAud Prob Part 1Ma. Hazel Donita DiazNoch keine Bewertungen

- Cpale Subjects & TopicsDokument12 SeitenCpale Subjects & Topicsnikol sanchezNoch keine Bewertungen

- Cash and Cash EquivalentsDokument33 SeitenCash and Cash EquivalentsJohn kyle Abbago100% (2)

- Bank Reconciliation Theory & ProblemsDokument9 SeitenBank Reconciliation Theory & ProblemsSalvador DapatNoch keine Bewertungen

- Written Report CashDokument16 SeitenWritten Report CashFatima BalagaNoch keine Bewertungen

- Unit 1 - CASH AND CASH EQUIVALENTS PDFDokument9 SeitenUnit 1 - CASH AND CASH EQUIVALENTS PDFJeric Lagyaban Astrologio100% (1)

- Bank ReconciliationDokument20 SeitenBank ReconciliationLoslyn LumacangNoch keine Bewertungen

- Intermediate Accounting 1 by Sir ChuaDokument22 SeitenIntermediate Accounting 1 by Sir ChuaAnalyn LafradezNoch keine Bewertungen

- Intermediate Accounting I - Notes (9.13.2022)Dokument18 SeitenIntermediate Accounting I - Notes (9.13.2022)Mainit, Shiela Mae, S.Noch keine Bewertungen

- Cornerstones: of Managerial Accounting, 5eDokument30 SeitenCornerstones: of Managerial Accounting, 5eLeneNoch keine Bewertungen

- Lecture Note - Receivables Sy 2014-2015Dokument10 SeitenLecture Note - Receivables Sy 2014-2015LeneNoch keine Bewertungen

- Partnership Midterm Set BDokument10 SeitenPartnership Midterm Set BLene100% (1)

- Inventories - Additional Valuation IssuesDokument56 SeitenInventories - Additional Valuation IssuesLeneNoch keine Bewertungen

- Articles of PartnershipDokument3 SeitenArticles of PartnershipLeneNoch keine Bewertungen

- Club Medica Practice Set - 1Dokument43 SeitenClub Medica Practice Set - 1Lene91% (11)

- Philippine Financial System MaterialDokument24 SeitenPhilippine Financial System MaterialLeneNoch keine Bewertungen

- Song LyricsDokument55 SeitenSong LyricsLeneNoch keine Bewertungen

- Competito Analysis of Anand RathiDokument62 SeitenCompetito Analysis of Anand RathiSaran Kutty67% (3)

- Cis Rene NinžoDokument3 SeitenCis Rene NinžoJean Leloup VreavloNoch keine Bewertungen

- ENGAY, Marivic M.-SAMPLE PROBLEM - RECORDING BUSINESS TRANSACTIONSDokument7 SeitenENGAY, Marivic M.-SAMPLE PROBLEM - RECORDING BUSINESS TRANSACTIONSEmgee EngayNoch keine Bewertungen

- A Study of Customer Satisfaction For Services Provided by KCC BankDokument72 SeitenA Study of Customer Satisfaction For Services Provided by KCC BankANKITNoch keine Bewertungen

- CIMA Application Form GuideDokument8 SeitenCIMA Application Form GuidematsusajerryNoch keine Bewertungen

- Gvs BankingDokument4 SeitenGvs BankingGayatriThotakuraNoch keine Bewertungen

- CH 21Dokument86 SeitenCH 21Sayed Mashfiq RahmanNoch keine Bewertungen

- Lucio TanDokument12 SeitenLucio TanNolyne Faith O. VendiolaNoch keine Bewertungen

- Agricultural Debt Waiver and Debt Relief SchemeDokument11 SeitenAgricultural Debt Waiver and Debt Relief SchemehiteshvavaiyaNoch keine Bewertungen

- Subs Testing Proc AAADokument18 SeitenSubs Testing Proc AAARosario Garcia CatugasNoch keine Bewertungen

- Internship Report Format For UIMSDokument17 SeitenInternship Report Format For UIMSasimkhan2014Noch keine Bewertungen

- JKR PWD Form 203A With Bills of QuantitiesDokument54 SeitenJKR PWD Form 203A With Bills of QuantitiesGnabBang50% (2)

- Project ProposalDokument6 SeitenProject ProposaladtyshkhrNoch keine Bewertungen

- Earnings Insight FactSet 01-2019Dokument29 SeitenEarnings Insight FactSet 01-2019krg09Noch keine Bewertungen

- Audit Risk PDFDokument1 SeiteAudit Risk PDFaon waqasNoch keine Bewertungen

- STMNT 112013 9773Dokument3 SeitenSTMNT 112013 9773redbird77100% (1)

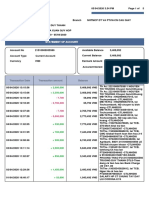

- Statement of Account: Transaction Amount Balance Transaction Details Transaction DateDokument5 SeitenStatement of Account: Transaction Amount Balance Transaction Details Transaction DatehyhNoch keine Bewertungen

- Know All Men by These Presents:: For Use by Ofws OnlyDokument3 SeitenKnow All Men by These Presents:: For Use by Ofws OnlyartemisNoch keine Bewertungen

- Ific Final ReportDokument26 SeitenIfic Final ReportFahim AhmedNoch keine Bewertungen

- Bank Muamalat Apply Form CompleteDokument10 SeitenBank Muamalat Apply Form CompleteewanPGNoch keine Bewertungen

- Sec. 99 A Reinsurance Is Presumed To Be A Contract of Indemnity Against Liability, and Not Merely Against DamageDokument2 SeitenSec. 99 A Reinsurance Is Presumed To Be A Contract of Indemnity Against Liability, and Not Merely Against DamageFlorena CayundaNoch keine Bewertungen

- Front Office AccountingDokument13 SeitenFront Office AccountingpranithNoch keine Bewertungen

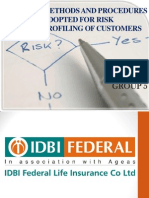

- Methods and Procedures For Risk Profiling ofDokument18 SeitenMethods and Procedures For Risk Profiling ofRohith VijayanNoch keine Bewertungen

- PayGate PayWebv2 v1.15Dokument23 SeitenPayGate PayWebv2 v1.15gmk0% (1)

- Director Finance in NYC New York Resume John BowmanDokument3 SeitenDirector Finance in NYC New York Resume John BowmanJohnBowman2Noch keine Bewertungen

- Closed Loop PDFDokument2 SeitenClosed Loop PDFKrishna Kala100% (1)

- Universak BankingDokument33 SeitenUniversak BankingprashantgoruleNoch keine Bewertungen

- E Banking FDokument21 SeitenE Banking FM Javaid Arif QureshiNoch keine Bewertungen

- LC Application FormDokument4 SeitenLC Application FormbpharmbaNoch keine Bewertungen

- Central Bank of India: New Business GroupDokument7 SeitenCentral Bank of India: New Business GroupAbhishek BoseNoch keine Bewertungen

- Basic Bridge: Learn to Play the World's Greatest Card Game in 15 Easy LessonsVon EverandBasic Bridge: Learn to Play the World's Greatest Card Game in 15 Easy LessonsNoch keine Bewertungen

- I Am a Card Counter: Inside the World of Advantage-Play Blackjack!Von EverandI Am a Card Counter: Inside the World of Advantage-Play Blackjack!Noch keine Bewertungen

- Poker: A Beginners Guide To No Limit Texas Holdem and Understand Poker Strategies in Order to Win the Games of PokerVon EverandPoker: A Beginners Guide To No Limit Texas Holdem and Understand Poker Strategies in Order to Win the Games of PokerBewertung: 5 von 5 Sternen5/5 (49)

- Alchemy Elementals: A Tool for Planetary Healing: An Immersive Audio Experience for Spiritual AwakeningVon EverandAlchemy Elementals: A Tool for Planetary Healing: An Immersive Audio Experience for Spiritual AwakeningBewertung: 5 von 5 Sternen5/5 (5)

- Molly's Game: The True Story of the 26-Year-Old Woman Behind the Most Exclusive, High-Stakes Underground Poker Game in the WorldVon EverandMolly's Game: The True Story of the 26-Year-Old Woman Behind the Most Exclusive, High-Stakes Underground Poker Game in the WorldBewertung: 3.5 von 5 Sternen3.5/5 (129)

- Poker: How to Play Texas Hold'em Poker: A Beginner's Guide to Learn How to Play Poker, the Rules, Hands, Table, & ChipsVon EverandPoker: How to Play Texas Hold'em Poker: A Beginner's Guide to Learn How to Play Poker, the Rules, Hands, Table, & ChipsBewertung: 4.5 von 5 Sternen4.5/5 (6)

- Ultimate Guide to Poker Tells: Devastate Opponents by Reading Body Language, Table Talk, Chip Moves, and Much MoreVon EverandUltimate Guide to Poker Tells: Devastate Opponents by Reading Body Language, Table Talk, Chip Moves, and Much MoreBewertung: 3 von 5 Sternen3/5 (2)

- Earn $30,000 Per Month Playing Online Poker: A Step-By-Step Guide to Single Table TournamentsVon EverandEarn $30,000 Per Month Playing Online Poker: A Step-By-Step Guide to Single Table TournamentsBewertung: 2 von 5 Sternen2/5 (6)

- Your Worst Poker Enemy: Master The Mental GameVon EverandYour Worst Poker Enemy: Master The Mental GameBewertung: 3.5 von 5 Sternen3.5/5 (1)

- The Book of Card Games: The Complete Rules to the Classics, Family Favorites, and Forgotten GamesVon EverandThe Book of Card Games: The Complete Rules to the Classics, Family Favorites, and Forgotten GamesNoch keine Bewertungen

- The Everything Bridge Book: Easy-to-follow instructions to have you playing in no time!Von EverandThe Everything Bridge Book: Easy-to-follow instructions to have you playing in no time!Noch keine Bewertungen

- Cards and Card Tricks, Containing a Brief History of Playing Cards: Full Instructions with Illustrated Hands, for Playing Nearly all Known Games of Chance or Skill; And Directions for Performing a Number of Amusing TricksVon EverandCards and Card Tricks, Containing a Brief History of Playing Cards: Full Instructions with Illustrated Hands, for Playing Nearly all Known Games of Chance or Skill; And Directions for Performing a Number of Amusing TricksNoch keine Bewertungen

- The Everything Card Tricks Book: Over 100 Amazing Tricks to Impress Your Friends And Family!Von EverandThe Everything Card Tricks Book: Over 100 Amazing Tricks to Impress Your Friends And Family!Noch keine Bewertungen

- Shortness: A Key to Better Bidding, Second EditionVon EverandShortness: A Key to Better Bidding, Second EditionBewertung: 5 von 5 Sternen5/5 (1)

- POKER MATH: Putting the Odds in Your Favor: The Science of Poker MathematicsVon EverandPOKER MATH: Putting the Odds in Your Favor: The Science of Poker MathematicsNoch keine Bewertungen

- How to Be a Poker Player: The Philosophy of PokerVon EverandHow to Be a Poker Player: The Philosophy of PokerBewertung: 4.5 von 5 Sternen4.5/5 (4)

- Blackjack Card Counting: How to be a Professional GamblerVon EverandBlackjack Card Counting: How to be a Professional GamblerBewertung: 4 von 5 Sternen4/5 (7)

- Everybody Wins: Four Decades of the Greatest Board Games Ever MadeVon EverandEverybody Wins: Four Decades of the Greatest Board Games Ever MadeNoch keine Bewertungen

- The Little Book of Bridge: Learn How to Play, Score, and WinVon EverandThe Little Book of Bridge: Learn How to Play, Score, and WinNoch keine Bewertungen