Das könnte Ihnen auch gefallen

- Activity 3 - International Trade TheoryDokument4 SeitenActivity 3 - International Trade TheoryIris leavesNoch keine Bewertungen

- GermanyDokument52 SeitenGermanyMinh Trần Bảo NgọcNoch keine Bewertungen

- Globalization German1Dokument4 SeitenGlobalization German1ismadinNoch keine Bewertungen

- Deutsche Bank ResearchDokument12 SeitenDeutsche Bank ResearchMichael GreenNoch keine Bewertungen

- International Economics, Group 4Dokument16 SeitenInternational Economics, Group 4Kinnari PopatNoch keine Bewertungen

- Outlook For The German Economy - Macroeconomic Projections For 2011 and 2012Dokument14 SeitenOutlook For The German Economy - Macroeconomic Projections For 2011 and 2012Ravi KantNoch keine Bewertungen

- Rising Domestic Demand and Net Exports Underpin German GrowthDokument15 SeitenRising Domestic Demand and Net Exports Underpin German Growthapi-228714775Noch keine Bewertungen

- German Foreign Trade With China: China's Importance As A Trading Partner Has Grown ConsiderablyDokument3 SeitenGerman Foreign Trade With China: China's Importance As A Trading Partner Has Grown ConsiderablyCristina CiolpanNoch keine Bewertungen

- 5.internet8722: According To The Country's Statistics OfficeDokument3 Seiten5.internet8722: According To The Country's Statistics OfficeMichelle BabaNoch keine Bewertungen

- Activity 1 - GlobalizationDokument4 SeitenActivity 1 - GlobalizationIris leavesNoch keine Bewertungen

- 201104mba en German BalanceDokument20 Seiten201104mba en German BalanceRohan KulkarniNoch keine Bewertungen

- GermanyDokument58 SeitenGermanyMinh Trần Bảo NgọcNoch keine Bewertungen

- Germany Country Analysis - Social, Cultural, Economic Context For BusinessDokument40 SeitenGermany Country Analysis - Social, Cultural, Economic Context For BusinessJustinNoch keine Bewertungen

- Trường Đại Học Kinh Tế Quốc Dân: The opportunities and issues of Luc Ngan lychee joining the German marketDokument13 SeitenTrường Đại Học Kinh Tế Quốc Dân: The opportunities and issues of Luc Ngan lychee joining the German marketTrần Lan AnhNoch keine Bewertungen

- 2 50 Years: in GermanyDokument1 Seite2 50 Years: in Germanyapi-128415287Noch keine Bewertungen

- B2B E-Commerce Strategies For The Chinese Manufacturing MarketDokument25 SeitenB2B E-Commerce Strategies For The Chinese Manufacturing MarketGXSNoch keine Bewertungen

- Trade Gloom Drives French and German Economic DivergenceDokument7 SeitenTrade Gloom Drives French and German Economic DivergencemakedonisNoch keine Bewertungen

- Emerging Opportunities in The PhilppinestDokument2 SeitenEmerging Opportunities in The PhilppinestjudemcNoch keine Bewertungen

- Van MM1 Tot MM8Dokument30 SeitenVan MM1 Tot MM8FDwebredNoch keine Bewertungen

- EURObiz 7thDokument60 SeitenEURObiz 7thperico1962Noch keine Bewertungen

- HCMC QMR Q2 2015 - enDokument265 SeitenHCMC QMR Q2 2015 - enTrung VõNoch keine Bewertungen

- 2b Facts About German Foreign Trade 2022 BMWKDokument20 Seiten2b Facts About German Foreign Trade 2022 BMWKhilal050106Noch keine Bewertungen

- China Export FT - VGDokument10 SeitenChina Export FT - VGLuiz MartinsNoch keine Bewertungen

- Germany: BackgroundDokument4 SeitenGermany: BackgroundNargis Noordeen100% (1)

- Task 2-Demand and Supply (350 Words) : - Great Supply Product: Motor VehicleDokument10 SeitenTask 2-Demand and Supply (350 Words) : - Great Supply Product: Motor VehicleLy Lê KhánhNoch keine Bewertungen

- Biuletyn IZ NR 208Dokument7 SeitenBiuletyn IZ NR 208Instytut Zachodni w PoznaniuNoch keine Bewertungen

- German EconomyDokument5 SeitenGerman EconomyprakharNoch keine Bewertungen

- Vietnam's FDI Outlook For 2016: 2. Sources of InvestmentDokument5 SeitenVietnam's FDI Outlook For 2016: 2. Sources of InvestmentSean O'PryNoch keine Bewertungen

- Group 2 - Section BDokument20 SeitenGroup 2 - Section BSeemaNoch keine Bewertungen

- For Official Use STD/NAES/TASS/ITS (2006) 16: Statistics DirectorateDokument16 SeitenFor Official Use STD/NAES/TASS/ITS (2006) 16: Statistics DirectoratebachibNoch keine Bewertungen

- German EconomyDokument5 SeitenGerman EconomyprakharNoch keine Bewertungen

- Deutsche Industriebank German Market Outlook 2014 Mid Cap Financial Markets in Times of Macro Uncertainty and Tightening Bank RegulationsDokument32 SeitenDeutsche Industriebank German Market Outlook 2014 Mid Cap Financial Markets in Times of Macro Uncertainty and Tightening Bank RegulationsRichard HongNoch keine Bewertungen

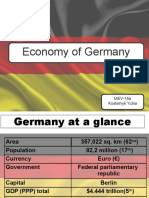

- Economy of Germany: MEV-18a Kostelnyk YuliiaDokument21 SeitenEconomy of Germany: MEV-18a Kostelnyk YuliiaЮлияNoch keine Bewertungen

- China Economy Case StudyDokument8 SeitenChina Economy Case StudyShem W Lyngdoh100% (1)

- GermanyDokument3 SeitenGermanysaifNoch keine Bewertungen

- ENR Top 250 International Contractors-2015Dokument77 SeitenENR Top 250 International Contractors-2015OnurUmanNoch keine Bewertungen

- Ifm Cia 1Dokument8 SeitenIfm Cia 1Dharshan ChandrasekaranNoch keine Bewertungen

- Facts and Figures On EU-China Trade: Did You Know?Dokument2 SeitenFacts and Figures On EU-China Trade: Did You Know?Aleksandar SavicNoch keine Bewertungen

- MACRO ECONOMIC THEORY AND POLICY CIA 1 ConvDokument21 SeitenMACRO ECONOMIC THEORY AND POLICY CIA 1 ConvAastha SinghNoch keine Bewertungen

- General Trends in FDIDokument2 SeitenGeneral Trends in FDIGabyNoch keine Bewertungen

- Working Paper Number 110: Sanjaya Lall and Manuel AlbaladejoDokument29 SeitenWorking Paper Number 110: Sanjaya Lall and Manuel Albaladejomemm1Noch keine Bewertungen

- Economic Growth - China EssayDokument7 SeitenEconomic Growth - China EssayAnjali PatelNoch keine Bewertungen

- Economics 1Dokument5 SeitenEconomics 1Mansi SainiNoch keine Bewertungen

- FDI in China Dullien 2005Dokument29 SeitenFDI in China Dullien 2005Hans Grungilungi ChristianNoch keine Bewertungen

- Нов Презентация на Microsoft PowerPointDokument7 SeitenНов Презентация на Microsoft PowerPointIulia BurtoiuNoch keine Bewertungen

- Euro ZoneDokument3 SeitenEuro Zonedavid_llewellyn_smithNoch keine Bewertungen

- Country Risk Analysis-GermanyDokument22 SeitenCountry Risk Analysis-Germanyamitsharma_acdsNoch keine Bewertungen

- EIB Investment Survey 2018 - Czech Republic overviewVon EverandEIB Investment Survey 2018 - Czech Republic overviewNoch keine Bewertungen

- 51 Nicolas FancoiseDokument39 Seiten51 Nicolas Fancoiseaaaaa53Noch keine Bewertungen

- 33Dokument1 Seite33vitalie GalNoch keine Bewertungen

- Country Report: Germany: Submitted byDokument12 SeitenCountry Report: Germany: Submitted byJijo Francis100% (1)

- Germany List 6 95Dokument40 SeitenGermany List 6 95ehsanNoch keine Bewertungen

- Indicators For GERMANY: France Ational Tatistical ATADokument25 SeitenIndicators For GERMANY: France Ational Tatistical ATASatNam SiNgh TethiNoch keine Bewertungen

- Multinational CorporationsDokument8 SeitenMultinational CorporationsThu Huệ Nguyễn ThịNoch keine Bewertungen

- Industry 4.0 FinaleDokument25 SeitenIndustry 4.0 FinaleFrame UkirkacaNoch keine Bewertungen

- Assignment 2Dokument10 SeitenAssignment 2entc.fdp.zaranaNoch keine Bewertungen

- Swiss Market Index (Smi) FinalDokument28 SeitenSwiss Market Index (Smi) Finalvijay dhondiyalNoch keine Bewertungen

- China's European Outreach Hits A Wall in Germany - Nikkei Asian ReviewDokument13 SeitenChina's European Outreach Hits A Wall in Germany - Nikkei Asian Reviewi am the greatest1Noch keine Bewertungen

- Leadership Mind and HeartDokument12 SeitenLeadership Mind and HeartSidra KhanNoch keine Bewertungen

- CH 03Dokument14 SeitenCH 03Sidra KhanNoch keine Bewertungen

- The Leader As An IndividualDokument15 SeitenThe Leader As An IndividualSidra KhanNoch keine Bewertungen

- 20.32 Tourist Arrivals by SexDokument1 Seite20.32 Tourist Arrivals by SexSidra KhanNoch keine Bewertungen

- Transport & Communications: Air Sea LandDokument1 SeiteTransport & Communications: Air Sea LandSidra KhanNoch keine Bewertungen

- Robbins9 ppt02Dokument23 SeitenRobbins9 ppt02Sidra KhanNoch keine Bewertungen

- Managing and Managers 1 (Autosaved)Dokument19 SeitenManaging and Managers 1 (Autosaved)Sidra KhanNoch keine Bewertungen

- HRM Telenor RPRTDokument19 SeitenHRM Telenor RPRTnoorirocks75% (4)

- Impact of CollaborationDokument19 SeitenImpact of Collaborationinfo4rb6631Noch keine Bewertungen

- FDi Global Free Zones of The Year 2017Dokument15 SeitenFDi Global Free Zones of The Year 2017abasdfNoch keine Bewertungen

- Chapter 1 Managers and You in The WorkplaceDokument75 SeitenChapter 1 Managers and You in The WorkplaceJeff PanNoch keine Bewertungen

- Wilfred Olley's M. ADokument110 SeitenWilfred Olley's M. APrecious EkiNoch keine Bewertungen

- Product Lauch StageDokument13 SeitenProduct Lauch StageMuhd AlhamNoch keine Bewertungen

- Virtual Teams and Management ChallengesDokument9 SeitenVirtual Teams and Management ChallengesNader Ale EbrahimNoch keine Bewertungen

- Prospera Activity Plan 2023-2024Dokument80 SeitenProspera Activity Plan 2023-2024Rifky AdityaNoch keine Bewertungen

- Ideation, Validation & InnovationDokument2 SeitenIdeation, Validation & InnovationMotaherNoch keine Bewertungen

- Transformative RailDokument61 SeitenTransformative RailhimaNoch keine Bewertungen

- Accessaible Self ServiceDokument11 SeitenAccessaible Self ServiceSamiNoch keine Bewertungen

- Plcor FrameworkDokument347 SeitenPlcor Frameworkalain_charpentier100% (2)

- MPT - 062015 PDFDokument62 SeitenMPT - 062015 PDFanjangandak2932Noch keine Bewertungen

- RMK10 Full DocumentDokument451 SeitenRMK10 Full DocumentHakim AlbasrawyNoch keine Bewertungen

- PDF - 2023-03-19T191643.181Dokument16 SeitenPDF - 2023-03-19T191643.181Labib MohamedNoch keine Bewertungen

- Risk Transfer Innovation: The Key To Emerging Markets For Global ReinsurersDokument11 SeitenRisk Transfer Innovation: The Key To Emerging Markets For Global Reinsurersapi-227433089Noch keine Bewertungen

- UOP Opportunities-and-Developments in PX Production China PX DevelopmentForum April-2014 PDFDokument19 SeitenUOP Opportunities-and-Developments in PX Production China PX DevelopmentForum April-2014 PDFMaria de los AngelesNoch keine Bewertungen

- DocDokument11 SeitenDocCammy ChinNoch keine Bewertungen

- Thesis On Fog ComputingDokument223 SeitenThesis On Fog ComputingSaurav GautamNoch keine Bewertungen

- The Case of A Danish Caravan SiteDokument53 SeitenThe Case of A Danish Caravan Siteblazingsun_11100% (1)

- ESAC 2021 - L2 - SAP S4HANA Data Modelling OnboardingDokument25 SeitenESAC 2021 - L2 - SAP S4HANA Data Modelling OnboardingGabriel GutierrezNoch keine Bewertungen

- Electronic DLLDokument195 SeitenElectronic DLLKathleen Rose ReyesNoch keine Bewertungen

- Telangana PoliciesDokument11 SeitenTelangana PoliciesShravan kumarNoch keine Bewertungen

- Organic Organizational DesignDokument9 SeitenOrganic Organizational DesignANGELA MARIA CAÑIZARES RAMIREZNoch keine Bewertungen

- The Gap Between CIO Core Competencies and The Real Roles of CIOsDokument8 SeitenThe Gap Between CIO Core Competencies and The Real Roles of CIOsManekz Emmanuel Mendoza HernandezNoch keine Bewertungen

- Mail Strategies Fall 2008 IssueDokument36 SeitenMail Strategies Fall 2008 IssueKern USANoch keine Bewertungen

- Kansai Paints CompanyDokument3 SeitenKansai Paints CompanyMahesh ShettyNoch keine Bewertungen

- Failed ProductsDokument49 SeitenFailed ProductsSaifullah KhalidNoch keine Bewertungen

- EoC BDokument2 SeitenEoC BManthan PatilNoch keine Bewertungen

- (David Tolfree, Mark J. Jackson) Commercializing M PDFDokument271 Seiten(David Tolfree, Mark J. Jackson) Commercializing M PDFikhan1234100% (1)