Das könnte Ihnen auch gefallen

- Final Project EXIM FINANCEDokument78 SeitenFinal Project EXIM FINANCErohit utekar100% (1)

- Treasury Operations In Turkey and Contemporary Sovereign Treasury ManagementVon EverandTreasury Operations In Turkey and Contemporary Sovereign Treasury ManagementNoch keine Bewertungen

- Offshore Banking in BangladeshDokument5 SeitenOffshore Banking in BangladeshAbdul Ahad SheikhNoch keine Bewertungen

- Unlocking The Secrets Of Bitcoin And Cryptocurrency: Crypto Currency Made EasyVon EverandUnlocking The Secrets Of Bitcoin And Cryptocurrency: Crypto Currency Made EasyBewertung: 1 von 5 Sternen1/5 (1)

- International Banking (Assignment)Dokument18 SeitenInternational Banking (Assignment)JILPA76% (17)

- Role of Foreign Commercial Banks in Indian EconomyDokument25 SeitenRole of Foreign Commercial Banks in Indian EconomySantosh Parashar50% (2)

- Basics of SFMS StandardsDokument3 SeitenBasics of SFMS Standardsgani_scribdNoch keine Bewertungen

- Sohar International Bank SAOGDokument9 SeitenSohar International Bank SAOGsaleem razaNoch keine Bewertungen

- Foreign Remittance of DBBLDokument57 SeitenForeign Remittance of DBBLtariqul21100% (1)

- Foreign Exchange Department - Punjab National BankDokument23 SeitenForeign Exchange Department - Punjab National BankHusein RangwalaNoch keine Bewertungen

- SPF Client Compliance Application Blocked Funds mt799 PPP v1.1Dokument16 SeitenSPF Client Compliance Application Blocked Funds mt799 PPP v1.1David TamakloeNoch keine Bewertungen

- Karnataka Bank Vishal Chopra 05110Dokument64 SeitenKarnataka Bank Vishal Chopra 05110Kiran Gowda100% (1)

- What Is An International Bank?: AnswerDokument22 SeitenWhat Is An International Bank?: AnswerSonetAsrafulNoch keine Bewertungen

- International Banking SystemDokument24 SeitenInternational Banking SystemSukumar Nandi100% (9)

- Commercial BanksDokument5 SeitenCommercial BankssnehaNoch keine Bewertungen

- Presentation On Export CreditDokument21 SeitenPresentation On Export CreditArpit KhandelwalNoch keine Bewertungen

- Differences Between Commercial Banks and Merchant BanksDokument4 SeitenDifferences Between Commercial Banks and Merchant BanksSrinivas LaishettyNoch keine Bewertungen

- Micro FinanceDokument64 SeitenMicro Financewarezisgr8Noch keine Bewertungen

- BBVA Continental-Preliminary Offering Circular PDFDokument362 SeitenBBVA Continental-Preliminary Offering Circular PDFfanatico1982Noch keine Bewertungen

- HDFC Annual Report 2010 11Dokument156 SeitenHDFC Annual Report 2010 11Niranjan PrasadNoch keine Bewertungen

- BOB Foreign Inward Remittances Application Form PDFDokument6 SeitenBOB Foreign Inward Remittances Application Form PDFVarun SrivastavaNoch keine Bewertungen

- MT799Dokument2 SeitenMT799UBIQUITY India CorporationNoch keine Bewertungen

- Credit Managemant Project: Export FinanceDokument67 SeitenCredit Managemant Project: Export Finance✬ SHANZA MALIK ✬Noch keine Bewertungen

- Closed Loop PDFDokument2 SeitenClosed Loop PDFKrishna Kala100% (1)

- Profits - Successful Transaction in Private Placement ProgramDokument4 SeitenProfits - Successful Transaction in Private Placement ProgramDavid Enmanuel Rodriguez LopezNoch keine Bewertungen

- Export Finance (Case Study Need To Be Added)Dokument62 SeitenExport Finance (Case Study Need To Be Added)rupalNoch keine Bewertungen

- Swiss Bank ProjectDokument37 SeitenSwiss Bank ProjectDhwani RajyaguruNoch keine Bewertungen

- Role of IBBL - Promoting Export, Import Business and Inward Foreign RemittanceDokument22 SeitenRole of IBBL - Promoting Export, Import Business and Inward Foreign RemittanceSohel JoyNoch keine Bewertungen

- Etisalat Bond Prospectus PDFDokument2 SeitenEtisalat Bond Prospectus PDFLisaNoch keine Bewertungen

- MT 760 Bank InstrumentsDokument1 SeiteMT 760 Bank InstrumentskdelaozNoch keine Bewertungen

- Buyers Credit: NOTE-Nostro Account Is An Account of An Indian Bank With A Bank Outside India in Foreign CurrencyDokument14 SeitenBuyers Credit: NOTE-Nostro Account Is An Account of An Indian Bank With A Bank Outside India in Foreign Currencyshubh92Noch keine Bewertungen

- Banking Products and ServicesDokument13 SeitenBanking Products and ServicesDharmeshParikhNoch keine Bewertungen

- The Bond Market in GhanaDokument12 SeitenThe Bond Market in GhanaJohn Kennedy Akotia100% (3)

- Incentives EPZDokument1 SeiteIncentives EPZMOHAMMED ALI CHOWDHURYNoch keine Bewertungen

- ICC Global Trade and Finance Survey 2014Dokument144 SeitenICC Global Trade and Finance Survey 2014Radu Victor Tapu100% (1)

- Import FinanceDokument6 SeitenImport FinanceSammir Malhotra0% (1)

- Credit Management of NCC Bank Ltd.Dokument69 SeitenCredit Management of NCC Bank Ltd.death_heaven100% (1)

- Company Profile of KBZ BankDokument6 SeitenCompany Profile of KBZ BankKaung Ma Lay100% (1)

- Format Description Mt103 RCM v1 0 RCCDokument10 SeitenFormat Description Mt103 RCM v1 0 RCCharirk1986Noch keine Bewertungen

- New Non Banking Financial InstitutionsDokument18 SeitenNew Non Banking Financial InstitutionsGarima SinghNoch keine Bewertungen

- Jana Bank General Terms and Conditions For AccountsDokument18 SeitenJana Bank General Terms and Conditions For AccountsArc En CielNoch keine Bewertungen

- Swiss BankDokument14 SeitenSwiss BankVrinda GoyalNoch keine Bewertungen

- NZ: Open Bank ResolutionDokument23 SeitenNZ: Open Bank ResolutionBecket AdamsNoch keine Bewertungen

- ND 2 BFN Financial Institutions Lectures 2023Dokument20 SeitenND 2 BFN Financial Institutions Lectures 2023sanusi bello bakuraNoch keine Bewertungen

- Letter of CreditDokument16 SeitenLetter of CreditDaniyal100% (2)

- Arranging Finance For ExportDokument14 SeitenArranging Finance For ExportmaxsoniiNoch keine Bewertungen

- Certified Trade Finance SpecialistDokument4 SeitenCertified Trade Finance SpecialistKeith Parker100% (2)

- International BankingDokument28 SeitenInternational BankingPayal BhattNoch keine Bewertungen

- Axis BankDokument2 SeitenAxis BankAyush LohiaNoch keine Bewertungen

- Islamic Bank in Tanzania - Amana BankDokument8 SeitenIslamic Bank in Tanzania - Amana BankJaffer J. KesowaniNoch keine Bewertungen

- Merchant Banking (In The Light of SEBI (Merchat Bankers) Regulations, 1992)Dokument38 SeitenMerchant Banking (In The Light of SEBI (Merchat Bankers) Regulations, 1992)Parul PrasadNoch keine Bewertungen

- Financial Crices in BangladeshDokument22 SeitenFinancial Crices in BangladeshTarique AdnanNoch keine Bewertungen

- Global Leasing ToolkitDokument18 SeitenGlobal Leasing ToolkitIFC Access to Finance and Financial Markets0% (1)

- Regal Bond Information Memorandum 11.05.2015.Issued10thApril - CompressedDokument28 SeitenRegal Bond Information Memorandum 11.05.2015.Issued10thApril - Compressedhung_hatheNoch keine Bewertungen

- Bank ServDokument16 SeitenBank ServaNoch keine Bewertungen

- Radhika Growth of Banking SectorDokument36 SeitenRadhika Growth of Banking SectorPranav ViraNoch keine Bewertungen

- Innovation in Indian Banking SectorDokument20 SeitenInnovation in Indian Banking Sectorshalu71% (24)

- Foreign Exchange Activities of Merchantile Bank LTDDokument160 SeitenForeign Exchange Activities of Merchantile Bank LTDtanvirNoch keine Bewertungen

- Wolfgang Keller at Konigsbrau-TAK CASE ANALYSISDokument3 SeitenWolfgang Keller at Konigsbrau-TAK CASE ANALYSISArefeen Hridoy100% (11)

- What Is Recruitment and SelectionDokument2 SeitenWhat Is Recruitment and SelectionArefeen HridoyNoch keine Bewertungen

- Wolfgang Keller at Konigsbrau-TAK PresentationDokument22 SeitenWolfgang Keller at Konigsbrau-TAK PresentationArefeen Hridoy100% (3)

- Applicant Resource - How To Write A CV and Covering Letter May 2013 PDFDokument7 SeitenApplicant Resource - How To Write A CV and Covering Letter May 2013 PDFDarren TurnerNoch keine Bewertungen

- Why Do We Need To Learn Economic GeographyDokument4 SeitenWhy Do We Need To Learn Economic GeographyArefeen Hridoy100% (1)

- Dutch Bangla Bank ATM Service QualityDokument22 SeitenDutch Bangla Bank ATM Service QualityArefeen HridoyNoch keine Bewertungen

- Biman Bangladesh AirlinesDokument18 SeitenBiman Bangladesh AirlinesArefeen HridoyNoch keine Bewertungen

- Health and Safety Audit PresentationDokument23 SeitenHealth and Safety Audit PresentationArefeen HridoyNoch keine Bewertungen

- Bangladesh Bank HR FunctionDokument4 SeitenBangladesh Bank HR FunctionArefeen HridoyNoch keine Bewertungen

- Transom Electronics LTDDokument20 SeitenTransom Electronics LTDArefeen HridoyNoch keine Bewertungen

- 4 Things You Should Never Do After A Job InterviewDokument6 Seiten4 Things You Should Never Do After A Job InterviewArefeen HridoyNoch keine Bewertungen

- Sultanul Arefeen Md. Asif - Hepatitis B CaseStudy PDFDokument29 SeitenSultanul Arefeen Md. Asif - Hepatitis B CaseStudy PDFArefeen HridoyNoch keine Bewertungen

- An Evaluation of HRM Practice at Agrani Bank LimitedDokument59 SeitenAn Evaluation of HRM Practice at Agrani Bank LimitedShah Riar Kabir100% (1)

- Off-Shore Banking Unit: Key Operational & Risk Management AspectDokument1 SeiteOff-Shore Banking Unit: Key Operational & Risk Management AspectArefeen HridoyNoch keine Bewertungen

- The Firm Wide 360 Performance Evaluation Process at Morgan StanleyDokument4 SeitenThe Firm Wide 360 Performance Evaluation Process at Morgan StanleyArefeen Hridoy50% (2)

- General Banking Function of Agrani Bank LimitedDokument41 SeitenGeneral Banking Function of Agrani Bank LimitedArefeen HridoyNoch keine Bewertungen

- Master Budgeting Video SlidesDokument35 SeitenMaster Budgeting Video SlidesArefeen HridoyNoch keine Bewertungen

- Business Plan-All in 1 Service CenterDokument23 SeitenBusiness Plan-All in 1 Service CenterArefeen HridoyNoch keine Bewertungen

- International Economic (Group Assignment)Dokument12 SeitenInternational Economic (Group Assignment)Ahmad FauzanNoch keine Bewertungen

- Price and Output Determination Under Monopoly MarketDokument16 SeitenPrice and Output Determination Under Monopoly MarketManak Ram SingariyaNoch keine Bewertungen

- Calling DataDokument54 SeitenCalling DatainfoNoch keine Bewertungen

- Holly Tree 2015 990taxDokument21 SeitenHolly Tree 2015 990taxstan rawlNoch keine Bewertungen

- A Final Board Packet August 7, 2013 - 0.... 5Dokument199 SeitenA Final Board Packet August 7, 2013 - 0.... 5نيرمين احمدNoch keine Bewertungen

- Resume of SirducdinhDokument1 SeiteResume of Sirducdinhapi-25690844Noch keine Bewertungen

- Worldwide Service Network: Middle EastDokument3 SeitenWorldwide Service Network: Middle EastRavi ShankarNoch keine Bewertungen

- Stock Statement Format For Bank LoanDokument1 SeiteStock Statement Format For Bank Loanpsycho Neha40% (5)

- Export Invoice: Item Description: Qty: UOM: Curr Unit PriceDokument4 SeitenExport Invoice: Item Description: Qty: UOM: Curr Unit PriceAdam GreenNoch keine Bewertungen

- Elasticity & SurplusDokument6 SeitenElasticity & SurplusakashNoch keine Bewertungen

- Ethics DigestDokument29 SeitenEthics DigestTal Migallon100% (1)

- Understanding ManagementDokument35 SeitenUnderstanding ManagementXian-liNoch keine Bewertungen

- Lesson 23 Illustrating Simple and Compound InterestDokument12 SeitenLesson 23 Illustrating Simple and Compound InterestANGELIE FERNANDEZNoch keine Bewertungen

- Herbert HooverDokument4 SeitenHerbert HooverZuñiga Salazar Hamlet EnocNoch keine Bewertungen

- Section 125 Digested CasesDokument6 SeitenSection 125 Digested CasesRobNoch keine Bewertungen

- Certification of Residency - Form A - AccomplishedDokument2 SeitenCertification of Residency - Form A - AccomplishedjonbertNoch keine Bewertungen

- Liebherr Annual-Report 2017 en Klein PDFDokument82 SeitenLiebherr Annual-Report 2017 en Klein PDFPradeep AdsareNoch keine Bewertungen

- M2 Post-Task Regional Economic IntegrationDokument10 SeitenM2 Post-Task Regional Economic IntegrationJean SantosNoch keine Bewertungen

- Financial ServicesDokument42 SeitenFinancial ServicesGururaj Av100% (1)

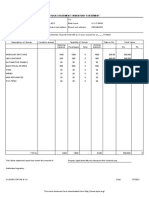

- Account Statement: Date Value Date Description Cheque Deposit Withdrawal BalanceDokument2 SeitenAccount Statement: Date Value Date Description Cheque Deposit Withdrawal BalancesadhanaNoch keine Bewertungen

- The Issue of Praedial Larceny in JamaicaDokument2 SeitenThe Issue of Praedial Larceny in JamaicaNavin NarineNoch keine Bewertungen

- PHM PCH EnglishDokument9 SeitenPHM PCH Englishlalit823187Noch keine Bewertungen

- Cola Wars PresentationDokument13 SeitenCola Wars PresentationkvnikhilreddyNoch keine Bewertungen

- Indias Defence BudgetDokument1 SeiteIndias Defence BudgetNishkamyaNoch keine Bewertungen

- We Control The World's Wealth Twitter1.2.19Dokument19 SeitenWe Control The World's Wealth Twitter1.2.19karen hudesNoch keine Bewertungen

- Wells Fargo Everyday CheckingDokument6 SeitenWells Fargo Everyday CheckingDavid Dali Rojas Huamanchau100% (1)

- The Mastercard Index of Women EntrepreneursDokument118 SeitenThe Mastercard Index of Women EntrepreneursxuetingNoch keine Bewertungen

- Gender Wise Classification of RespondentsDokument34 SeitenGender Wise Classification of Respondentspavith ranNoch keine Bewertungen

- Study Notes: Entrepreneurship DevelopmentDokument80 SeitenStudy Notes: Entrepreneurship DevelopmentDevid S. StansfieldNoch keine Bewertungen

- B2B Marketing - MRFDokument13 SeitenB2B Marketing - MRFMohit JainNoch keine Bewertungen

- Finance Basics (HBR 20-Minute Manager Series)Von EverandFinance Basics (HBR 20-Minute Manager Series)Bewertung: 4.5 von 5 Sternen4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaVon EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaBewertung: 4.5 von 5 Sternen4.5/5 (14)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingVon EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingBewertung: 4.5 von 5 Sternen4.5/5 (17)

- Value: The Four Cornerstones of Corporate FinanceVon EverandValue: The Four Cornerstones of Corporate FinanceBewertung: 4.5 von 5 Sternen4.5/5 (18)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetVon EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetBewertung: 5 von 5 Sternen5/5 (2)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successVon EverandReady, Set, Growth hack:: A beginners guide to growth hacking successBewertung: 4.5 von 5 Sternen4.5/5 (93)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistVon EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistBewertung: 4.5 von 5 Sternen4.5/5 (73)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisVon EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisBewertung: 5 von 5 Sternen5/5 (6)

- Joy of Agility: How to Solve Problems and Succeed SoonerVon EverandJoy of Agility: How to Solve Problems and Succeed SoonerBewertung: 4 von 5 Sternen4/5 (1)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelVon Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNoch keine Bewertungen

- Financial Risk Management: A Simple IntroductionVon EverandFinancial Risk Management: A Simple IntroductionBewertung: 4.5 von 5 Sternen4.5/5 (7)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityVon EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityBewertung: 4.5 von 5 Sternen4.5/5 (4)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursVon EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursBewertung: 4.5 von 5 Sternen4.5/5 (8)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialVon EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialBewertung: 4.5 von 5 Sternen4.5/5 (32)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)Von EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Bewertung: 4.5 von 5 Sternen4.5/5 (4)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsVon EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNoch keine Bewertungen

- How to Measure Anything: Finding the Value of Intangibles in BusinessVon EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessBewertung: 3.5 von 5 Sternen3.5/5 (4)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanVon EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanBewertung: 4.5 von 5 Sternen4.5/5 (79)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNVon Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNBewertung: 4.5 von 5 Sternen4.5/5 (3)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialVon EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNoch keine Bewertungen

- The Synergy Solution: How Companies Win the Mergers and Acquisitions GameVon EverandThe Synergy Solution: How Companies Win the Mergers and Acquisitions GameNoch keine Bewertungen

- Creating Shareholder Value: A Guide For Managers And InvestorsVon EverandCreating Shareholder Value: A Guide For Managers And InvestorsBewertung: 4.5 von 5 Sternen4.5/5 (8)

- Value: The Four Cornerstones of Corporate FinanceVon EverandValue: The Four Cornerstones of Corporate FinanceBewertung: 5 von 5 Sternen5/5 (2)